Startup Tips: 9 Realistic Business Tips for Emerging Startups

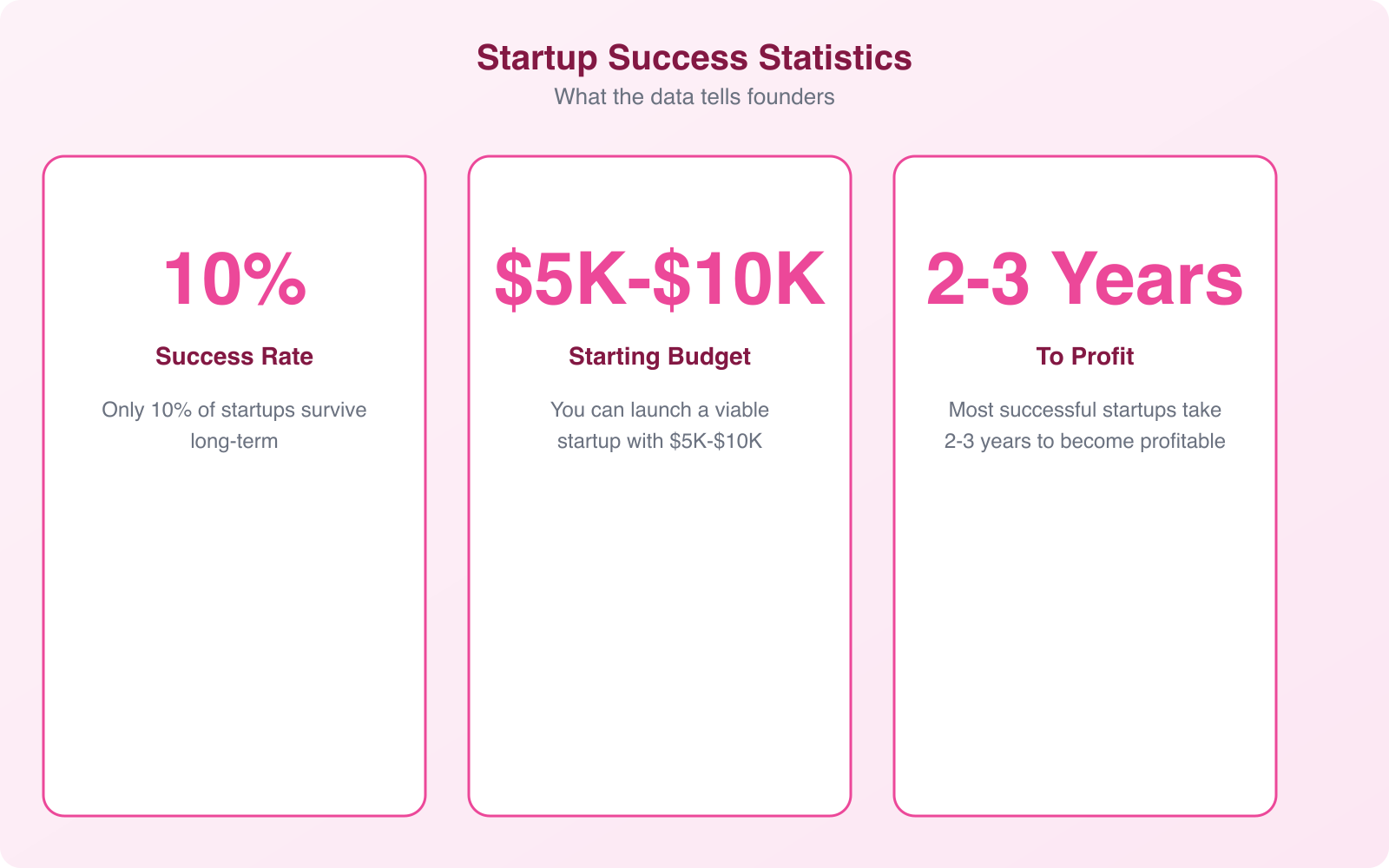

The best startup tips for 2026 aren’t about your idea. They’re about execution. After 18 years and hundreds of launches, my verdict on the business tips for startups that actually move the needle is simple: validate before you build, keep your costs low, own one narrow niche, and watch your cash like your life depends on it. Do those four things and you beat roughly 90% of founders who skip them. Skip them and a great idea won’t save you.

