What is PFMS? Significance & Benefits of PFMS

If you’ve ever wondered why your government scholarship or subsidy payment is delayed, the answer usually involves PFMS. The Public Financial Management System is the platform that every central government payment passes through before it reaches your bank account, from PM-KISAN installments to NSP scholarships to MGNREGS wages.

The problem is that most beneficiaries have no idea how to check their payment status, why a transfer failed, or what “PFMS” even means when they see it on a bank statement. Government portals aren’t exactly user-friendly, and the documentation assumes you already understand how fund flow works.

This guide breaks down what PFMS actually does, how it tracks every rupee from the central government to your bank account, and exactly how to check your payment status on pfms.nic.in. No jargon, no assumptions.

What is PFMS?

PFMS is a flagship reform initiative of the Ministry of Finance designed to bring India’s complex web of schemes and subsidies under a single digital roof. At its core, PFMS tracks every rupee released under Central Sector and Centrally Sponsored schemes, capturing how funds are allocated, released and spent. This granular view helps policymakers and citizens see which programs are working and where money is being deployed.

By providing real-time dashboards and reports, PFMS ensures that money invested in social and development programs reaches its intended beneficiaries. It enables the government to monitor budget utilisation at each stage of implementation and quickly identify bottlenecks or anomalies.

All of this budgeting data is anchored in the Controller General of Accounts’ accounting system, making PFMS the official source for consolidated financial records across ministries and states.

Before PFMS, India’s accounting system struggled to support effective monitoring, consolidated reporting and planning. The existing processes were fragmented and manual. PFMS was conceived to fix those gaps by offering a transparent, digital ledger that unifies budgeting, accounting and payments.

Since its launch it has been rolled out across all central ministries and state governments. The project’s innovation even earned the Microsoft Developer Innovation & Excellence Award back in 2009.

PFMS integrates with the core banking systems of over 150 banks across India, acting as the central management information system for all Direct Benefit Transfer (DBT) transactions. This integration supports fast, secure and error-free fund transfers.

More than eight hundred thousand implementing agencies and grantee institutions are registered on PFMS, ensuring accountability and traceability for each release.

Ultimately, the goal is to produce state-wise and scheme-wise statements that show how funds under centrally sponsored schemes are allocated, transferred and used, enabling better decision-making and preventing misuse.

Why PFMS was formed?

Before PFMS existed, India had no reliable way to track over Rs. 25 lakh crore released annually across hundreds of welfare schemes. Money left New Delhi but the central government couldn’t tell whether it arrived, sat idle in district accounts, or was diverted entirely. Reports were delayed by weeks, sometimes months. By the time the data reached central authorities, it was already outdated.

India runs hundreds of welfare schemes and development programs across multiple sectors, from rural employment (MGNREGS) to housing (PMAY) to farmer income support (PM-KISAN). The central government releases huge sums every year and needs to ensure those funds reach the intended beneficiaries. PFMS was established to keep a watchful eye on this flow of capital and to make budgeting more efficient. By centralizing payments and tracking, PFMS gives both administrators and ordinary citizens assurance that tax money is being spent wisely.

Earlier management information systems couldn’t give an accurate, real-time picture of where funds were utilised. Reports were delayed and often incomplete, making it hard for the government to know if money remained unused or had been diverted. PFMS addresses this by providing live information on fund transfers, bank balances across districts and scheme-wise utilisation details.

That gap led to the creation of PFMS as a mandatory mechanism for transparent public financial management. With PFMS in place, the government can plan better, respond quickly to changes on the ground and ensure that programmes deliver real impact.

How PFMS Works

PFMS operates as the single payment backbone for every central government scheme. Here’s the payment flow from allocation to your bank account, step by step:

- Ministry releases funds. A central ministry (say, the Ministry of Agriculture for PM-KISAN, or the Ministry of Rural Development for MGNREGS) approves a budget release and generates a sanction order inside PFMS. The system creates a unique sanction ID linked to the specific scheme and beneficiary pool.

- PFMS routes through an accredited bank. The payment instruction travels electronically through PFMS to one of its 150+ integrated bank partners. PFMS does not hold funds itself. It is the routing and tracking layer sitting between the government and the banking system. Every transfer is logged in real time against the scheme and the sanctioning ministry.

- Implementing agency receives credit. The sanctioned amount hits the bank account of the implementing agency, whether that’s a state government department, a district-level body, a Gram Panchayat, or an autonomous institution. For a programme like PMAY (Pradhan Mantri Awas Yojana), this might be the state housing board. For NSP (National Scholarship Portal), it could be a college or university. The agency can view the receipt instantly on the PFMS dashboard.

