Business Loan: How to Apply in India, the US, and the EU (2026 Guide)

Most business owners take the wrong loan from the wrong place because nobody told them the right options exist. Government-backed schemes go ignored. Public-sector banks get written off as “slow” before anyone reads the eligibility sheet. Fintech apps charge 22% APR for what a credit-guarantee scheme would do for 9%. This guide is the version I wish I’d had when I first applied for a small business line of credit, written for the three jurisdictions where most of you reading this actually operate: India, the United States, and the European Union.

The mechanics differ. The principles don’t. In every country there are four routes for a business loan: a government-backed scheme, a public-sector bank, a private bank, or a fintech/NBFC lender. Each route has a different cost, a different waiting time, and a different bar for eligibility. Pick the wrong one and you’ll either pay too much, wait too long, or get rejected for a loan you would have qualified for somewhere else. The point of this guide is to make sure that doesn’t happen.

The four routes for any business loan, anywhere

Before we split by country, here’s the universal map. Every business loan you will ever consider falls into one of these four buckets, regardless of jurisdiction:

- Government-backed schemes. Cheapest money. Slowest paperwork. Strict eligibility. Best for first-time borrowers, micro-enterprises, women and minority-led businesses, and anyone who can fit a scheme’s exact box. Examples: MUDRA in India, SBA 7(a) in the US, EIF guarantees in the EU.

- Public-sector banks. Mid-cost money. Mid-speed paperwork. Most loans backed by these banks ride on top of government schemes. SBI in India, KfW in Germany, BPI France in France.

- Private banks. Mid-to-high cost. Faster decisions. Higher rejection rate for thin-file applicants. HDFC, Chase, BNP Paribas, Santander.

- Fintech and NBFC lenders. Highest cost. Fastest approval (often under 48 hours). Most lenient on paperwork. The right answer when speed matters more than rate. Lendingkart and Indifi in India, OnDeck and BlueVine in the US, October and Iwoca in the EU.

The honest hierarchy: try a government-backed scheme first if you qualify, then a public-sector bank, then a private bank, then a fintech only if the first three fail or speed is non-negotiable. Most business owners do this in reverse, then complain about interest rates. Don’t.

Quick disclaimer: rates, eligibility thresholds, and scheme details change every fiscal year. Everything below is current as of 2026. For any specific application, verify on the lender’s official site or the relevant government portal before you commit.

India: government schemes most owners ignore

India runs more credit-linked subsidy schemes than any country I’ve researched, and the average small business owner I talk to has heard of one of them. The cost of that gap is staggering. A ₹10 lakh business loan at 9% from MUDRA Tarun versus the same ₹10 lakh at 18% from a fintech costs roughly ₹3.5 lakh more in interest over five years. That’s a salary. So before you fill out a form on any private platform, walk through the schemes below.

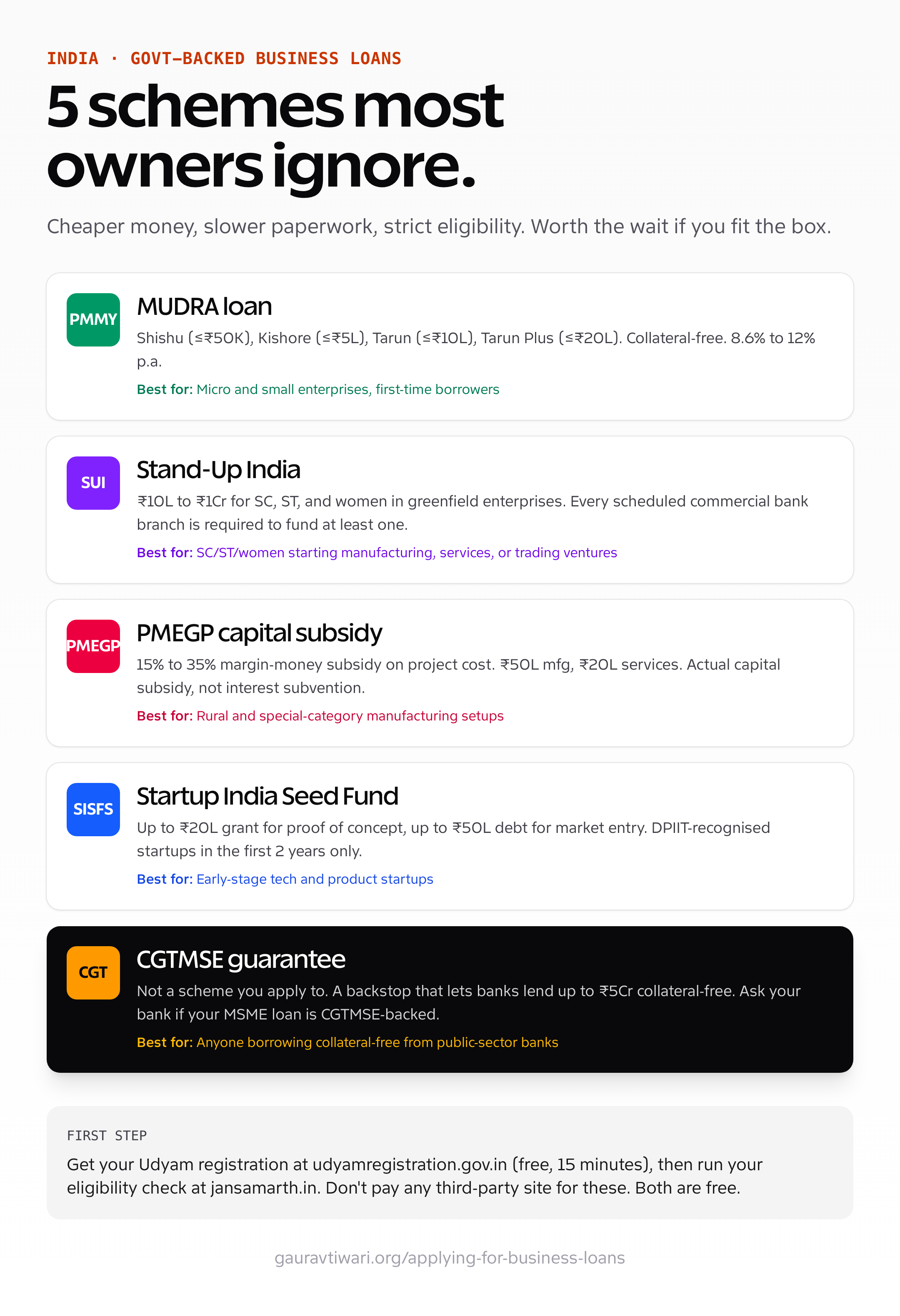

Pradhan Mantri MUDRA Yojana (PMMY)

