How to Stop the Debt Cycle and Build Better Money Habits

Debt can become a pattern before it becomes a crisis. A credit card covers groceries one month. A personal loan helps with a repair. A buy-now-pay-later plan makes a purchase feel manageable. Then the payments begin to stack up, cash gets tight, and borrowing starts again.

Stopping the debt cycle is not only about paying balances down. That is part of it, but it is not the whole solution. To make real progress, you also need to change the habits, systems, and gaps that keep debt coming back. This takes planning. It also takes patience.

What Is the Debt Cycle?

The debt cycle is a repeated pattern of using borrowed money to cover expenses, then struggling to repay what was borrowed. It can involve credit cards, payday loans, personal loans, medical bills, store cards, or short-term payment plans.

The pattern often looks simple at first. You borrow to cover a need. Then the payment reduces next month’s available cash. Because cash is short, you borrow again. Over time, balances grow and minimum payments become part of the monthly budget.

Many people begin searching for how to get out of debt when they realize the balance is not shrinking, even though they are making payments. That moment can feel discouraging, but it can also be useful. It is the point where the problem becomes clear enough to address.

Why People Get Stuck in Debt

Debt usually has more than one cause. Sometimes it begins with a job loss, medical bill, car repair, or emergency. Sometimes it grows from daily spending that slowly exceeds income. High interest can make the problem worse because much of the payment goes toward interest instead of the balance.

A lack of emergency savings is another common factor. Without a small buffer, every surprise expense can become new debt. Irregular income can also make planning harder. People who freelance, work hourly jobs, or depend on commissions may use credit during low-income months.

There is no need to turn this into a personal failure. Debt is a financial problem. It needs a financial plan.

Start With a Clear Debt Inventory

The first step is to list every debt. Include credit cards, personal loans, medical bills, student loans, auto loans, payday loans, and payment plans. For each one, write down the balance, interest rate, minimum payment, due date, and lender.

Also note whether each account is current or past due. This matters because past-due accounts may require faster attention to avoid more fees, collection activity, or credit damage.

Adding up the full amount may feel uncomfortable. Do it anyway. A clear number gives you a starting point. Without it, you are trying to solve a problem you cannot fully see.

Build a Budget That Prevents New Debt

A debt payoff plan will not work if new debt keeps replacing old debt. That is why a basic budget is necessary.

Start with income. Then list essential expenses such as housing, utilities, groceries, transportation, insurance, and minimum debt payments. After that, look for spending leaks. These might include subscriptions, takeout, convenience purchases, fees, impulse shopping, or unplanned online orders.

The goal is not to cut every enjoyable expense. That usually does not last. The goal is to create room for debt payments and a small savings buffer. A budget should help you stop relying on borrowed money for normal expenses. If you have never built one before, this walkthrough on how to balance your budget effectively covers the basics.

