Investing Basics for Beginners (India): The Boring Portfolio That Works

Most beginner investing guides in India tell you to “understand your risk tolerance” and “consider asset allocation.” That’s not advice. That’s a textbook reading itself out loud. The reason your parents kept their money in fixed deposits for thirty years wasn’t laziness. It was that nobody handed them a simple, honest rulebook for what to do instead. This article is that rulebook, written for the version of you that just got a salary account and has no idea what to do with the money sitting there.

I’ll get to the boring stuff in a minute. Definitions, asset classes, the ten things every guide opens with. But before we go there, here’s the version of investing that’s actually worked for me and the people I’ve talked into it: a Nifty 50 index fund for the bulk of your equity, two or three active funds around it, direct plans only, three to five funds total, a ₹500 minimum SIP, and an emergency fund that comes first. That’s the entire game. Everything below is the why and the how.

Why most “beginner investing” guides fail Indians

Most beginner investing guides on the internet were written for an American audience and lazily copy-pasted for India. You can spot them within two paragraphs. They mention 401(k), IRA, FDIC insurance up to $250,000, and Vanguard. None of that helps you. You don’t have a 401(k). Your bank deposits are insured by DICGC up to ₹5 lakh, not the FDIC. Vanguard doesn’t sell direct mutual funds in India. So when a guide tells you to “max out your IRA before investing in taxable accounts,” it’s not even wrong. It’s irrelevant.

Look, the underlying ideas (compound, diversify, stay invested) translate fine. The implementation does not. SEBI is not the SEC. ELSS is not a Roth IRA. A SIP is not a 401(k) deduction. So this guide is written for the rules you actually live under, with the funds and platforms you can actually use. If you’re an NRI investing back home, most of it still applies. If you’re outside India entirely, the framework holds; the names won’t.

Investing basics: the only definitions you actually need

You don’t need to memorize a glossary. You need eight terms. Read them once, then move on.

- Asset. Anything that produces income or grows in value. Stocks, bonds, real estate, gold. Your phone is not an asset.

- Equity. Ownership in a company. Stocks. Equity mutual funds. ETFs that hold stocks. High return, high volatility.

- Debt. Lending money to someone (a government, a company, a bank) for a fixed return. Bonds, debt mutual funds, FDs. Lower return, lower volatility.

- Portfolio. Your full collection of investments. Three funds is a portfolio. Twenty-three funds is a museum.

- Risk. The probability that you don’t get the return you expected, or you lose money. Equity has more of it than debt. Crypto has more of it than equity.

- Return. Profit, expressed as a percent of what you put in. Annualized over time, this becomes CAGR (compound annual growth rate).

- Expense ratio (TER). The annual fee a mutual fund charges, taken out of your returns. UTI Nifty 50 Index Fund charges 0.18%. Some active funds charge 1.8%. That difference compounds against you for decades.

- NAV. Net Asset Value. The “price” of one unit of a mutual fund on a given day. NAV alone tells you nothing. Two funds with NAV ₹50 and ₹500 can have identical returns.

That’s it. If a glossary article makes you read forty more, close the tab.

Why FDs lose to inflation (the math your bank won’t show you)

A fixed deposit at a major Indian bank pays around 6.5% to 7.5% pre-tax in 2026. That sounds reasonable until you do two pieces of arithmetic the bank’s marketing team would rather you skipped.

First, tax. FD interest is added to your income and taxed at your slab. If you’re in the 30% slab, a 7% FD becomes a 4.9% post-tax return. Second, inflation. Indian retail inflation has averaged around 5% to 6% over the last decade. So that 4.9% post-tax return, after inflation, is roughly zero. You worked for a year, paid tax on the interest, and gained nothing in real purchasing power.

A ₹10 lakh FD at 7% pre-tax, held for 20 years by a 30%-slab investor, grows to about ₹26 lakh in nominal terms. The same ₹10 lakh in a Nifty 50 index fund at the historical 12% CAGR, held for 20 years, grows to about ₹96 lakh. The difference is not 2x. It’s 4x. That gap is the price of “safety.”

FDs aren’t useless. They’re fine for an emergency fund, fine for goals less than 12 months away, fine if your slab is below 20%. As a default home for long-term wealth? They are how middle-class India quietly stayed middle-class while the people who held equities moved up. That’s the uncomfortable truth your bank manager won’t put on a brochure.

Build your emergency fund before the first SIP

Before any equity SIP, before any tax-saving fund, before any “I’ll just put 5% in crypto,” you need an emergency fund. Six months of expenses, parked somewhere you can pull from in two business days without losing money on a market dip. This is rule one because it’s the rule that prevents every other rule from breaking.