The big one. Launched in 2015 by the Government of India, MUDRA (Micro Units Development and Refinance Agency) provides credit-linked loans to non-corporate, non-farm micro and small enterprises. Three tiers based on loan size: Shishu (up to ₹50,000), Kishore (₹50,001 to ₹5 lakh), and Tarun (₹5 lakh to ₹10 lakh). Budget 2024 added Tarun Plus, extending the ceiling to ₹20 lakh for borrowers who have repaid an earlier MUDRA loan in full.

What’s working under the hood: MUDRA loans are collateral-free. The risk sits with the lending bank, not you, and the Credit Guarantee Fund for Micro Units (CGFMU) backstops the bank. Interest rates land between 8.6% and 12% depending on the lender and your credit profile. Apply through any scheduled commercial bank, regional rural bank, small finance bank, MFI, or NBFC. The unified Jan Samarth portal aggregates eligibility checks across schemes including MUDRA. That’s the cleanest digital-first entry point.

What’s not working: turnaround times vary wildly across branches. A well-prepared application at SBI or Bank of Baroda can close in two to three weeks. The same paperwork at a smaller cooperative bank can take two months. The portal helps with discovery but the final approval still happens at a branch, with all the unevenness that implies.

Stand-Up India

Targeted credit for entrepreneurs from Scheduled Castes, Scheduled Tribes, and women, for greenfield (new) enterprises in manufacturing, services, or trading. Loan size: ₹10 lakh to ₹1 crore. Available at every scheduled commercial bank branch in India, with at least one beneficiary from each category per branch as a mandate. Credit-linked guarantee through CGFMU plus margin-money support for first-generation entrepreneurs.

Honest read: Stand-Up India is the most under-utilised major scheme in the country. Disbursements have run well below targets every year since launch. The reason is mostly awareness, not eligibility. If you’re a woman starting a manufacturing or services business in India, this should be the first scheme you check. The official site is standupmitra.in; it also offers handholding agency support to help with the application package.

PMEGP (Prime Minister’s Employment Generation Programme)

The subsidy heavyweight. PMEGP combines a bank loan with a government-given margin-money subsidy that ranges from 15% to 35% of the project cost, depending on whether the unit is rural or urban and whether the entrepreneur belongs to a special category (women, SC/ST, OBC, minority, ex-servicemen, physically handicapped, NER residents). Project ceilings: ₹50 lakh for manufacturing, ₹20 lakh for services. Administered by the Ministry of MSME via KVIC, KVIB, and DICs.

Why this is rare and good: most “subsidies” advertised in India are interest-rate subventions of 1% to 2%. PMEGP is an actual capital subsidy that reduces the loan amount you have to repay. On a ₹25 lakh manufacturing project in a rural area for a special-category applicant, the 35% subsidy is ₹8.75 lakh that you simply don’t owe. Apply through the KVIC PMEGP e-portal. The application requires a project report and an EDP (Entrepreneurship Development Programme) certificate, which is two weeks of training and one of the few requirements I’d call non-negotiable.

Startup India Seed Fund Scheme (SISFS)

For DPIIT-recognised startups in their first two years. Up to ₹20 lakh as grant for proof of concept, prototype, or product trials, plus up to ₹50 lakh as debt or convertible debentures for market entry, commercialisation, or scaling. Deployed through approved incubators, not banks directly. Apply on seedfund.startupindia.gov.in.

What works: the grant portion is genuinely free money for early-stage product validation, with no equity dilution and no repayment obligation if used per the sanctioned plan. What needs work: the incubator-routing layer adds bureaucratic friction. Picking a strong incubator matters more than the application content. T-Hub Hyderabad, Atal Incubation Centres, IIT incubators, and a few private ones (NSRCEL, IIM Bangalore) have a track record of pushing applications through.

CGTMSE: collateral-free credit guarantee

Not a scheme you apply to directly. CGTMSE (Credit Guarantee Fund Trust for Micro and Small Enterprises) is a guarantee mechanism the lender uses to extend collateral-free credit. The trust covers up to 85% of the loan default for the bank, which is what makes the bank willing to lend without security. The current ceiling is ₹500 lakh per borrower (raised from ₹200 lakh in 2024). Most MUDRA loans, SIDBI loans, and a chunk of public-sector bank MSME loans are CGTMSE-backed underneath.

Practical implication: when you apply for an MSME loan at SBI, Bank of Baroda, or Canara Bank, ask the relationship manager explicitly whether the loan is being processed under CGTMSE. If yes, no collateral is required. If no, ask why. Branch managers sometimes default to a collateralised structure even when the borrower would qualify for the guarantee. It’s not malicious; it’s just easier paperwork. Push back.

India: MSME registration and Udyam (do this first)

Before you apply for any MSME-eligible scheme or loan, you need a Udyam registration certificate. This is the official MSME registration mechanism that replaced the old Udyog Aadhaar in 2020. Without it, you don’t qualify as an MSME for legal purposes, regardless of what your turnover or balance sheet says.

Definition (revised by Budget 2025): a Micro enterprise has investment in plant and machinery up to ₹2.5 crore and turnover up to ₹10 crore. Small enterprise: investment up to ₹25 crore, turnover up to ₹100 crore. Medium enterprise: investment up to ₹125 crore, turnover up to ₹500 crore. The thresholds were raised from earlier limits to expand the MSME envelope; a lot of businesses that were classified as “Medium” or above earlier are now formally Small.