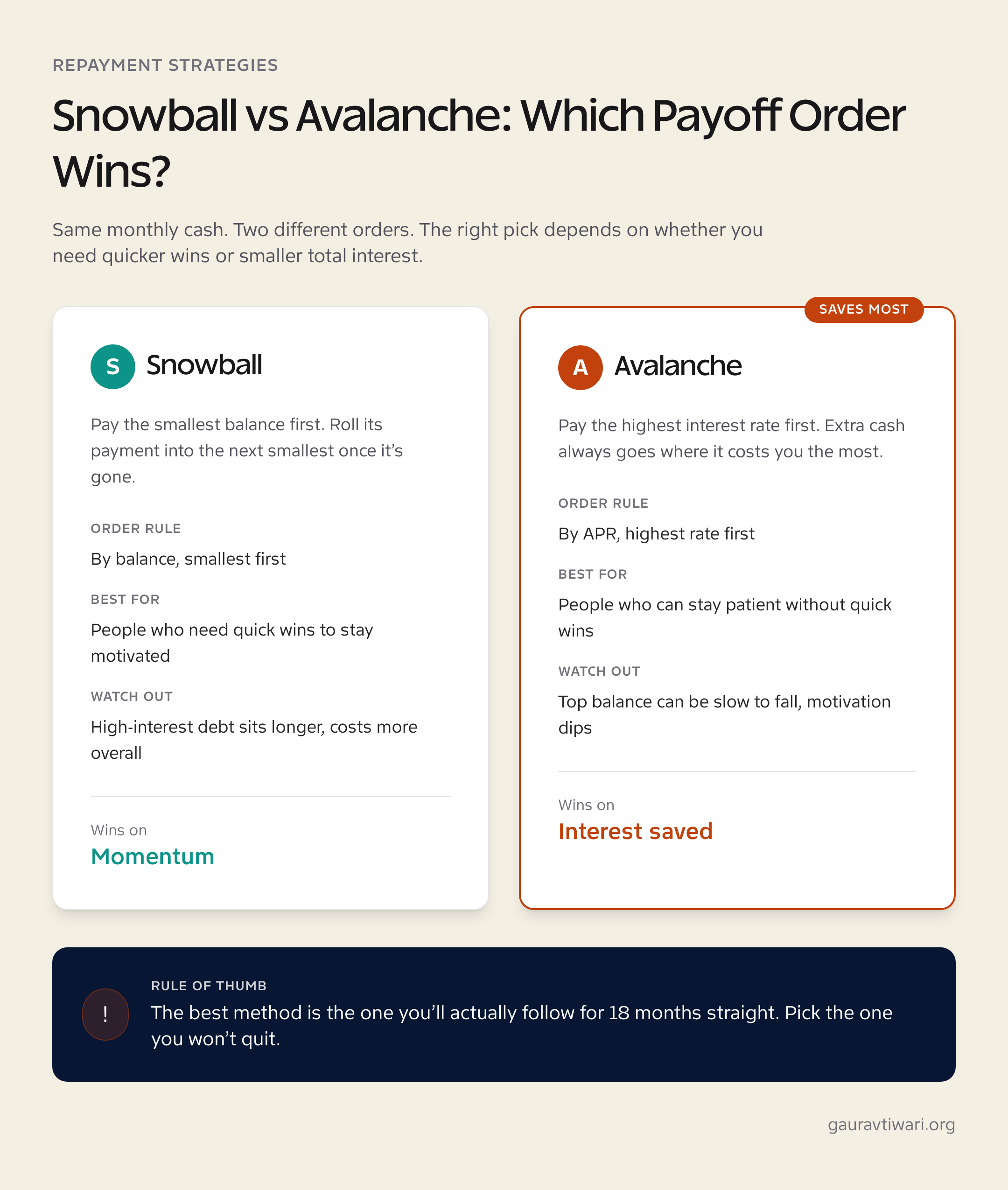

Choose a Debt Repayment Strategy

Once you know your debts and your budget, choose a repayment strategy.

The debt snowball method focuses on the smallest balance first. You make minimum payments on all debts, then put extra money toward the smallest one. Once it is paid off, you roll that payment into the next smallest debt. This method can build motivation because you see accounts disappear faster.

The debt avalanche method focuses on the highest interest rate first. You still make minimum payments on all debts, but extra money goes toward the debt costing you the most. This can save more money over time.

Debt consolidation may also help in some situations. It combines multiple debts into one payment, often with the goal of lowering interest or simplifying repayment. However, consolidation only helps if you stop adding new debt. Otherwise, it can turn into a larger problem.

The best method is the one you can follow consistently.

Build a Small Emergency Fund

Saving while paying off debt may sound backward, but a small emergency fund can help break the borrowing pattern. Without savings, a flat tire or medical copay can send you back to a credit card.

Start with a modest goal. For some people, $500 is a good first target. For others, $1,000 may be more realistic. The amount depends on income, expenses, and risk.

This fund is not for sales, vacations, or regular bills. It is for urgent and unexpected expenses. Even a small buffer can reduce panic and protect your progress.