Why six months? Because that’s roughly how long it takes to find a new job in a downturn, recover from a hospital stay, or wait out a freelancing dry patch. If your monthly expenses are ₹40,000, you need ₹2.4 lakh sitting in a liquid place. Not in equity. Not in a tax-saver locked for three years. Liquid.

Two acceptable homes: a sweep-in fixed deposit linked to your savings account, or a liquid fund like Nippon India Liquid or HDFC Liquid Fund. Liquid funds redeem in T+1 day, are taxed at slab (so the 30% slab investor barely beats a sweep FD), but give you 6.5% to 7% with zero penalty for early withdrawal. Pick whichever you’ll actually leave alone.

If you start equity SIPs without an emergency fund, you will eventually hit a month where rent is due, a market correction has just hit, and your only liquid money is in a fund that’s down 18%. That’s the moment people redeem at the bottom and never recover. The emergency fund is what keeps you invested through the bad months.

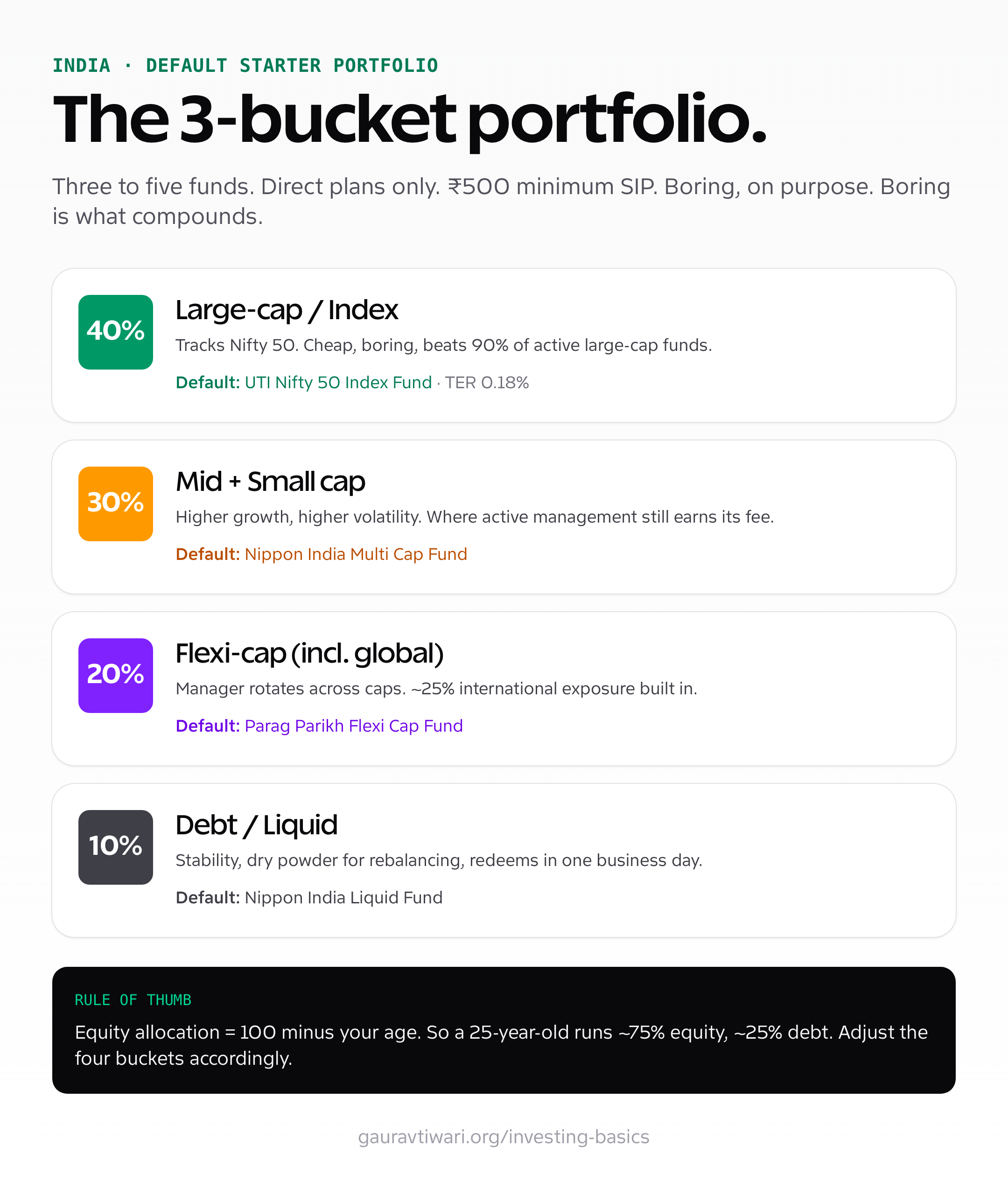

The 3-bucket portfolio I default to for first-time investors

Once your emergency fund is set, here’s the portfolio I’d hand a 25-year-old with ₹15,000 a month to invest. It’s boring on purpose. Boring is what compounds.