The registration takes 10 to 15 minutes online if you have your Aadhaar, PAN, and basic business details ready. Go to udyamregistration.gov.in. That’s the only legitimate URL. There are dozens of impostor sites that charge ₹500 to ₹2,000 for the same free service. Avoid them. The registration is free and self-declared, and your certificate downloads immediately on completion.

If you registered before 2020 with the older Udyog Aadhaar, that registration expired on 1 July 2022. Re-register on the Udyam portal. Several MSME loan rejections I’ve seen in the last two years traced back to applicants assuming their old Udyog Aadhaar was still valid.

India: business loan eligibility: the real bar

Lender marketing pages list “minimum eligibility” criteria that almost everyone meets. The actual bar at major banks in 2026 is significantly higher. Here’s the unmarketed reality:

- CIBIL score 700+ for unsecured loans, 750+ for the better rates. Below 700, expect either rejection or a higher-rate fintech offer. Below 650, fix the score before applying. Every rejection adds an enquiry that drops the score further.

- Business vintage of 3+ years for most private banks, 2+ years for public-sector banks, 6 months for fintech. First-year businesses without a track record should default to PMMY Shishu or Stand-Up India, not private bank applications.

- Annual turnover usually ₹40 lakh to ₹1 crore minimum for unsecured loans at private banks. Public-sector banks under MSME schemes often have no minimum.

- GST returns for the last 12 months, ITRs for the last 2 to 3 years, and bank statements for 6 to 12 months. Inconsistent GST filings are the single most common reason for rejection at banks.

- Profitability: most banks expect at least one profitable year on file. Loss-making applicants get pushed to NBFCs and fintech.

The best move before applying: pull your CIBIL report (free once a year at cibil.com), reconcile it, and dispute any errors. I’ve seen scores jump 40 to 60 points after a clean dispute on a duplicate or mis-tagged tradeline. That’s the difference between an unsecured loan at 11% and a “you’ll need collateral” conversation at 14%.

India: business loan interest rate, 2026

Rough rate ranges by lender category, as of 2026. Verify on the lender’s site before you decide.

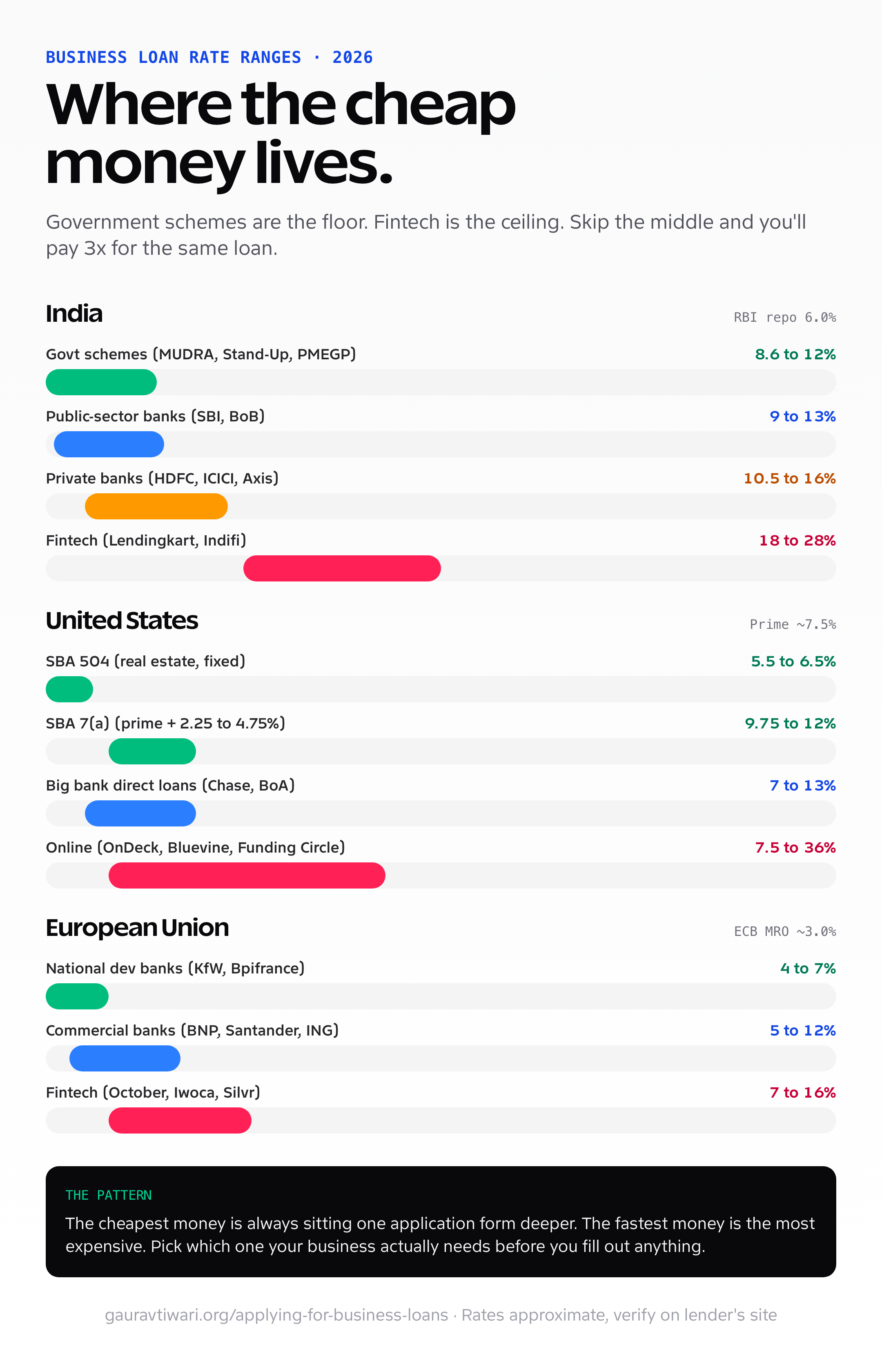

| Lender category | Rate range (p.a.) | Typical decision time | Best for |

|---|---|---|---|

| Government schemes (MUDRA, Stand-Up India, PMEGP) | 8.6% to 12% | 2 to 8 weeks | Eligible micro/small enterprises, special-category entrepreneurs |