- Beneficiary receives DBT transfer. For direct benefit transfer schemes like PM-KISAN or MGNREGS, the final leg bypasses the implementing agency entirely. PFMS pushes the payment directly to the beneficiary’s Aadhaar-seeded bank account via NPCI’s DBT infrastructure. The transfer is recorded in real time, the beneficiary gets an SMS alert, and the central system marks the transaction as settled. No middleman. No cash. No delay.

This end-to-end digital trail is why PFMS is described as “just-in-time” fund release. Money moves only when it is needed, which reduces idle float sitting in intermediate accounts and cuts the government’s borrowing costs.

What PFMS Achieves

PFMS delivers results across three distinct groups: the central government and its departments, ordinary citizens, and state governments. The impact looks different for each. Here’s how it breaks down.

Government Bodies

PFMS gives central ministries and implementing agencies a live command view of every rupee in motion. That changes how government bodies plan, audit, and execute schemes.

- PFMS ensures transparency by routing every rupee through accredited banks and linking the bank accounts of implementing agencies to a central portal. Every transaction, down to the last paisa, is recorded and visible to the central government, building trust and confidence in public finance.

- The system eliminates inconsistencies and delays in fund flow, reducing the scope for mismanagement. By providing clear audit trails and near real-time reconciliations, PFMS helps auditors keep a close eye on how funds are being used.

- To ensure funds are used as intended, PFMS establishes implementing agencies at the state, district and grassroots levels that are accountable for every rupee. These entities track receipts and expenditures, detect bottlenecks and flag underutilization or misappropriation before money is wasted.

- PFMS streamlines the release of grants and subsidies to NGOs, autonomous bodies and government ministries. Instead of sending cheques through the post, the system electronically credits registered bank accounts of agencies and beneficiaries, leaving no room for middlemen to siphon off funds.

- Traditionally, finance systems only booked the release of funds but rarely tracked how those funds were spent. PFMS mandates recording of actual utilization and outcomes, fostering a culture of accountability and ensuring taxpayers see real results for their money.

- By minimizing idle balances in bank accounts, PFMS improves cash and debt management. The system tightens fund flow and schedules transfers just when needed, which reduces borrowing costs and improves the government’s financial health.

- PFMS automates the creation of sanction orders. This reduces manual data entry and the associated errors, saving time for government staff and ensuring sanctions are generated quickly and accurately. Comprehensive reports track pending, issued and settled sanctions in real time.

- The system clearly distinguishes between funds allocated, funds released and actual expenditure. Policymakers can see at a glance how much was sanctioned, how much was disbursed, and how much was spent on the ground. Under PMGSY (Pradhan Mantri Gram Sadak Yojana), for instance, every road construction payment is tracked against the specific district sanction.

- PFMS flags agencies, including NGOs, that receive grants from multiple schemes or departments. This oversight prevents double-dipping and ensures funds are distributed equitably.

Citizens

PFMS empowers ordinary citizens with direct visibility and control over government welfare funds. If you’re a PM-KISAN beneficiary, an NSP scholarship recipient, or a MGNREGS wage earner, PFMS is the system that puts money in your account and lets you verify it arrived.

- Registered citizens receive real-time alerts when funds are released to government facilities in their area. The alerts specify the amount, purpose and scheme, so residents know what’s planned for their community.

- PFMS supports direct payments under social sector schemes and conditional cash transfers. Money goes straight from the treasury to beneficiaries’ bank accounts, cutting out middlemen and reducing corruption.

- Citizens can self-register on the PFMS portal by providing basic details and their geographical location. This allows them to track benefits, verify transactions and participate in local monitoring.

- PFMS supports multiple payment modes including demand drafts, cheques, RTGS, ECS, online banking and printed advice. This flexibility accommodates users with varying levels of digital access.

The Citizen Information Portal offers an easy-to-use dashboard that displays state-wise releases, district-wise releases, scheme-wise details, agency registrations and investment data. Residents can quickly see where money is being deployed and hold authorities accountable.

- State-wise releases

- District-wise releases

- Agency-wise releases

- Scheme-wise releases

- Information of all agencies registered

- Millennium development goals investment

- Sector-wise investment

- Flagship scheme investment

State Governments

- PFMS gives state governments a unified dashboard showing every planning grant they receive via treasury transfers, special purpose vehicles, societies, autonomous bodies, NGOs and individuals registered in the state. This level of detail helps officials plan budgets, forecast cash flows and ensure that no funds fall through the cracks.

- It enables full implementation, monitoring and management of schemes at every level, making the entire programme lifecycle from sanction to execution visible online. Administrators can track progress, check compliance and troubleshoot issues without wading through paper records.

- The system offers transparent, searchable lists of all grants received from central ministries under various schemes, including PMAY central releases to state housing departments and PMGSY allocations to state rural development bodies. States can quickly verify the amount, date and purpose of each transfer and align it with local spending priorities.