| Bucket | Allocation | What it does | Default fund |

|---|---|---|---|

| Large-cap / Index | 40% | Tracks Nifty 50. Boring, cheap, beats most active large-caps. | UTI Nifty 50 Index Fund |

| Mid + Small cap | 30% | Higher growth, higher volatility. Where active management still earns its fee. | Nippon India Multi Cap Fund |

| Flexi-cap (incl. global) | 20% | Manager chooses across caps. Adds international exposure. | Parag Parikh Flexi Cap Fund |

| Debt / Liquid | 10% | Stability, dry powder for rebalancing. | Nippon India Liquid Fund |

The split shifts with age and risk tolerance. A common rule: equity allocation = 100 minus your age. So a 25-year-old runs 75% equity, 25% debt. A 55-year-old runs 45% equity. The rule isn’t precise, but it’s better than no rule.

Notice what’s not in the table. There’s no “international fund” line item, because Parag Parikh’s flexi-cap already holds about 25% international (Alphabet, Meta, Microsoft). There’s no separate gold fund, because at this size gold doesn’t move the needle. There’s no sectoral fund, because sectoral bets are how beginners convince themselves they have stock-picking skill. Three to five funds. Total. That’s the sweet spot.

Equity: index funds first, active funds second

The index-vs-active debate is mostly settled in large-cap. SPIVA India Scorecard data shows that roughly 90% of actively managed large-cap funds fail to beat the Nifty 50 over rolling 5-year periods. Pay 1.5% TER for a 90% chance of underperforming a 0.18% TER index fund. The math doesn’t work.

So your large-cap money goes into a Nifty 50 or Sensex index fund. UTI Nifty 50 Index Fund and Nippon India Nifty 50 Index Fund are the two cheapest and most liquid. Either is fine. If you have strong views on the next-50 stocks, add UTI Nifty Next 50 as a 5% to 10% slice; otherwise skip it.

Active funds still earn their fee in the messier corners of the market. Mid-cap and small-cap stocks are followed by fewer analysts, mispriced more often, and a good fund manager can genuinely add value. The same goes for flexi-cap, where the manager can rotate between caps. So the rule is: index your large-cap, active-manage your mid/small/flexi. Not the other way around.

Default equity stack: 40% UTI Nifty 50 Index, 30% Nippon India Multi Cap (or a small-cap like Quant Small Cap if you can stomach it), 20% Parag Parikh Flexi Cap, 10% liquid. Direct plans, all of them.

Debt: where to park money you’ll need in 1 to 5 years

Debt funds are misunderstood. People hear “debt” and think “safe.” Then they get a credit-risk fund that lost 12% in a week and decide debt is a scam. The category matters more than the asset class.

For money you’ll need in under 12 months, use a liquid fund. For 1 to 3 years, a short-duration fund (like HDFC Short Term Debt Fund or Axis Short Term Fund). For 3 to 5 years, a corporate bond fund or banking and PSU debt fund. Avoid credit-risk funds entirely unless you genuinely understand what you’re buying. The extra 1% yield is not worth the tail risk.

One thing that changed in 2023 and trips up beginners: indexation benefits on debt funds were removed. Debt fund gains are now taxed at your slab rate, regardless of how long you hold them. So for a 30%-slab investor, a debt fund returning 7% becomes 4.9% post-tax. That’s the same math as an FD. The advantage debt funds have over FDs is now mainly liquidity and the option to switch funds without breaking a deposit. The tax advantage is gone.

Tax-saving (Section 80C) without a 15-year lock-in

If you’re on the old tax regime, Section 80C gives you a ₹1.5 lakh annual deduction. The classic options are PPF, ELSS, NPS, life insurance, and a few others. Most people pick PPF because their parents picked PPF. PPF is fine. It’s also dramatically suboptimal for anyone under 40.