Change the Habits That Keep Debt Coming Back

Debt repayment is easier when spending habits change too. Start with a pause rule for nonessential purchases. Waiting 24 to 72 hours can reduce impulse spending.

For problem categories, consider using cash or debit. This might apply to dining out, clothes, entertainment, or online shopping. When the money is gone, spending stops.

Unsubscribe from spending triggers. Promotional emails, retail app alerts, and social media shopping content can make unnecessary purchases feel urgent. Remove the pressure where you can.

Plan for irregular expenses with sinking funds. These are small savings categories for predictable costs such as car repairs, gifts, insurance premiums, school expenses, or holidays. When those costs arrive, they will not feel like emergencies.

Reduce Interest and Fees Where Possible

High interest can slow debt payoff. Look for ways to reduce the cost of your debt.

You may be able to call creditors and ask about lower rates, hardship programs, or payment options. Automatic minimum payments or calendar reminders can help you avoid late fees. Balance transfers or consolidation may help some borrowers, but only if the terms are clear and the fees make sense.

Read the details before agreeing to any new product. A lower payment is not always a better deal if the repayment period is much longer or the fees are high.

Increase Income to Speed Up Progress

Cutting expenses has limits. If your budget is already tight, extra income may help more than cutting another small purchase.

Options may include extra shifts, freelance work, seasonal jobs, selling unused items, or using a skill for paid projects. This does not have to be forever. Even a temporary income boost can help pay off a small balance or build an emergency fund.

Assign the money before it arrives. If extra income has no clear purpose, it often disappears into daily spending.

Know When to Ask for Help

Some debt situations need outside support. If you cannot afford minimum payments, have accounts in collections, are using debt for basic needs, or face legal action, consider speaking with a qualified professional.

Nonprofit credit counseling, legal aid, or a trusted financial professional may help you understand your options. Asking for help is not failure. It is a practical step when the situation is too difficult to manage alone. Parents juggling debt and tuition can also find practical ideas in this guide on paying off debt while supporting your kids through school.

Stay Motivated While Breaking the Cycle

Debt payoff takes time. Track your balances monthly so you can see progress. Use a visual tracker if that helps. Celebrate small wins without spending more money.

Setbacks may happen. A hard month does not erase your progress. Adjust the budget, revisit the plan, and keep going.

Final Thoughts

Stopping the debt cycle requires two things: paying down what you owe and changing the habits that make debt return. You need a clear list of debts, a realistic budget, a repayment strategy, and a small emergency fund.

Start with one step today. List every debt. Choose a repayment method. Set aside a small amount for emergencies. Progress begins when you stop guessing and start working from a plan. Once the cycle is broken, the same habits become the foundation for how to achieve financial freedom on your own terms.

Frequently Asked Questions

What is the debt cycle in simple terms?

The debt cycle is a pattern where you borrow money to cover expenses, then have less cash next month because of the repayment, so you borrow again. Balances grow even when you keep making payments.

Should I save or pay off debt first?

Do both, in small amounts. A starter emergency fund of $500 to $1,000 keeps a flat tire or copay from turning into new credit card debt. Once that buffer exists, push extra cash at the debt.

Is the snowball or avalanche method better?

The avalanche saves the most interest because it targets the highest APR first. The snowball builds motivation faster because small balances disappear. The best method is the one you’ll actually follow for the full payoff window.

Will debt consolidation stop the cycle?

Only if you stop adding new debt. Consolidation lowers the rate or simplifies payments, but if the freed-up credit lines get used again, the balance grows back. Pair it with a budget that prevents new borrowing.

How long does it take to break the debt cycle?

Most people who follow a written plan see meaningful progress in 12 to 24 months. Total payoff depends on balance, interest rate, and how much extra you can put toward the debt each month.

When should I ask for professional help?

Call a nonprofit credit counselor or legal aid if you can’t afford minimum payments, have accounts in collections, are using credit for basic needs like groceries, or are facing legal action from a creditor.