| Public-sector banks (SBI, BoB, Canara, PNB) | 9% to 13% | 2 to 4 weeks | Established MSMEs, CGTMSE-backed loans |

| Private banks (HDFC, ICICI, Axis, Kotak) | 10.5% to 16% | 3 to 7 days | Profitable businesses with 3+ years vintage |

| NBFCs (Bajaj Finserv, L&T Finance, Tata Capital) | 14% to 22% | 2 to 5 days | Mid-tier credit profiles, faster turnarounds |

| Fintech lenders (Lendingkart, Indifi, FlexiLoans) | 18% to 28% | 24 to 72 hours | Speed-critical applications, thin-file borrowers |

The compounding effect of choosing badly is brutal. On a ₹25 lakh, 5-year loan, the difference between a 10% public-sector bank rate and a 22% NBFC rate is roughly ₹9 lakh in extra interest. That’s the gap between a good year and a bad one for most small businesses. The 2 to 3 weeks the public-sector application takes is almost always worth it.

SBI business loan: the deep dive

State Bank of India is the largest MSME lender in the country and runs the broadest catalogue of business loan products. If you’re qualifying for any government-backed scheme, SBI is almost always one of the cleanest paths. Here are the four products worth knowing.

SBI e-Mudra Loan

End-to-end digital MUDRA loan. Up to ₹1 lakh disbursed within minutes for eligible existing SBI current/savings account holders. The catch: the e-only flow is currently for the Shishu and Kishore tiers; for Tarun (above ₹5 lakh) the application still routes through a branch. Honest take: this is the cleanest digital MSME loan flow at any Indian bank, but the ₹1 lakh ceiling is too low for most actual business needs. Useful for inventory top-ups, less useful for capex.

SBI SME Smart Score

Pre-approved scoring-based working capital and term loans up to ₹50 lakh for established MSMEs with at least 3 years of operations. Decision in 10 to 15 days. Interest rates start around 9.5% under the current EBLR (External Benchmark Lending Rate) regime. The “smart score” engine evaluates banking behaviour, GST/ITR data, and credit history; minimum aggregate score required for sanction varies branch to branch but typically lands at 60+ on a 100-point scale.

SBI Asset-Backed Loans

Higher-ticket, collateral-secured business loans up to ₹10 crore against commercial or residential property. Loan-to-value typically 60% to 65% of fair market value. Interest rates 9.25% to 11% depending on profile. The product to know if you’re scaling capex past the ₹50 lakh limits of unsecured products.

SBI Stand-Up India

SBI‘s branch network is the single largest deployment surface for the Stand-Up India scheme. ₹10 lakh to ₹1 crore for SC/ST and women entrepreneurs in greenfield enterprises. Margin-money support and CGFMU guarantee both bake into the structure. Apply at any SBI branch with the standard package: business plan, identity proof, address proof, and a valid Udyam registration.

Across all four products, SBI‘s bottleneck is the same: the application moves through the branch’s MSME desk, which is staffed unevenly across the country. A senior MSME officer can process a clean Smart Score application in two weeks; an overworked branch with one officer for the entire MSME book can take two months. Ask the branch manager who handles MSME applications before you start the process. If they shrug, find another branch.

India: HDFC, ICICI, Axis Bank business loans

The private-bank trio that runs most middle-market MSME lending in India. All three offer roughly the same shape of product: unsecured working-capital loans up to ₹50 lakh, secured loans against property up to ₹5 to ₹10 crore, overdraft facilities, and bill-discounting lines. Rates start in the 11% to 12% band and climb to 16% based on profile. Speed is the primary differentiator versus public-sector banks: a clean private-bank application can sanction in 3 to 5 working days.

- HDFC Bank tends to give the cleanest digital application flow. Pre-approved offers based on existing relationship banking are common; if you’ve banked with HDFC for 2+ years, check your NetBanking dashboard before applying anywhere else.

- ICICI Bank’s InstaBIZ app is genuinely good for sole-proprietorship working-capital lines under ₹25 lakh. KYC and disbursal can complete in 2 days for existing customers.

- Axis Bank is the strongest of the three for asset-backed loans against commercial property. Their MSME desk in metros has historically been faster on documentation review than the other two.

For more on whether MSME loans actually serve small businesses well in India, my earlier piece Are MSME Loans a Boon or a Curse for India? goes into the structural problems and where the schemes still fall short.

India: when to use a fintech lender (and when not to)

Lendingkart, Indifi, FlexiLoans, NeoGrowth, IndiaLends, and Razorpay Capital are the fintech lenders that matter for Indian businesses. They share a common operating model: GST-data-driven underwriting, fully digital onboarding, disbursal in 24 to 72 hours, and rates that start at 18% APR and climb fast. The trade-off is straightforward.

- Use a fintech when you have a real opportunity-cost on the next 7 days (a bulk inventory purchase, a confirmed PO that needs working capital), your bank application has stalled past 2 weeks, or you simply don’t qualify at a bank yet.

- Skip the fintech when you can wait. The 12-percentage-point rate gap between a fintech and a public-sector bank is the difference between profitable lending and predatory lending for many small businesses.

Honest commentary: most fintech credit-decisioning runs on GST-return signals, current-account flow analysis, and a thin layer of credit-bureau data. The underwriting isn’t bad. It’s just expensive because the cost of capital for an NBFC funded through bond markets is structurally higher than a public-sector bank’s deposit base. That’s the actual reason rates can’t compress. The marketing pages won’t tell you that.