| Option | Lock-in | Recent return | Risk | Best for |

|---|---|---|---|---|

| ELSS (equity tax-saver fund) | 3 years | 13–17% CAGR (10-yr) | Equity volatility | Anyone under 40 with stomach for drawdowns |

| PPF | 15 years (partial after 5) | 7.1% (govt-set) | Effectively zero | Risk-averse savers, retirement bucket |

| NPS Tier 1 | Until age 60 | 9–11% CAGR | Mixed equity + debt | Long retirement horizon, extra ₹50k 80CCD(1B) |

| Tax-saver FD | 5 years | 6.5–7% | Bank credit risk | Hard to recommend, honestly |

| Life insurance (ULIP/endowment) | 5+ years | 4–6% | Insurance + market | Skip. Buy term insurance separately, invest the rest. |

My pick is ELSS first, NPS second (for the extra ₹50,000 deduction under 80CCD(1B)), PPF only if you’ve already maxed equity exposure elsewhere. Mirae Asset ELSS Tax Saver has delivered roughly 17.8% 5-year CAGR; the lock-in is 3 years, the shortest of any 80C instrument. PPF‘s 7.1% looks safe until you remember inflation eats most of it.

If you’ve moved to the new tax regime, 80C is moot. You don’t get the deduction. Invest the same money in a regular ELSS, an index fund, or a flexi-cap. The fund mechanics are identical; you just lose the upfront tax benefit.

Never combine insurance and investment. ULIPs and endowment plans are sold hard because they pay 25% to 35% commission on the first-year premium. The “returns” you see are net of those commissions. Buy a pure term life cover (₹1 crore for 25 to 30 years costs roughly ₹10,000 to ₹15,000 a year for a healthy 30-year-old) and invest the rest in mutual funds. The math always wins.

Direct plans vs regular plans: the ₹5 to ₹8 lakh question

Every Indian mutual fund comes in two flavors: direct and regular. Direct plans are bought from the AMC (or a free platform like Kuvera). Regular plans are bought through a distributor or your bank, and they include a 0.5% to 1% annual commission baked into the expense ratio.

That commission compounds against you. On a ₹10,000 monthly SIP held for 20 years at 12% CAGR, the difference between a direct plan and a regular plan is roughly ₹5 to ₹8 lakh. For a 30-year horizon, it’s closer to ₹15 lakh. That money goes to your bank’s relationship manager, not you.

So always direct. Always. The only situation where a regular plan makes sense is if you’re paying a fee-only financial planner who needs the trail commission as part of their compensation, and that arrangement is rare in India. For 99% of self-directed investors, direct is the default.

If you already have regular-plan investments (most people who started before 2018 do), switch them. Use Kuvera’s “switch to direct” feature, or do it manually through the AMC. There’s a small short-term capital gains hit if you redeem and rebuy within a year, so plan around the LTCG window if you can.

SIP vs lump sum (and why I stopped overthinking it)

The internet has spent a decade debating SIP versus lump sum. Here’s the honest answer. If you have a lump sum sitting in a savings account today, the math says invest it now. Markets go up more often than they go down, and time-in-the-market beats time-out-of-the-market on long horizons. Multiple studies on Nifty 50 data show lump sum beats SIP about two-thirds of the time over 10-year holds.

But that math assumes you’ll actually deploy the lump sum and not panic if the market drops 15% the next month. Most people can’t. So the SIP framework wins not because it’s mathematically optimal, but because it’s behaviorally sustainable. Which beats optimal every time.

Practical rule: if you have a lump sum that’s less than 6 months of your SIP value, deploy it now. If it’s more, stagger it across 6 to 12 months as an STP (systematic transfer plan) from a liquid fund into the equity fund. This gives you most of the math advantage without the stomach problem.

Minimum SIP amount in most funds is now ₹100 to ₹500 a month. There’s no excuse to wait until you “have enough.” Start with ₹500. Step it up by ₹500 every 6 months. The habit matters more than the amount in year one.

The platforms I actually use

Three platforms cover 95% of what an Indian retail investor needs. Each does one thing better than the others.

Kuvera

Free, mutual-fund-only, direct plans by default, decent goal-tracking, family-account support. This is where I’d send a beginner who only wants mutual funds. The interface is clean, KYC is fast, and the family feature lets you manage spouse and parent portfolios from one login.

- Direct plans only, no commission baked in

- Free for life, no premium tier nag

- Goal-based investing with auto-rebalance prompts

- Family accounts in one place

- Mutual funds only (no stocks, no bonds, no crypto)

- Customer support is email-only

Zerodha (Coin + Kite)

If you also want to buy individual stocks, ETFs, or bonds, Zerodha is the cleanest stack. Coin handles direct mutual funds, Kite handles equities, the same login covers both. Charges are flat (₹20 per trade) with zero brokerage on equity delivery. The educational content (Varsity) is genuinely good.

