How to Balance Your Budget: A Practical Framework That Sticks (2026)

Most budgets fail within 90 days. Not because the math was wrong, but because the structure was unrealistic, the tracking was tedious, or the categories didn’t match how the household actually spends money. The budgeting frameworks that stick across years aren’t the ones with the most categories or the cleverest spreadsheets — they’re the ones simple enough to maintain on a Tuesday evening when you’re tired.

This guide is the practical framework to balance your budget that I’ve watched stick across consulting clients, family members, and my own household over 16 years. The 50/30/20 baseline that works for most situations, when to deviate, how to handle irregular income, and the apps that actually save time vs the ones that add admin work.

Why most budgets fail (the structural failure modes)

- Too many categories. 30+ category budgets become unmaintainable. The brain doesn’t track that many spending buckets in real time.

- Categories that don’t match real life. “Entertainment” sounds clean but combines streaming subscriptions, restaurant meals, concert tickets, and books — spending that should be tracked separately.

- Tracking after the fact, not before. Reviewing last month’s spending tells you what happened. It doesn’t change behavior.

- No buffer for irregular expenses. Budgets that don’t include monthly contributions to annual expenses (car insurance, holidays, birthdays) get derailed quarterly.

- Punishment-based framing. Budgets that feel like deprivation collapse within 60–90 days. Sustainable budgets feel like priorities, not restrictions.

The 50/30/20 baseline (and when to deviate)

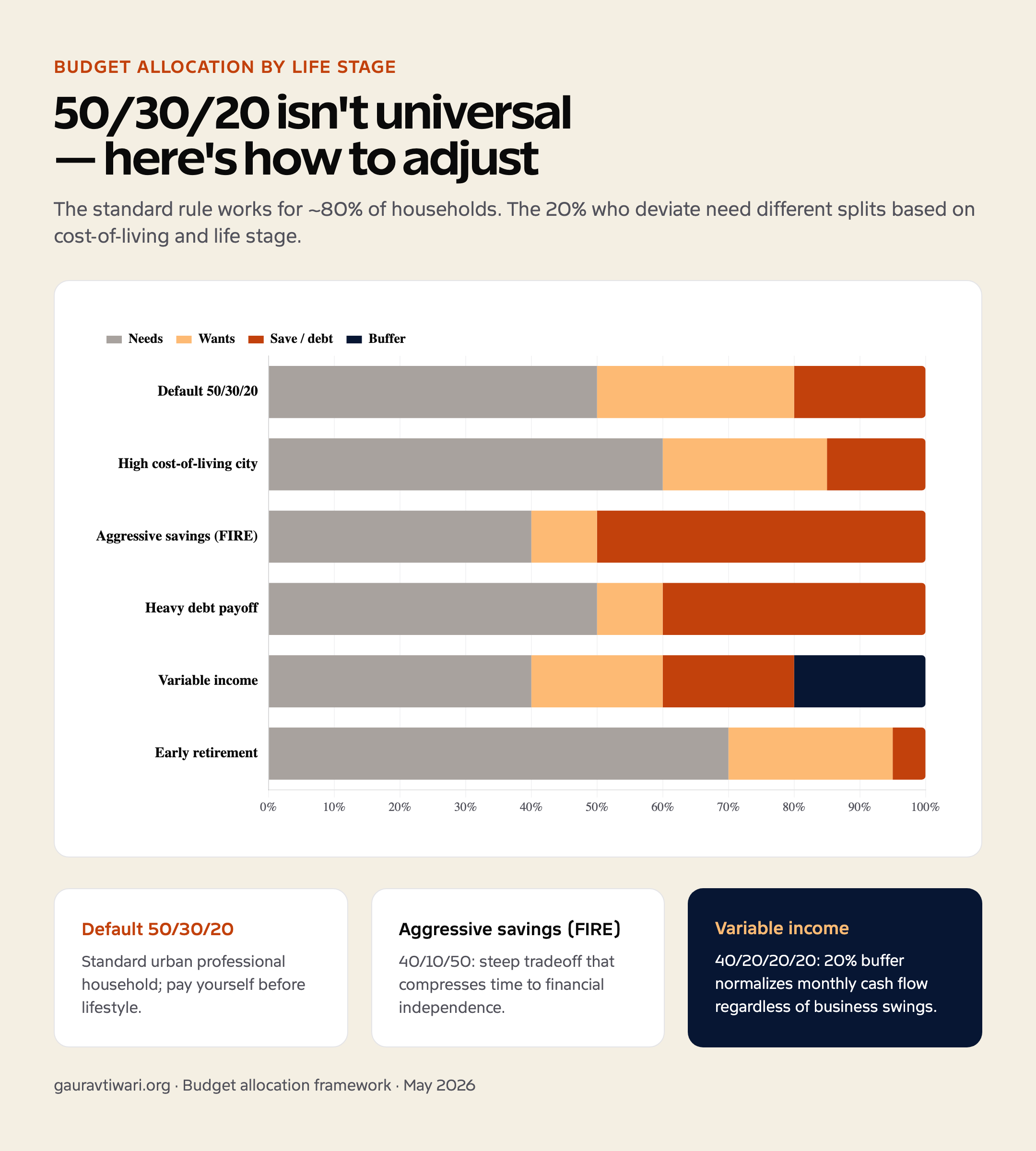

The 50/30/20 framework: 50% of after-tax income for needs, 30% for wants, 20% for savings + debt payoff. It’s the right starting point for ~80% of households. The percentages adjust based on cost-of-living and life stage.