- At the district and block level, agencies can generate unique sanction IDs and component-wise investments within PFMS. These IDs are integrated with banking transactions and updated in real time, allowing finance officers to track each rupee from sanction to utilisation.

How to Check Your PFMS Payment Status

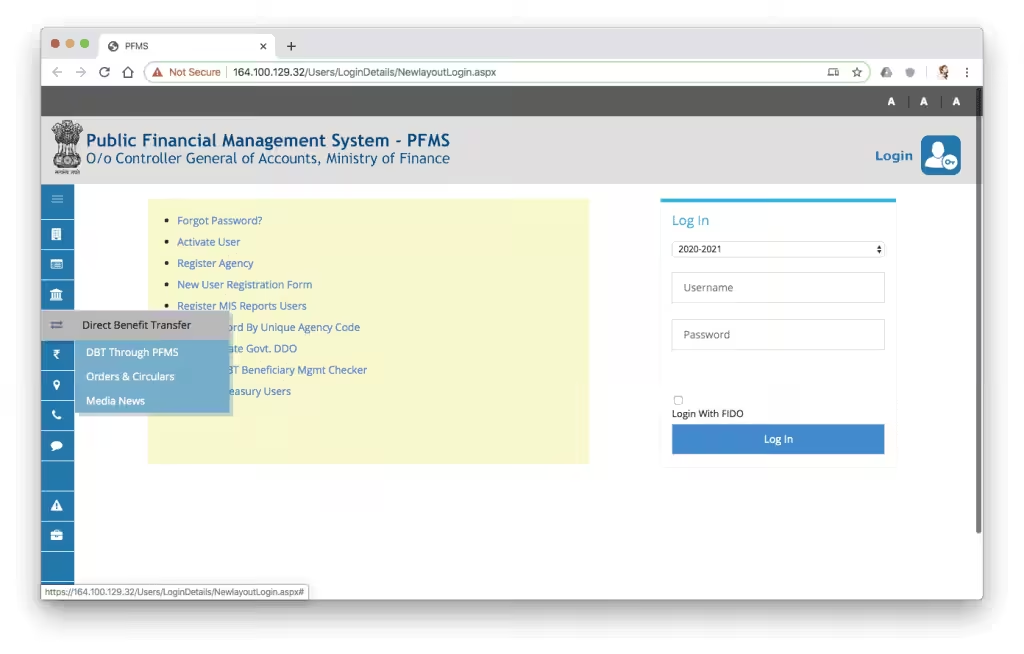

If you’re waiting on a PM-KISAN instalment, an NSP scholarship disbursement, or any other government DBT transfer, you can check its status directly on pfms.nic.in in under two minutes. Here’s how.

- Visit the official PFMS portal. Open your browser and go to pfms.nic.in. The homepage loads the national dashboard showing aggregate fund flow data.

- Click “Know Your Payments”. Look for the “Know Your Payments” link in the top navigation or on the homepage panel. This takes you to the beneficiary payment search page.

- Enter your bank account or Aadhaar number. You’ll see two lookup options. Enter your bank account number along with the bank name, or use your Aadhaar number if your account is Aadhaar-seeded. Enter the captcha code shown on screen.

- View your transaction history. Hit Search. The system will pull up a list of all DBT transactions linked to your account across every scheme, including the scheme name, amount, date, and payment status. If a transfer is pending, it shows as “Initiated.” If it’s landed in your account, it shows as “Paid” with the exact value date.

One thing to note: PFMS data updates with a slight lag on some schemes. If your bank shows a credit but PFMS hasn’t updated yet, wait 24 hours before calling the helpline. The portal also lets registered users log in at pfms.nic.in/Users/FidoLogin.aspx to manage their accounts, track transactions, generate reports and update agency or beneficiary details.

सरकारी लाभ पाने के लिए।

PFMS

PFMS scheme kya hai aur iska benefit kaun aur kaise le sakta hai?

main confused hu kyonki payment kaise hoga sirf itna btaya gya hai lekin mere samjh me ye nahi aa rha ki pfms ke through kisi ke account me maine 800-2200 tak payment aaya hai. kabhi kabhi lagatar do din payment aaya hai kaise? samajhayiye.

Thanks for sharing this information , its detailed and too good since you have shared the screenshots of the entire method involved in the process . This is really good . Helpful !!

I have noticed that of all forms of insurance, health care insurance is the most questionable because of the turmoil between the insurance coverage company’s obligation to remain adrift and the client’s need to have insurance plan. Insurance companies’ revenue on health plans are extremely low, hence some corporations struggle to generate income. Thanks for the suggestions you discuss through this blog.