India: how to actually apply via Jan Samarth

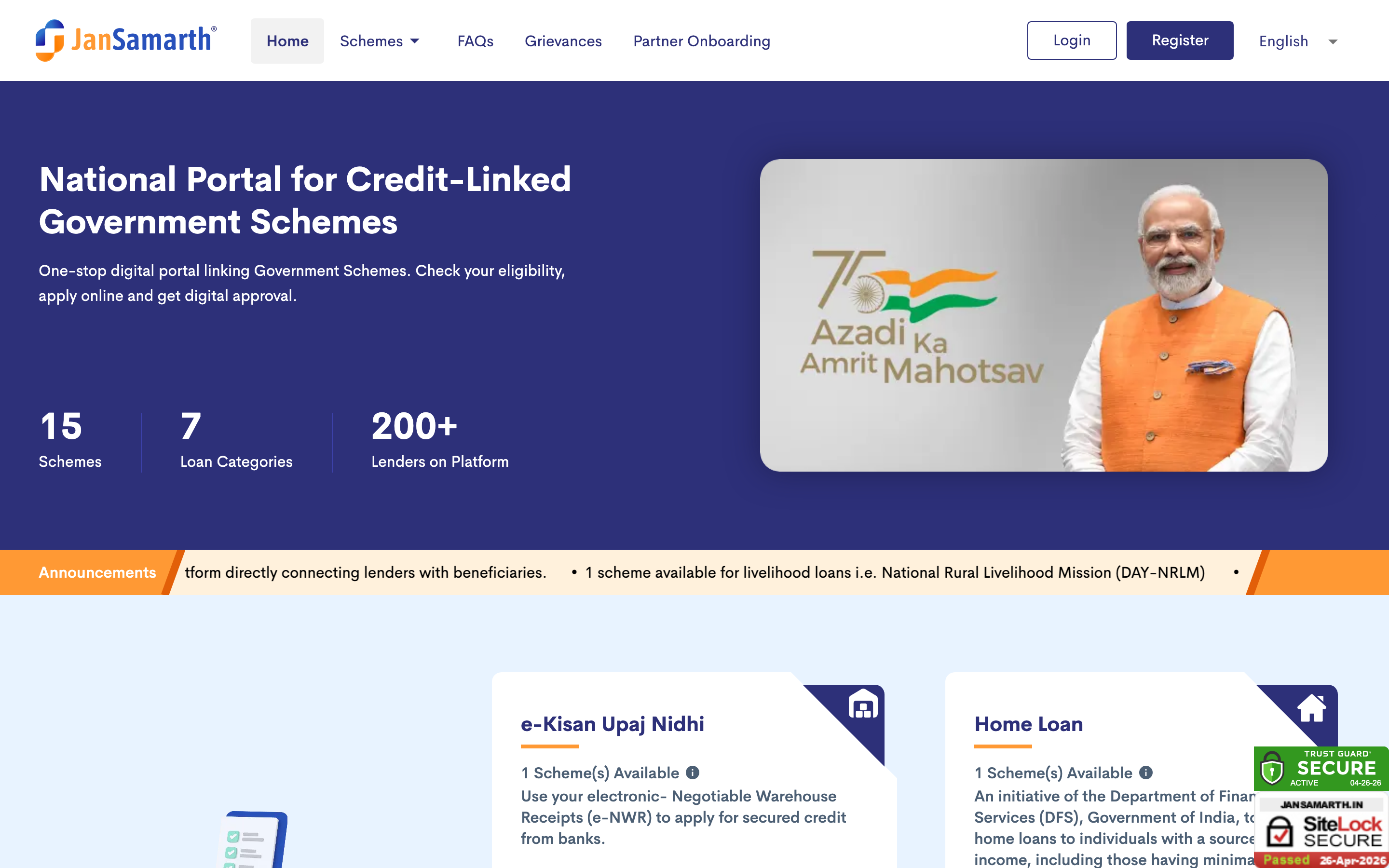

Jan Samarth is the unified portal for credit-linked government schemes, launched by the Ministry of Finance in 2022. It covers four loan categories: Education, Agri, Business Activity, and Livelihood. For business loans, the portal aggregates eligibility checks across MUDRA, Stand-Up India, PMEGP, PM SVANidhi, and a few state-level schemes.

- Visit jansamarth.in and click on “Business Activity Loan”.

- Run the eligibility checker. The questions are short: type of business, location (rural/urban), category (general/SC/ST/OBC/minority/women), proposed loan amount, intended use of funds.

- The portal returns a list of schemes you qualify for, with eligibility, subsidy details, and the participating banks for each.

- Select a scheme. The portal forwards your application to a participating bank along with pre-validated KYC.

- The bank’s MSME desk picks up the application from the portal queue. From there it’s the standard process: documentation, branch verification, sanction.

What works: the eligibility check is genuinely useful. I’ve seen applicants discover PMEGP eligibility they didn’t know about purely through the questionnaire. What doesn’t: the back-end queue handoff to the bank is uneven. Some banks pull from the portal queue daily; others let it sit. Once you submit through Jan Samarth, follow up at the relevant bank branch within 7 days. Don’t assume the digital handoff will move on its own.

United States: SBA loans and the direct-lender stack

The American business-loan landscape is dominated by two paths: government-guaranteed loans through the Small Business Administration, and direct loans from banks, credit unions, and fintech lenders. The SBA itself does not lend; it guarantees a portion of loans made by approved partner lenders, which lets those lenders extend credit on terms more favourable than they could justify on a standalone basis.

SBA 7(a) Loan

The flagship SBA programme. Up to $5 million for working capital, equipment, real estate, or business acquisition. SBA guarantees 75% to 85% of the loan, depending on size. Interest rates are pegged to the prime rate plus a margin, typically prime + 2.25% to prime + 4.75% in 2026. Repayment terms run 10 to 25 years depending on use of proceeds.