Starting a business sounds exciting until you’re three months in, running on fumes, and wondering why nobody told you it would be this hard. I’ve watched startups crash because the founder had a great idea but no execution plan. I’ve also watched bootstrapped founders with mediocre ideas build profitable companies because they nailed the fundamentals. The difference isn’t talent or luck. It’s discipline.

Here are the startup tips that actually matter when you’re building from scratch. Not the fluffy “follow your passion” advice. The real stuff that separates businesses that survive from the ones that don’t. These are the startup tips and startup advice for new startups that I’d give any early-stage founder sitting across from me at my own desk.

- Who this is for: first-time and early-stage founders bootstrapping a startup on a tight budget, not VC-backed teams with a runway to burn.

- Why trust me: 18 years building online businesses, hundreds of launches advised, and a content business I bootstrapped to profit using the exact channels below.

- The proof that matters: CB Insights data shows 35% of startups die from no market need and 38% from running out of cash. Both are fixable before you write a line of code.

- The tradeoff: this approach is slower than “raise a big round and grow fast.” It trades speed for survival. If you want a moonshot, this isn’t your playbook.

What changed for 2026: AI dropped the cost of building to near zero, so the bottleneck moved from product to distribution. Investors now want a path to positive unit economics within 18 to 24 months, and many founders raise smaller amounts every 12 to 18 months instead of one giant round. AI startups pull nearly half of all VC funding yet fail at an 85 to 90% clip, higher than traditional tech. Translation: building is easy now, getting paid customers is the hard part, and the fundamentals below matter more than ever.