| Situation | Adjusted split | Reason |

|---|---|---|

| Default 50/30/20 | 50% needs / 30% wants / 20% save | Standard urban professional household |

| High cost-of-living city | 60% needs / 25% wants / 15% save | Rent + transport eat more of the budget |

| Aggressive savings (FIRE pursuit) | 40% needs / 10% wants / 50% save | Steep tradeoff but accelerates financial independence |

| Heavy debt payoff phase | 50% needs / 10% wants / 40% debt + save | Temporary; revert after debt cleared |

| Variable income | 40% needs / 20% wants / 20% save / 20% buffer | Buffer normalizes monthly cash flow |

| Early retirement / withdrawal | 70% needs / 25% wants / 5% save | Drawing down rather than accumulating |

What counts as “needs” vs “wants” (the honest version)

Most budget failures start with miscategorizing. Honest definitions:

- Needs (50%): housing (rent/mortgage + utilities), groceries (basic, not premium), transportation (commute), insurance (health, auto, basic life), minimum debt payments, basic clothing. If skipping it would cause real harm in 30 days, it’s a need.

- Wants (30%): dining out, entertainment subscriptions, hobbies, premium groceries, vacations, gym memberships, premium clothing, gifts, gadget upgrades. If skipping it would just be uncomfortable, it’s a want.

- Savings (20%): emergency fund (until 3–6 months expenses), retirement contributions, investment accounts, debt payoff above the minimums.

The boundary that trips most people: a $7 latte is a want. A $7 lunch when you forgot to pack food is a want. The $1,200 phone upgrade when your existing phone works is a want. Honest categorization is uncomfortable but necessary.

Handling irregular and annual expenses

The expenses that derail most budgets aren’t groceries. They’re the predictable-but-irregular ones: car insurance, holidays, birthdays, vacation, car maintenance, medical co-pays, annual subscriptions. Solve this once with a “sinking fund” approach:

- List every annual or irregular expense: car registration, insurance premiums, holiday gifts, vacation, birthdays, annual subscriptions, expected medical costs, home maintenance.

- Sum them annually. Divide by 12.

- Move that monthly amount from your checking to a separate sinking-fund savings account each month.

- When the irregular expense hits, transfer from the sinking fund. The expense is already covered.

Most budgets don’t include this category. The result: every quarter brings a “surprise” expense that derails the plan. Sinking funds make irregular expenses regular and predictable.

Variable income: paying yourself a salary

Freelancers, business owners, commission-based salespeople have irregular monthly income. Trying to budget against irregular income directly fails. The pattern that works:

- Create a buffer account separate from operating accounts.

- Aim for 3 months of expenses in the buffer before you start drawing a fixed salary.

- Pay yourself a fixed monthly amount from the buffer, sized to cover essentials reliably.

- Excess income above the salary goes back into the buffer first; once buffer hits 6–12 months, route to investment.

- Lean months draw from buffer; fat months refill it. Personal cash flow becomes predictable regardless of business cash flow.

Budgeting apps worth using (and the ones that aren’t)

- YNAB (You Need A Budget): envelope-style budgeting with strong forward-planning emphasis. Subscription — $109/year — but the discipline-building is worth it for most users.

- Monarch Money: visual aggregation of accounts, net worth tracking, multi-account view. Strong replacement for the now-defunct Mint. ~$100/year.

- Copilot: Mac/iOS-only, beautiful UI, good auto-categorization. ~$95/year.

- Empower (formerly Personal Capital): free for net-worth tracking and investment analysis. Premium tier for human advisor.

- Fina Money: India-friendly aggregation across UPI, banks, mutual funds.

- Walnut, ET Money, Money Manager (India): India-specific options with good local bank coverage.

- Spreadsheet (Google Sheets, Excel, Notion): for households that want full control. Templates available; takes 1–2 hours to set up, 15 min/month to maintain.

- Avoid: apps that aggressively cross-sell credit products, apps that aren’t end-to-end encrypted, apps from companies whose primary business is selling user financial data.

The weekly + monthly review rhythm

- Weekly (10 minutes, Sunday evening): categorize the past week’s transactions, check category balances, decide if next week needs adjustment.

- Monthly (30–45 minutes, end of month): compare actuals vs plan, review savings progress, adjust next month’s plan, check sinking fund balances.

- Quarterly (60 minutes): review trajectory toward annual goals, rebalance investments if needed, audit subscriptions, adjust the budget for major life changes.

- Annually: set next year’s plan, calculate net worth change, review tax efficiency, plan for the year’s irregular expenses.

For broader money context, see my investment diversity guide and side income guide.

Frequently asked questions

What’s the simplest way to balance a personal budget?

The 50/30/20 rule: 50% of after-tax income for needs (rent, utilities, groceries), 30% for wants, 20% for savings and debt payoff. Adjust the percentages for your cost-of-living reality, but the structure works for 80% of households.

How is a household budget different from a business budget?

Household budgets track fixed and variable personal expenses against take-home pay. Business budgets add revenue forecasting, accrual accounting, tax provisions, and capital expenditure planning. The discipline of monthly reconciliation is identical in both.

What budgeting apps actually help?

YNAB (You Need A Budget) for envelope-style discipline, Monarch and Copilot for visual aggregation, Mint replacement Empower for net-worth tracking. In India, Walnut, Money Manager, and ET Money work well; for global expats, Wise plus a Notion template often beats any single app.

How do I balance a budget when income is irregular?

Pay yourself a fixed monthly salary from a buffer account. Save irregular windfalls into the buffer first; draw the salary out predictably. Aim for 3 months of expenses in the buffer before scaling lifestyle.

What’s the biggest budget mistake people make?

Tracking what they spent without setting boundaries on what they will spend. A budget without forward-looking targets is just an expense report. The categories with caps are the categories that change behavior.