What works under the hood: the guarantee mechanism reduces the lender’s risk, which is what enables the longer terms and lower rates than a standalone bank loan would offer. What doesn’t: the application is paperwork-heavy and the decision timeline runs 30 to 90 days for a full underwrite. SBA Express, a sub-product, caps at $500,000 and runs faster (under 36 hours for the SBA decision, though the lender still adds time).

SBA 504 Loan

For real-estate and major equipment purchases. Up to $5.5 million. Structured as 50% from a conventional lender, 40% from a Certified Development Company (CDC) backed by the SBA, and 10% from the borrower. Fixed rates on the SBA portion, typically 5.5% to 6.5% in 2026. That makes 504 the cheapest fixed-rate commercial property finance widely available to American small businesses.

SBA Microloan

Loans up to $50,000, made by SBA-approved nonprofit intermediaries. Typical loan size is closer to $13,000. Rates run 8% to 13%. Designed for very small businesses, women, minorities, veterans, and low-income entrepreneurs who don’t yet qualify for 7(a) or conventional bank loans. The intermediary lender often bundles the loan with technical assistance, which is uncommon and useful.

For more on the SBA path, my earlier Complete Guide to Getting a Small Business Administration (SBA) Loan covers the application checklist and the Lender Match tool in detail.

Direct lenders: banks, credit unions, online

Outside the SBA ecosystem, the choice of direct lender shapes the cost. Big four banks (JPMorgan Chase, Bank of America, Wells Fargo, Citi) have the broadest small-business products but the strictest underwriting; expect rates of 7% to 13% for established borrowers and outright rejection for thin-file applicants. Community banks and credit unions often offer better rates and more flexibility but with lower loan ceilings.

Online lenders fill the speed gap. OnDeck for term loans and lines of credit up to $250,000, with rates from around 27% APR (yes, that’s correct. Convenience comes priced). Bluevine for working-capital lines of credit up to $250,000, rates from 7.8% APR for the strongest profiles. Funding Circle for term loans up to $500,000, rates from 7.49% to 36% depending on credit. Kabbage (now part of American Express) for short-duration lines.

Honest take on online lenders: APR-stated products are honest. The “factor rate” products (typical with Merchant Cash Advances and short-term commercial advances) are not. A factor rate of 1.3 on a 6-month repayment is approximately 60% APR, which most borrowers don’t realise. Always convert factor rates to APR before signing. My MCA loan guide has the formula and the disclosure traps.

European Union: a fragmented map with one common backstop

The EU does not have a single SBA-equivalent. Business lending happens primarily through national systems, but the European Investment Fund (EIF) and the European Investment Bank (EIB) sit on top, providing guarantees and on-lending facilities to national intermediaries. The result is a two-layer market: EU-level guarantees behind the scenes, national-level applications in the foreground.

EIF / EIB programmes

InvestEU is the consolidated EU-level instrument that replaced the older COSME and EFSI programmes in 2021. It runs four policy windows, one of which (SME Window) provides guarantees to financial intermediaries who in turn lend to SMEs across all 27 member states. Borrowers don’t apply to InvestEU directly; they apply to a national bank or fintech that’s signed up as an intermediary, and the EU guarantee shows up as more favourable rates or relaxed collateral requirements.

The EU‘s Access to Finance portal lets you filter intermediaries by country and product type. That’s the entry point for finding an EU-guarantee-backed loan in your country.

National development banks

Each major EU economy has a public development bank that channels government and EU programmes into SME credit. Worth knowing because they typically offer better terms than commercial banks and process applications through partner lenders.

- Germany: KfW. The largest national development bank in Europe. KfW Unternehmerkredit and ERP-Gründerkredit are the two flagship SME products. Rates currently 4% to 7% depending on programme and credit profile. Apply through your house bank, which forwards the application to KfW.

- France: Bpifrance. Combines guarantees, direct loans, and equity for French SMEs. Prêt Croissance and Prêt à Taux Zéro (zero-interest innovation loans) are the standouts.

- Spain: ICO. The Instituto de Crédito Oficial channels EU and Spanish-state credit into SMEs through commercial banks. ICO Empresas y Emprendedores covers most general business needs.

- Italy: Cassa Depositi e Prestiti (CDP). Co-finances SME lending with commercial banks. CDP-backed loans typically run 100 to 200 basis points cheaper than market.

- Netherlands: Invest-NL. Newer national development bank, focused more on growth-stage and impact financing than micro-loans.

Commercial banks and pan-European fintech

Commercial bank rates for SME loans in the EU run 5% to 12% depending on country and risk profile, sitting structurally below comparable Indian or fintech rates because of the lower European Central Bank base rate environment. The bigger banks (BNP Paribas, Santander, ING, UniCredit, Deutsche Bank) all operate cross-border SME desks, but the local subsidiary’s rates are usually better than the cross-border product.

The pan-European fintech lenders worth knowing: October (P2P lending across France, Spain, Italy, Netherlands, Germany), Iwoca (UK and Germany, lines of credit), Silvr (revenue-based financing for digital businesses), and Lendix/October Nordic for Scandinavia. Rates typically 7% to 16% APR for borrowers with at least 6 months of operating history, faster than bank approval but slower than the US fintech equivalents.

EU-specific quirk worth flagging: many member states require a notarised loan agreement above certain thresholds (Germany’s notary requirement above €100,000 is the canonical example). Add 1 to 3 weeks to your timeline for that step if you’re borrowing in Germany, Austria, France, or Italy. The cost is typically 0.5% to 1% of the loan, paid to the notary.

Documents you’ll need (any country)

The list varies in detail across jurisdictions, but the shape is consistent. Have the following ready before you start any application:

- Identity proof. Aadhaar + PAN in India; SSN/ITIN + driver’s licence in the US; national ID + tax number in the EU.

- Business registration. Udyam certificate (India), EIN with state registration (US), Handelsregister/SIRET/Camera di Commercio entry (EU).

- Tax filings. Last 2 to 3 years of business and personal tax returns. ITRs in India, federal tax returns and Schedule C in the US, country-specific filings in the EU.