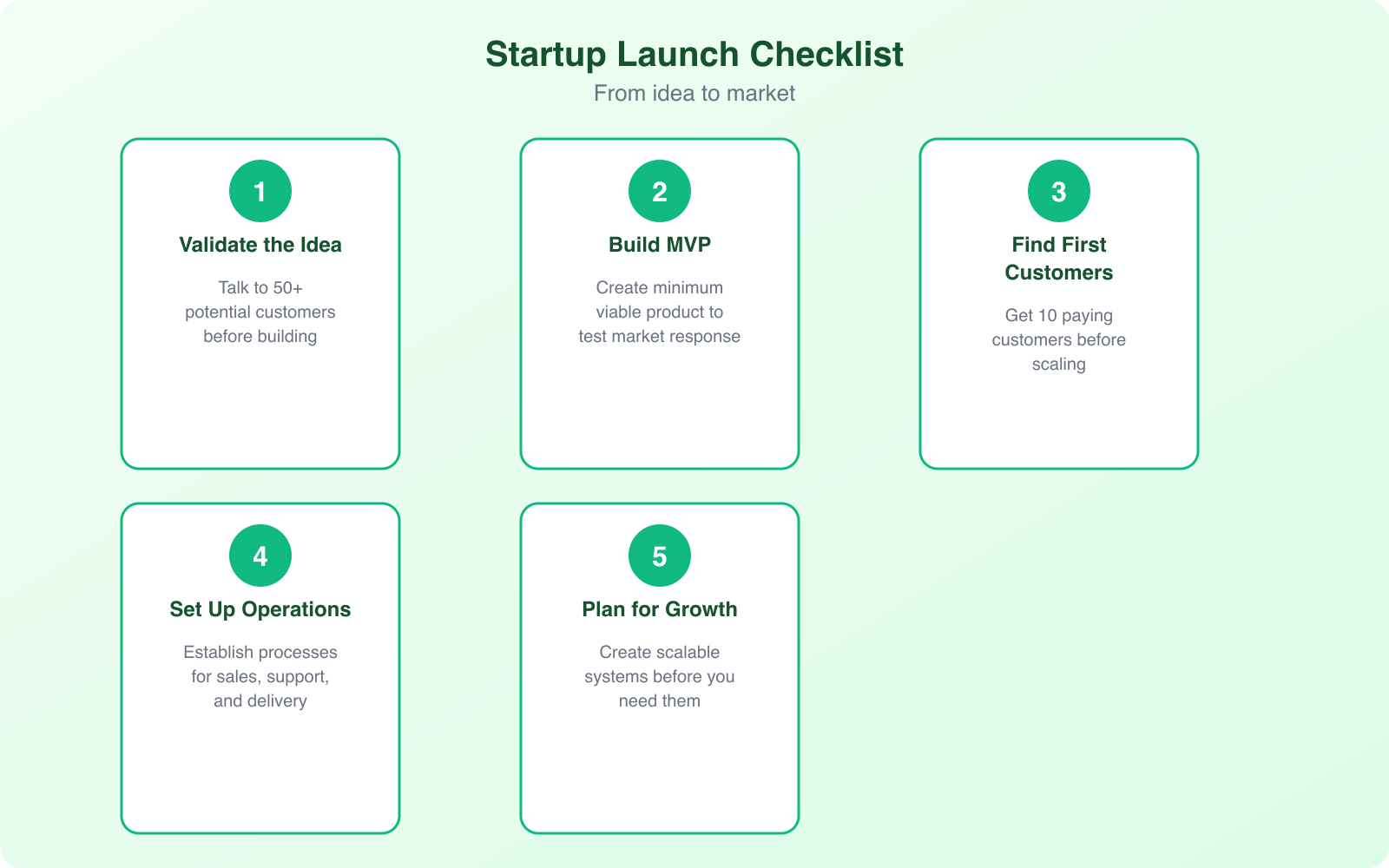

Validate Your Idea Before You Build Anything

The single biggest mistake I see new founders make is spending months (and thousands of dollars) building a product nobody wants. They fall in love with their idea, assume the market agrees, and skip the validation step entirely. Then they launch to crickets.

Here’s what validation actually looks like. Talk to 30 potential customers. Not your friends. Not your family. People who fit your target market. Ask them about the problem you’re solving. Ask how they currently deal with it. Ask what they’d pay for a better solution. If the majority don’t care about the problem, you’ve just saved yourself a year of wasted effort.

Better yet, pre-sell. Create a landing page describing your product, set a price, and see if people will put down a deposit or pre-order. If 10% of visitors convert, you have something. If nobody bites, go back to the drawing board.

The lean startup methodology popularized by Eric Ries gets this right: build a minimum viable product (MVP), test it with real users, measure the results, and iterate. Don’t build the full product first. Build the smallest version that proves people will pay for it.

Here’s the startup mistake most founders still ignore in 2026: they validate the product and forget to validate the channel. AI made building so cheap that a working MVP no longer proves much. The real question is whether you have one scalable, repeatable way to reach paying customers. The founders who win pick a single distribution channel and push it to the extreme before touching a second. If you can’t name how customer #100 finds you, you haven’t validated anything yet. If your launch already feels stuck, my breakdown of why a small business struggles to take off walks through the usual culprits.

Begin With a Strong Strategy, Not a Perfect Plan

Your business plan doesn’t need to be 50 pages. At the startup stage, it needs to answer five questions clearly: What problem are you solving? Who are you solving it for? How will you make money? How will you reach customers? What does success look like in 12 months?

Write this down in one page. Seriously, one page. The specifics will change as you learn, and that’s fine. The plan is a starting point, not a contract.

What matters more than the plan itself is the thinking behind it. Most startups fail because the founder never forced themselves to answer hard questions upfront. “Who will pay for this?” is a hard question. “How much will they pay?” is harder. “Why will they choose me over the 10 competitors already in this space?” is the hardest. If you can’t answer these clearly, you’re not ready to launch.

Use the Lean Canvas instead of a traditional business plan. It’s a one-page framework that covers problem, solution, key metrics, unique advantage, channels, customer segments, cost structure, and revenue streams. You can fill it out in 20 minutes and update it weekly.

Define Your Vision and Stay Flexible

A clear vision keeps you focused when things get chaotic. And things will get chaotic. You need a north star that guides every decision: who you’re building for, what outcome you’re creating, and why it matters.

But here’s the thing most startup advice gets wrong: your vision should be fixed, but your strategy should be flexible. Instagram started as a check-in app called Burbn. Slack started as an internal tool for a gaming company. Twitter was a side project from a podcasting platform. The vision stayed (connect people), but the product changed dramatically.

Be willing to pivot when the data tells you to. If your original idea isn’t gaining traction after 3-6 months of genuine effort, look at what is working and follow that signal. Some of the best businesses started as something completely different.