- One login for MF, stocks, ETFs, bonds, IPOs

- Zero brokerage on delivery equity

- Varsity education is free and well-written

- Strong outage history vs newer apps

- Annual maintenance charge of ₹300 on demat

- Coin’s MF UX is more functional than friendly

Groww

Easiest onboarding of the three. If a friend is intimidated by Kuvera or Zerodha, send them to Groww. Direct mutual funds, stocks, US stocks, and a slick mobile app. The trade-off is a busier interface that nudges you toward more action than you probably need.

- Fastest KYC and onboarding I’ve seen

- Beginner-friendly UI

- US stocks via partner integration

- App pushes “trending stocks” notifications a bit too eagerly

- Outage record is shakier than Zerodha

What I’d skip: any platform that pre-loads a “regular plan” portfolio at sign-up (most banks do this), and any “wealth advisor” app that takes 1% AUM annually. You’re paying that fee to avoid making four decisions a year. It’s not worth it.

Real estate, crypto, and gold: the satellites that aren’t asset classes

Three things every beginner gets pitched within their first year of investing. None of them belong in the core portfolio. All of them have a place at the edges if you actually want them.

Real estate

The Indian middle class has been told for two generations that buying a flat is the safest investment. It’s the most illiquid investment they’ll ever make, costs 6% to 10% in transaction friction (stamp duty, registration, brokerage), and locks 70% of their net worth into one address. If you want real estate exposure, REITs are the easier honest answer.

Listed Indian REITs (Embassy Office Parks, Mindspace Business Parks, Brookfield India REIT, Nexus Select Trust) trade on NSE like stocks. You can buy ₹5,000 worth, collect quarterly distributions, and sell next month if you need the money. No tenants, no broker, no power-of-attorney. Allocation: 5% to 10% if you want it, zero if you already own a flat. Don’t double up.

Crypto

Cap it at 5% of your portfolio, treat it as speculation, and only allocate money you can fully lose. Bitcoin and Ethereum are the only two with infrastructure mature enough to take seriously. Everything else is a casino chip with marketing. India’s 30% flat tax on crypto gains and 1% TDS on every trade also hurt the math; a 30% tax with no offset for losses is brutal compared to equity LTCG.

Gold

If you want gold, Sovereign Gold Bonds (SGBs) are the right wrapper: 2.5% annual interest on top of gold price appreciation, capital gains tax-free if held to maturity. SGB issuance has slowed since 2024, so secondary-market SGBs and the GOLDBEES ETF are reasonable alternatives. Physical gold (chains, coins, biscuits) is for sentiment, not investment. Resale haircuts are 5% to 10% before you even leave the shop.

The mistakes that cost beginners the most money

Most beginner losses don’t come from picking the wrong fund. They come from the same five behaviors, repeated across every market cycle. If you avoid these, you’ll outperform the average investor without any extra skill.

- Stopping SIPs during a crash. The exact moment your SIP becomes valuable (cheaper units) is the moment most people pause it. The 2020 COVID crash was the best 12 months to keep SIPs running in the last decade. The people who paused missed the recovery. Set the SIP, then forget the password.

- Over-diversification. Holding 12 funds isn’t safer than holding 4. It’s just harder to track. Most overlap on the same underlying stocks anyway. Three to five funds. That’s it.

- Timing the market. “I’ll start when the market dips” is how people sit in cash for three years and miss a 60% rally. The data is unambiguous: time-in-market beats timing the market. Always.

- Chasing star fund managers. Last year’s top-performing fund is rarely next year’s. Performance reverts to the mean. Pick a fund for its mandate and cost, not its 1-year return.

- Buying regular plans because the bank “advised” you. Your relationship manager is a salesperson with a quota. The 1% trail commission they’re earning compounds against you for life. Always direct.

- Redeeming the emergency fund for a “great opportunity.” The opportunity will pass. The emergency won’t.

Sample plans: ₹10,000 and ₹50,000 a month

Two worked examples, using the 3-bucket framework. Adjust for your age and risk tolerance, but the structure stays the same.