- Bank statements. 6 to 12 months of business current-account statements.

- Financial statements. Profit and loss, balance sheet, cash flow. CA-certified in India, CPA-prepared for larger US loans, accountant-attested in most EU countries.

- Project report or business plan. Mandatory for government schemes (PMEGP, SBA 7(a), KfW Gründerkredit), often optional for direct bank loans.

- Collateral documents. Property deeds, equipment invoices, fixed-deposit receipts, for any secured loan.

The single highest-impact prep step is reconciling your bank statements with your tax returns. Lenders look at consistency between declared revenue and actual cash flow. Mismatches kill applications faster than bad credit scores. Spend a weekend on this before you submit anything.

The mistakes that cost businesses the most money

- Borrowing more than you need. Lenders nudge you to take the maximum approved amount. Take only what your cash flow can service without strain. The interest on every “extra” lakh or dollar compounds for the full tenure.

- Not checking government schemes first. Skipping PMMY, SBA, or KfW because “the paperwork is annoying” is the most common four-figure-mistake I see. The rate gap pays for the paperwork three times over.

- Applying at five lenders simultaneously. Each application triggers a credit-bureau enquiry. Five enquiries in 30 days drops your score 30 to 50 points and signals desperation to underwriters. Pre-qualify with soft pulls, then apply at one or two.

- Confusing factor rate with APR. Especially in the US fintech space. A factor rate of 1.3 isn’t a 30% interest rate; depending on tenure, it can be 50% to 80% APR. Always convert before signing.

- Ignoring the prepayment clause. Many private bank and NBFC loans charge 2% to 5% on early repayment of principal. If your business is seasonal or your cash flow is lumpy, this clause matters more than the headline rate.

- Assuming “no collateral” means “no risk”. Personal guarantees on unsecured business loans are standard in India and the US. If the business defaults, the lender comes after the promoter’s personal assets. Read the personal guarantee clause carefully.

- Skipping the Udyam/MSME registration. In India specifically, missing this step disqualifies you from the most favourable rates and schemes. It’s free, it takes 15 minutes, and there’s no reason not to do it.

Frequently Asked Questions

Which government scheme is best for a new business in India?

For most new businesses with project costs under ₹10 lakh, MUDRA Shishu or Kishore is the cleanest option. For SC/ST and women entrepreneurs starting greenfield enterprises with project sizes between ₹10 lakh and ₹1 crore, Stand-Up India is the strongest choice. For manufacturing and services projects up to ₹50 lakh in rural areas (or ₹20 lakh urban), PMEGP gives you a 15 to 35 percent capital subsidy on top of the loan. For DPIIT-recognised startups in the first two years, the Startup India Seed Fund Scheme offers up to ₹20 lakh as grant and ₹50 lakh as debt.

What is the eligibility for an MSME business loan in India?

Your business must be Udyam-registered as Micro, Small, or Medium based on the 2025 thresholds: investment in plant and machinery up to ₹2.5 crore (Micro), ₹25 crore (Small), or ₹125 crore (Medium); turnover up to ₹10 crore, ₹100 crore, or ₹500 crore respectively. For unsecured MSME loans, banks typically require a CIBIL score of 700 or higher, a business vintage of 2 to 3 years, the last 12 months of GST returns, and 2 to 3 years of ITRs. Public-sector banks under government schemes are more lenient on vintage; fintech lenders are more lenient on credit score but charge higher rates.

What is the current business loan interest rate in India in 2026?

Government-scheme rates start around 8.6 percent for MUDRA loans through public-sector banks. Public-sector bank MSME loans run 9 to 13 percent. Private bank rates are 10.5 to 16 percent. NBFC rates run 14 to 22 percent. Fintech lenders charge 18 to 28 percent APR. The gap between the cheapest and most expensive option on a ₹25 lakh, 5-year loan can easily be ₹9 lakh in extra interest, which is why government schemes and public-sector banks are worth the longer wait when you qualify.

How do I apply for a government subsidy loan for business in India?

Start with the Jan Samarth portal at jansamarth.in. The portal aggregates eligibility checks across MUDRA, Stand-Up India, PMEGP, and other credit-linked schemes; the eligibility questionnaire takes 5 to 10 minutes. For PMEGP specifically, apply through the KVIC e-portal at kviconline.gov.in/pmegpeportal/. For PMMY and Stand-Up India, you can also walk into any scheduled commercial bank branch with your Udyam registration, KYC documents, ITRs, and a project report. Public-sector banks (SBI, Bank of Baroda, Canara, PNB) have the deepest experience processing these applications.

What is the SBI business loan interest rate?

SBI‘s MSME loan rates are linked to the External Benchmark Lending Rate (EBLR), and starting rates in 2026 are around 9.25 to 9.5 percent for asset-backed loans and SME Smart Score products, climbing to 11 percent for higher-risk profiles. SBI e-Mudra loans up to ₹1 lakh start near MUDRA scheme rates of 9 to 12 percent. The exact rate offered depends on your CIBIL score, business vintage, banking relationship, and loan size. Existing SBI current-account holders typically get 25 to 50 basis points off the published rate.

What is the maximum loan amount under Pradhan Mantri MUDRA Yojana?

The original three tiers cap at Shishu ₹50,000, Kishore ₹50,001 to ₹5 lakh, and Tarun ₹5 lakh to ₹10 lakh. Budget 2024 introduced Tarun Plus, which extends the ceiling to ₹20 lakh for borrowers who have repaid an earlier MUDRA loan in full. Most banks process MUDRA Shishu and Kishore loans without collateral; for Tarun, a CGFMU guarantee covers the bank’s risk so collateral is still not required, though some banks ask for personal guarantees from the proprietor.

What is the SBA 7(a) loan and how do I apply in the US?