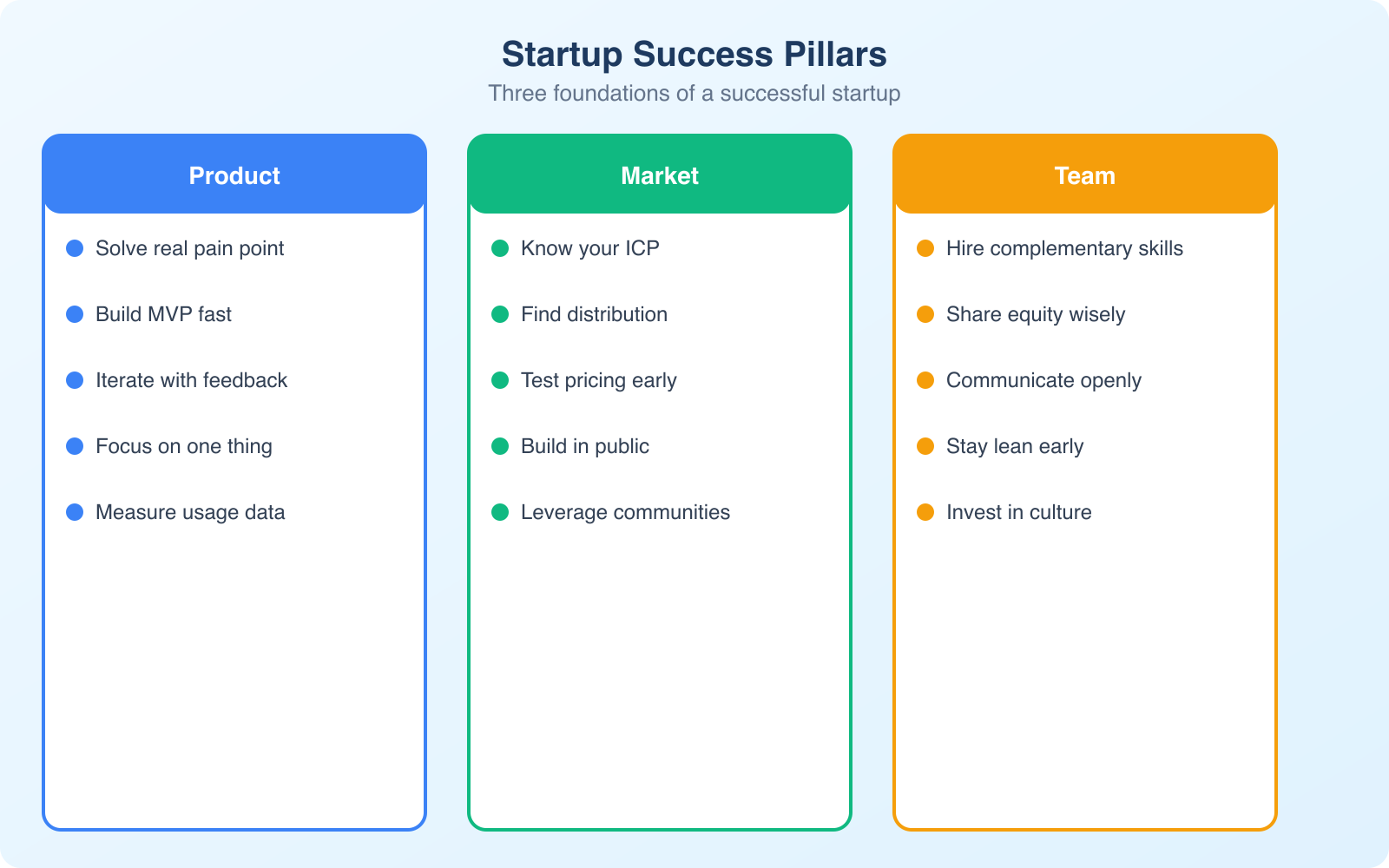

Identify and Own Your Market Niche

Competing with established players in a broad market is a losing game for a startup. You don’t have their budget, their brand recognition, or their customer base. What you do have is the ability to be more specific and more focused than they are.

Find a niche that’s small enough to own but large enough to sustain a business. A project management tool for “everyone” competes with Monday.com, Asana, and Trello. A project management tool for “freelance designers managing client projects” has a clear audience, specific pain points, and virtually no competition.

The right niche has three characteristics. First, people in it are already spending money to solve the problem. Second, you can reach them through specific channels (communities, publications, conferences). Third, it’s big enough to support your revenue goals. If your niche has fewer than 10,000 potential customers and you need 1,000 of them to pay $50/month to hit your targets, the math probably doesn’t work.

Design a Business Model That Scales

Your business model is how you make money. It sounds simple, but I’ve met founders who couldn’t clearly explain their revenue model when asked. There are a few common models for startups, and picking the right one matters.

Subscription/SaaS: Customers pay monthly or annually for access. Great for recurring revenue and predictable cash flow. The challenge is reducing churn.

Marketplace: You connect buyers and sellers and take a commission. The challenge is the chicken-and-egg problem of needing both sides of the market.