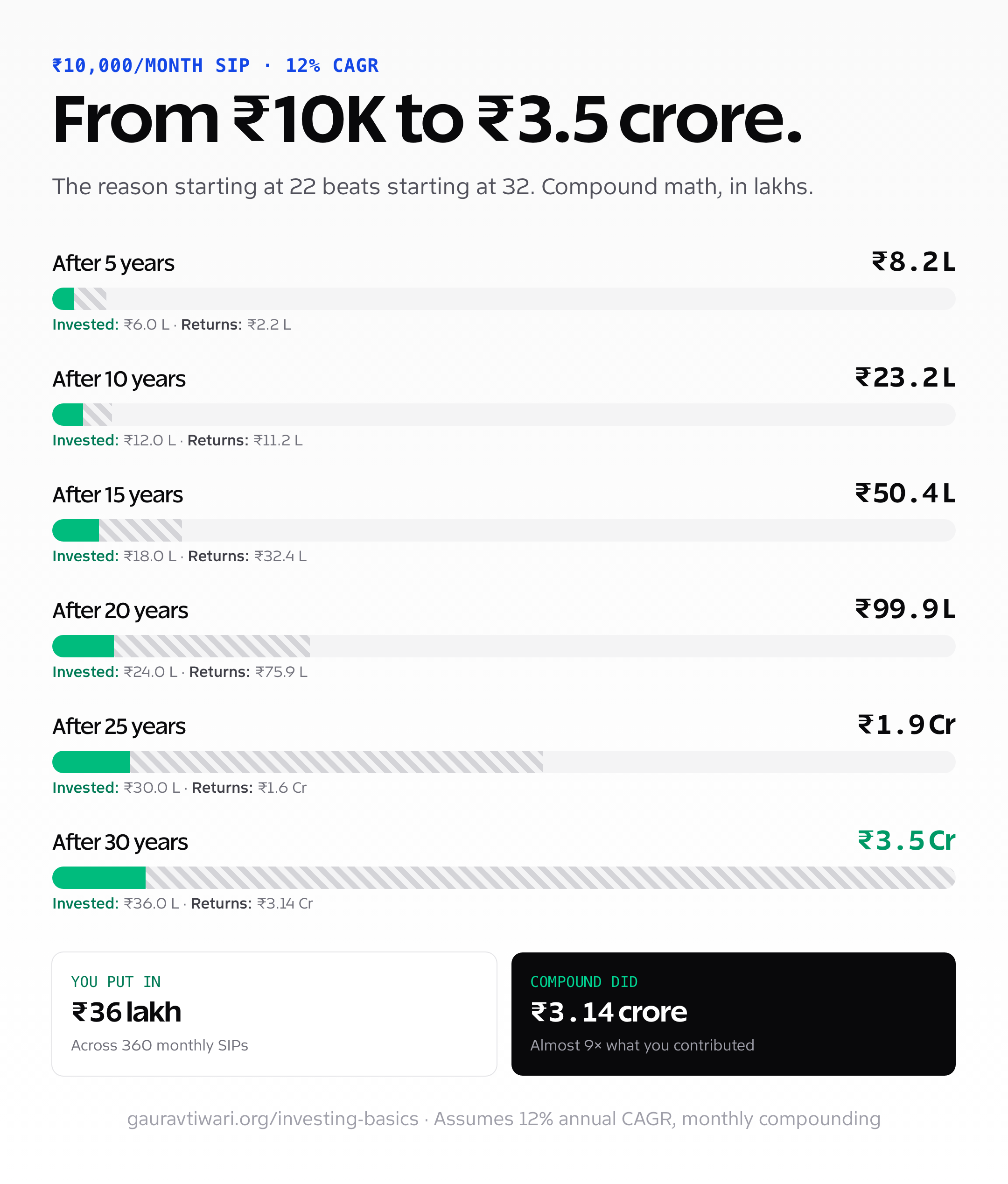

₹10,000 per month (typical 25-year-old salaried)

| Fund | Bucket | SIP |

|---|---|---|

| UTI Nifty 50 Index Fund (Direct) | Large-cap / Index | ₹4,000 |

| Nippon India Multi Cap Fund (Direct) | Mid + Small | ₹3,000 |

| Parag Parikh Flexi Cap Fund (Direct) | Flexi (incl. global) | ₹2,000 |

| Nippon India Liquid Fund | Debt | ₹1,000 |

If you’re on the old tax regime, swap ₹4,000 of large-cap for Mirae Asset ELSS Tax Saver to use up part of your 80C. Step the total up by ₹500 to ₹1,000 every salary hike. At ₹10,000 per month for 30 years at 12% CAGR, you end up with roughly ₹3.5 crore. That’s not a typo.

₹50,000 per month (mid-career, possibly with bonus chunks)

| Fund | Bucket | SIP |

|---|---|---|

| UTI Nifty 50 Index Fund (Direct) | Large-cap / Index | ₹15,000 |

| UTI Nifty Next 50 Index Fund (Direct) | Large/Mid index tilt | ₹5,000 |

| Nippon India Multi Cap Fund (Direct) | Mid + Small | ₹10,000 |

| Quant Small Cap Fund (Direct) | Aggressive small-cap | ₹5,000 |

| Parag Parikh Flexi Cap Fund (Direct) | Flexi + global | ₹10,000 |

| HDFC Short Term Debt Fund | Debt | ₹5,000 |

This is six funds, which is on the upper end of what I’d recommend. The argument for the extra two is that ₹50,000 has enough capital to give Next 50 and a small-cap tilt meaningful weight without overlapping too much. If you’re not comfortable with small-cap volatility, drop Quant and increase Parag Parikh by ₹5,000. Same total, less heart-rate.