The SBA 7(a) loan is the flagship US Small Business Administration programme, offering up to $5 million for working capital, equipment, real estate, or business acquisition, with the SBA guaranteeing 75 to 85 percent of the loan to the lending bank. You apply through an SBA-approved partner lender, not the SBA directly. Use the SBA Lender Match tool at sba.gov to find participating lenders near you. Rates are pegged to the prime rate plus 2.25 to 4.75 percent, terms run 10 to 25 years, and full underwriting takes 30 to 90 days. SBA Express, a sub-product capped at $500,000, runs faster.

How do EU business loans differ from US and Indian ones?

The EU has no single SBA-equivalent. Business loans are originated by national banks and fintech lenders, with EU-level guarantees from the European Investment Fund (EIF) and the European Investment Bank (EIB) backing select intermediaries through programmes like InvestEU. Rates are structurally lower than India and the US thanks to the lower ECB base rate environment, typically 5 to 12 percent for SME loans. Each major EU economy also has a public development bank (KfW in Germany, Bpifrance in France, ICO in Spain, CDP in Italy) that channels government and EU credit into SMEs at favourable terms.

Can a startup get a loan from the Indian government?

Yes. The most relevant scheme for new ventures is the Startup India Seed Fund Scheme (SISFS), open to DPIIT-recognised startups in the first two years of incorporation, offering up to ₹20 lakh as grant for proof of concept and up to ₹50 lakh as debt or convertible debentures. Apply through approved incubators, not banks directly. For broader credit, MUDRA loans, Stand-Up India, and PMEGP are also available to startups that meet the eligibility criteria. Get DPIIT recognition first at startupindia.gov.in; it unlocks tax benefits, easier compliance, and access to the seed fund.

What credit score do I need for a business loan?

For unsecured business loans at major Indian private banks, a CIBIL score of 700 or higher is the practical minimum, with the better rates reserved for 750+. US banks typically require a personal FICO of 680 or higher and a business credit score (Dun and Bradstreet PAYDEX) of 80 or higher for SBA-backed loans. EU lenders rely on country-specific bureaus (Schufa in Germany, Banque de France ratings, etc.) and bank-internal scorecards more than a single number. Below the bank thresholds, fintech lenders will lend at higher rates with credit scores down to 600 or below in most jurisdictions.

Abbreviations used in this article

Quick reference for every abbreviation used above. Each one is wrapped in an inline <abbr> tag in the body, so hovering shows the full form in context.

| Abbreviation | Full form |

|---|---|

| APR | Annual Percentage Rate |

| BoB | Bank of Baroda |

| CA | Chartered Accountant |

| CDC | Certified Development Company |

| CDP | Cassa Depositi e Prestiti (Italy) |

| CGFMU | Credit Guarantee Fund for Micro Units |

| CGTMSE | Credit Guarantee Fund Trust for Micro and Small Enterprises |

| CIBIL | Credit Information Bureau (India) Limited |

| COSME | Programme for the Competitiveness of Enterprises and SMEs |

| CPA | Certified Public Accountant |

| DICs | District Industries Centres |

| DPIIT | Department for Promotion of Industry and Internal Trade |

| EBLR | External Benchmark Lending Rate |

| ECB | European Central Bank |

| EFSI | European Fund for Strategic Investments |

| EIB | European Investment Bank |

| EIF | European Investment Fund |

| EIN | Employer Identification Number |

| ERP | European Recovery Programme (Germany) |

| EU | European Union |

| FICO | Fair Isaac Corporation credit score |

| GST | Goods and Services Tax |

| HDFC | Housing Development Finance Corporation Bank |

| ICICI | Industrial Credit and Investment Corporation of India Bank |

| ICO | Instituto de Crédito Oficial (Spain) |

| ITIN | Individual Taxpayer Identification Number |

| ITR | Income Tax Return |

| KVIB | Khadi and Village Industries Board |

| KVIC | Khadi and Village Industries Commission |

| KfW | Kreditanstalt für Wiederaufbau (German national development bank) |

| MCA | Merchant Cash Advance |

| MFI | Microfinance Institution |

| MSME | Micro, Small, and Medium Enterprises |

| MUDRA | Micro Units Development and Refinance Agency |

| NBFC | Non-Banking Financial Company |

| NER | North Eastern Region |

| OBC | Other Backward Classes |

| P2P | Peer-to-Peer |

| PAN | Permanent Account Number |

| PAYDEX | Dun & Bradstreet PAYDEX (business payment score) |

| PMEGP | Prime Minister’s Employment Generation Programme |

| PMMY | Pradhan Mantri MUDRA Yojana |

| PNB | Punjab National Bank |

| PO | Purchase Order |

| SBA | Small Business Administration (United States) |

| SBI | State Bank of India |

| SC | Scheduled Caste |

| SIDBI | Small Industries Development Bank of India |

| SIRET | Système d’Identification du Répertoire des Etablissements (France) |

| SISFS | Startup India Seed Fund Scheme |

| SME | Small and Medium-sized Enterprise |

| SSN | Social Security Number |

| ST | Scheduled Tribe |

| SVANidhi | Street Vendor’s AtmaNirbhar Nidhi |

| Udyam | MSME registration system (replaces Udyog Aadhaar since 2020) |

Where to go from here

The boring discipline of checking government schemes first, doing your CIBIL or FICO clean-up before applying, and only borrowing what you can service is what separates good business borrowing from expensive mistakes. Most of the rest is paperwork.

For deeper reading on adjacent topics: my MSME loans piece goes into the structural problems with how India serves small business credit. The SBA guide covers the US application checklist in detail. If you’re early-stage and weighing debt against equity, Raising Startup Capital walks through the alternatives. Balancing Personal and Business Finances is the one I’d hand a first-time founder before they sign anything. And if a loan has already gone sideways, Debt Relief for Your Small Business covers the recovery options.

A note on what I’m not. I’m not a chartered financial planner, a registered investment advisor, or a licenced loan broker. The above reflects my own research and the conversations I’ve had with founders applying for these products in the three jurisdictions. Rates, eligibility, and scheme details change every fiscal year. Always verify on the lender’s official site or the relevant government portal before you commit.