Services: You sell your time and expertise. Easy to start, hard to scale because revenue is tied to hours worked. The path to scaling is productizing your services.

E-commerce: You sell physical or digital products. Revenue is transactional, and the challenge is customer acquisition costs and margins.

The key question: can your model grow revenue without proportionally growing costs? If doubling your customers requires doubling your team, you’re building a job, not a scalable business. Look for ways to serve more customers without adding more overhead.

Marketing on a Tight Budget

You don’t need a big budget to get your first 100 customers. You need hustle and focus. This is where most startup advice goes soft, so I’ll be specific. For a deeper playbook, my guide to effective customer acquisition strategies for startups pairs well with the channels below. Here’s what works when you’re bootstrapping.

Content marketing: Write blog posts, create videos, or start a podcast that speaks directly to your target audience. It costs nothing but your time, and it compounds over time. One well-written article can bring in traffic for years. This is how I’ve built most of my own audience.

Community involvement: Go where your customers already hang out. That might be Reddit, Facebook Groups, Discord servers, or industry forums. Don’t spam. Add value. Answer questions, share insights, and build genuine relationships. People buy from people they trust.

Cold outreach: For B2B startups, personalized emails to potential customers still work incredibly well. The key is personalization. “Hi [name], I noticed you [specific thing about their business]” converts at 10x the rate of generic templates.

Partnerships: Find businesses that serve the same audience but aren’t competitors. Offer to co-create content, run a joint webinar, or cross-promote. This gives you access to their audience without spending a dollar on ads.

Email marketing: Start building an email list from day one. Email marketing consistently delivers the highest ROI of any marketing channel. Most platforms are free up to 1,000 subscribers. Use it.

Build Your Team and Network Early

You can’t build a great company alone. At some point, you’ll need co-founders, employees, advisors, or contractors. The mistake most founders make is waiting until they’re desperate to start looking.

Start networking before you need anything. Attend industry events. Join online communities. Reach out to people you admire and ask for 15 minutes of their time. Most successful entrepreneurs are surprisingly generous with their time if you approach them with genuine curiosity instead of a sales pitch.

When it comes to hiring, culture matters more than credentials at the early stage. Your first 5 employees will define the DNA of your company. Look for people who are self-motivated, adaptable, and comfortable with ambiguity. You can teach skills. You can’t teach hustle.

Can’t afford full-time hires? Start with freelancers and contractors for specific projects. Platforms like Upwork and Fiverr let you test working relationships before committing to a full hire. Use freelancer management tools to keep everything organized.

Manage Your Money Like Your Business Depends on It

Because it does. Cash management is the #1 reason startups die. Not bad products. Not lack of demand. Running out of money.

Here are the financial rules I recommend for every startup founder.

Keep your personal and business finances completely separate. Open a business bank account and never mix funds. This makes accounting easier and protects you legally.

Track every expense from day one. Use accounting software like QuickBooks or Wave. Know your burn rate (how much cash you spend per month) and your runway (how many months of cash you have left).

Keep 6 months of operating expenses in reserve if possible. If you can’t afford that, start with 3 months and build from there. This buffer gives you time to adjust when things don’t go as planned. The flip side of building a buffer is spending less to begin with, so it’s worth knowing the simple ways to reduce start-up costs before you commit to any recurring expense.

Don’t raise funding until you’ve validated your idea. Taking investment money before you have product-market fit means you’ll burn through it faster than you expect, and you’ll give away equity too early at a low valuation.

Use the Right Tools from Day One

You don’t need 20 SaaS subscriptions. You need 4-5 core tools that cover your essential operations. Of all the startup tips here, this is the one founders overspend on the fastest.

Project management: Use Trello (free) or Notion (free) to organize tasks, deadlines, and team workflows. Don’t rely on sticky notes and memory.

Communication: Slack’s free tier handles most startup needs. Keep conversations organized by topic instead of buried in email threads.

Accounting: Wave is free for basic accounting. QuickBooks starts at $15/month. Pick one and use it from day one. Catching up on 6 months of bookkeeping is miserable.

Website: WordPress is free and powers 43% of the web. For a simple landing page, Carrd costs $19/year. Don’t overthink your website at the start. A clean single page that explains what you do and how to buy is enough.

Analytics: Google Analytics and Google Search Console are free. Install them before you launch so you have data from day one.

The bottom line: you can run a startup’s full tech stack for under $35/month. Don’t let tool costs become an excuse for not starting.