If you get an annual bonus, don’t try to time it into the market. Park it in a liquid fund and STP it across 6 to 12 months into your equity funds. This is the textbook lump-sum-into-SIP solution and it works.

When to rebalance (and when to leave it alone)

Rebalance once a year, on a date you’ll remember (your birthday, April 1, the day after Diwali, doesn’t matter). If your equity allocation has drifted more than 5 percentage points from your target, sell from the overweight bucket and buy the underweight. If it hasn’t, do nothing.

The reason annual is enough: market noise washes out, and frequent rebalancing creates short-term capital gains tax events that eat your returns. Once a year is plenty. Some people rebalance only when allocation drifts 10%; that’s also fine.

The other rebalance trigger is life. New job, marriage, kid, house purchase, retirement within 5 years. These shift your goal dates and risk tolerance, and the portfolio should shift with them. The classic move is glide-path: drop 5% of equity per year for the 5 years before you start drawing on the money.

What I’d do differently if I were 22 again

Three things, honestly.

First, I would have started the SIP earlier and smaller. The years you waste “researching” before starting are years that compounding can’t get back. ₹500 a month at 22 beats ₹5,000 a month at 32. Run the math, it’s not even close.

Second, I would have ignored every “hot small-cap” tip I got from cousins and college friends. Concentrated stock picks based on someone’s brother-in-law’s broker are how 22-year-olds learn what a permanent loss feels like. Index funds for years, then maybe individual stocks once you’ve watched a full bear market without flinching.

Third, I would have read the actual SEBI consultation papers and AMFI fund factsheets instead of YouTube finance influencers. The primary sources are dry, free, and right. The secondary sources are entertaining and often wrong. Pick which one your future net worth deserves.

Look, the boring portfolio works. It’s worked for fifty years across every major market. The reason most people don’t follow it isn’t that they don’t know. It’s that “set up four SIPs and ignore them for thirty years” doesn’t sell newsletters, courses, or YouTube views. So the financial content economy keeps inventing new things to do. Don’t fall for it. The sample plan above is enough. The rest is reading.

If you want to go deeper on specific funds, my best mutual funds in India guide covers each category fund-by-fund. For the bigger-picture playbook around money, see how to achieve financial freedom. To track your portfolio without spreadsheets, the Android apps to manage personal finance roundup has what I actually use. And if you do allocate that 5% to crypto, the crypto exchange comparison covers where to buy it without getting fleeced on fees.

A note on what I’m not. I’m not a SEBI-registered investment advisor. The views above are what I’ve done with my own money and what I’ve recommended to friends and family who asked. Tax rates and rules quoted here apply to FY26 in India and may change. Past returns don’t predict future ones. The framework (index core, active satellites, direct plans, three buckets) is older than I am and likely to outlast me. The specific funds and percentages are educated defaults, not personalized advice.

Frequently Asked Questions

What is the minimum amount needed to start investing in India?

₹100 to ₹500 per month is enough to start an SIP in most Indian mutual funds. UTI Nifty 50 Index Fund and Parag Parikh Flexi Cap accept ₹500 monthly. Stocks have no minimum (you can buy one share). The amount matters less than the consistency in year one. Start with ₹500, step up by ₹500 every six months as you get comfortable.

Is it better to invest in stocks or mutual funds as a beginner?

Mutual funds, almost always. Direct stock picking requires research time, emotional discipline, and tolerance for being wrong about specific companies. Mutual funds (especially index funds) give you instant diversification across 50 to 250 stocks, professional management or low-cost passive tracking, and a structure that prevents the worst beginner mistakes. Buy individual stocks only after you’ve held a mutual fund portfolio through a full bear market without panicking.

How are mutual fund returns taxed in India in 2026?

Equity funds: short-term gains (held under 12 months) are taxed at 20%. Long-term gains above ₹1.25 lakh per year are taxed at 12.5%. Debt funds: all gains are taxed at your slab rate, regardless of holding period (the indexation benefit was removed in 2023). Plan redemptions to stay within the ₹1.25 lakh annual LTCG exemption when possible.

How many mutual funds should I invest in?

Three to five funds total. A typical mix: one large-cap or index fund (40%), one mid or small-cap fund (30%), one flexi-cap (20%), and one debt or liquid fund (10%). More funds create overlap on the same underlying stocks and make tracking harder. If you have a large portfolio (₹10 lakh+), six funds is the upper limit before diminishing returns.

Should I prefer index funds or active mutual funds in India?

Index funds for large-cap, active funds for mid-cap, small-cap, and flexi-cap. SPIVA India data shows roughly 90% of active large-cap funds underperform the Nifty 50 over 5 years, so paying 1.5% TER for them rarely makes sense. UTI Nifty 50 Index Fund at 0.18% TER is the default large-cap pick. In mid-cap and small-cap categories, active management still adds value because those segments are less efficiently priced.

What is the difference between direct and regular mutual fund plans?

Direct plans are bought from the AMC or a free platform like Kuvera. Regular plans are bought through a distributor or bank and include a 0.5% to 1% annual commission. Over 20 years on a ₹10,000 monthly SIP, that commission costs ₹5 to ₹8 lakh in lost returns. Always pick direct plans unless you’re paying a fee-only advisor who needs the trail commission as part of their compensation.

Is ELSS better than PPF for tax saving?

For most investors under 40 on the old tax regime, yes. ELSS funds have a 3-year lock-in (shortest of any 80C instrument) and have delivered 13 to 17% CAGR over 10-year periods. PPF is locked for 15 years and currently pays 7.1%, which barely beats inflation. The trade-off: ELSS is volatile and can drop 20 to 30% in a bad year, while PPF is government-guaranteed. If you can stomach drawdowns, ELSS wins on long-term math.

Should I stop my SIPs when the market is falling?

No. The whole point of an SIP is rupee-cost averaging, which works best when prices fall. A falling market means your monthly contribution buys more units. Investors who paused SIPs during the March 2020 COVID crash missed one of the strongest 12-month rallies in NSE history. If you can afford the SIP, keep it running through corrections. Stopping is the most expensive instinct in retail investing.

Are mutual funds safe in India?

Mutual funds in India are regulated by SEBI and managed by AMFI-registered AMCs. Your money is held in a trust separate from the AMC‘s balance sheet, so even if an AMC fails, your investments are protected. The risk that remains is market risk: equity funds can lose 20 to 40% in a bear market. That risk is real but recoverable on long horizons. Operational risk (fraud, AMC failure) is small in India compared to most emerging markets.

Can NRIs invest in mutual funds in India?

Yes. NRIs can invest in Indian mutual funds through NRE or NRO bank accounts after completing KYC with passport and overseas address proof. Some AMCs restrict investments from US and Canada-based NRIs due to FATCA compliance, so check with the specific AMC before investing. Taxation depends on the DTAA (Double Tax Avoidance Agreement) between India and your country of residence. Kuvera and most major AMCs handle NRI accounts directly.

Abbreviations used in this article

Quick reference for every abbreviation used above. Each one is also wrapped in an inline <abbr> tag in the body, so hovering shows the full form in context.

| Abbreviation | Full form |

|---|---|

| AMC | Asset Management Company |

| AMFI | Association of Mutual Funds in India |

| AUM | Assets Under Management |

| CAGR | Compound Annual Growth Rate |

| DICGC | Deposit Insurance and Credit Guarantee Corporation |

| DTAA | Double Taxation Avoidance Agreement |

| ELSS | Equity Linked Savings Scheme |

| ETF | Exchange-Traded Fund |

| FATCA | Foreign Account Tax Compliance Act |

| FD | Fixed Deposit |

| FDIC | Federal Deposit Insurance Corporation |

| FY26 | Financial Year 2025-26 |

| IPO | Initial Public Offering |

| IRA | Individual Retirement Account |

| KYC | Know Your Customer |

| LTCG | Long-Term Capital Gains |

| NAV | Net Asset Value |

| NPS | National Pension System |

| NRE | Non-Resident External |

| NRI | Non-Resident Indian |

| NRO | Non-Resident Ordinary |

| NSC | National Savings Certificate |

| NSE | National Stock Exchange |

| PPF | Public Provident Fund |

| PSU | Public Sector Undertaking |

| REIT | Real Estate Investment Trust |

| SEBI | Securities and Exchange Board of India |

| SEC | Securities and Exchange Commission |

| SGB | Sovereign Gold Bond |

| SIP | Systematic Investment Plan |

| SPIVA | S&P Indices Versus Active |

| STCG | Short-Term Capital Gains |

| STP | Systematic Transfer Plan |

| TDS | Tax Deducted at Source |

| TER | Total Expense Ratio |

| ULIP | Unit Linked Insurance Plan |