Startup Tips for Avoiding First-Year Mistakes That Kill Startups

I’ve watched enough startups fail to spot the patterns. These are the mistakes I see most often in the first 12 months, and they’re all avoidable. Before the list, here’s what the 2026 data actually says is killing startups, so you can aim your effort at the failures that matter most.

| Top reason startups fail (2026) | Share of failures | What fixes it early |

|---|---|---|

| No market need | ~35% | Talk to 30 buyers and pre-sell before building |

| Ran out of cash / pricing | ~38% | Track burn and runway weekly from month one |

| Wrong team / culture | ~30% | Hire for hustle and adaptability, not credentials |

| Weak distribution / customer acquisition | ~28% | Own one repeatable channel before scaling |

| Got outcompeted | ~20% | Pick a niche too narrow for incumbents to bother |

Hiring too early. Many founders hire before they have consistent revenue. Every employee is a fixed cost that doesn’t pause when sales slow down. If your monthly revenue is $5,000 and you hire someone at $4,000/month, one bad month puts you in the red. Use freelancers and contractors until your revenue consistently covers payroll with a 30% buffer.

Building features nobody asked for. It’s tempting to keep adding to your product. Resist it. Every feature you build costs time and money to maintain. Talk to your customers weekly. Build what they’re asking for, not what you think they need. The fastest way to waste 3 months is to build a feature, launch it, and discover nobody uses it.

Ignoring unit economics. If it costs you $100 to acquire a customer who pays you $50, you’re losing money on every sale. It sounds obvious, but I’ve seen startups burn through $50,000+ before they realized their customer acquisition cost (CAC) was higher than their customer lifetime value (LTV). Calculate these numbers in month one and track them weekly.

Copying competitors instead of understanding customers. Watching what competitors do is smart. Blindly copying them is not. You don’t know why they made those choices, and their customers aren’t necessarily your customers. Focus on understanding your specific audience’s pain points and build solutions tailored to them.

Trying to do everything alone for too long. Being scrappy is great. Being a martyr isn’t. If you’re working 80-hour weeks and your business isn’t growing, you don’t need to work harder. You need to work smarter. Identify the tasks that only you can do, and delegate or automate everything else. Check out these best apps for small business to streamline the repetitive stuff.

Building a startup is hard. There’s no way around that reality. But most of the hard things aren’t mysteries. They’re fundamentals that you execute consistently. Validate your idea. Keep your costs low. Focus on one market. Build relationships. Track your numbers. Avoid the first-year mistakes that kill most businesses. Do these things well, and you’ll be ahead of 90% of founders who skip them. That’s the honest version of business tips for startups, no shortcuts attached. If you’re still at square one, my step-by-step guide to how to start a new business covers the setup decisions that come before everything here.

Frequently Asked Questions

How much money do I need to start a business?

It depends entirely on the type of business. A service-based business (consulting, freelancing, coaching) can start for under $500. An e-commerce business might need $2,000-5,000 for inventory and a website. A SaaS product could require $5,000-20,000 for development. Start with the minimum viable version and reinvest profits to grow.

Should I quit my job to start a startup?

Not until you’ve validated the idea and have either 6 months of savings or early revenue coming in. Many successful startups were built as side projects first. Test the waters while you still have a steady paycheck. Quit when the startup demands full-time attention and the numbers support it.

How long does it take for a startup to become profitable?

Service businesses can become profitable in 1-3 months if you already have a skill to sell. Product businesses typically take 6-18 months. SaaS businesses often take 12-24 months to reach profitability. The key variable is how quickly you find product-market fit and how low you can keep your costs during the early stage.

Do I need a co-founder?

Not necessarily. Solo founders can succeed, especially in service businesses and bootstrapped startups. A co-founder helps when the business requires complementary skills (one technical, one business), when the workload is too much for one person, or when you need accountability and emotional support. Pick a co-founder carefully though. Bad partnerships destroy more startups than bad products.

What’s the best marketing channel for a new startup?

There’s no universal best channel. It depends on your audience. For B2B startups, cold email and LinkedIn tend to work best. For B2C, content marketing and social media perform well. For local businesses, Google Business Profile and local SEO are most effective. Start with one channel, measure results for 30-60 days, then decide whether to double down or try something else.

Disclaimer: This site is reader-supported. If you buy through some links, I may earn a small commission at no extra cost to you. I only recommend tools I trust and would use myself. Your support helps keep gauravtiwari.org free and focused on real-world advice. Thanks. - Gaurav Tiwari