The Future of Cryptocurrency in India

This article on the future of Cryptocurrency in India was written in an unbiased mode. I do not want to oppose or support a specific party or government. If you think there is an opinion that offends you or your opinion — I will humbly apologize for that. But in this article I have tried my best to bring the best of information without bending towards any subject.

Cryptocurrency in India is a very sensitive matter and God knows what will happen in the near future but the truth is that the Indian government is not innovation-friendly and prohibits the transactions in Crypto by just quoting the risk of Black Money etcetera — which is totally absurd. Every new tech has some disadvantages but for the better good things are adapted and the system is improvised. Bitcoin landed on the market in 2009 and in the last 12 years the government couldn’t find a way to use it.

India should have been one of the first countries to establish its reliability and trustworthiness as an alternative financial system. In a country with over 1.30 Billion people you always need to find a way to make lives better for the people.

Countries across the world have made efforts towards developing a secure and efficient system for transacting in this new form of currency, with a view that in the near future cryptocurrency is highly likely to rule the world economy.

India is yet to open to Cryptocurrencies, specifically Bitcoin. There is a low chance that they’d be open for these in any near future. But now and then they show slightest signs of improvement regarding Cryptocurrency.

Let’s study all the things in detail in 3 main headings: the past, the present and the future of Cryptocurrency in India.

Cryptocurrency in India: The Past

In 2013, India announced Bitcoin as untrustworthy and labeled it as “Wild West Territory” where frauds and scams like Silk Road, market of drugs on dark-net are prevalent and where selfish greedy geeks conned innocent citizens into losing their money. This was the Manmohan Singh Government — who themselves were prone to corruption and scams. Calling a new technology was not fair, even though their claim of Bitcoin being untrustworthy was correct.

The fact to note is that India was not aware of its value at that time but as the nation went through a change in its global financial and political situation, its viewpoint towards cryptocurrency also changed. India became an ideal place to trade in Bitcoin a few years later. The government could have just adapted to Bitcoin and related cryptocurrencies — or they could have just released their own Cryptocurrency.

During 2012-2016, there was a high demand from the public to curb corruption and to eliminate the Black Money market. Bitcoin could only add to the trouble. Demonetization happened on 8th November 2016 and India was left with a little liquidity. Indian Government with assistance from the Reserve Bank of India (RBI) removed 500 and 1000-Rupees currencies from circulation, bringing 86% of the country’s money straight to ashes. The decision was taken as a step to crush its ever-growing dark economy and to get rid of never-ending illegal affairs

Simultaneously, this verdict, though not intentional, taught the nation’s 1.3 billion people of the uncertainty that comes with holding cash as property. With a 7% fall in the stock market, cash scarcity and some serious adversaries faced by many citizens in the queue for exchanging their useless money, it didn’t take long to cause a nationwide hysteria.

This was a big experiment and whatever the outcome was — it was sure that the Indian Currency was not to be trusted. Many people were already using Bitcoin but this also set them back. According to The Economic Times, by mid-2017, around 2,500 Indian investments were happening with Bitcoin on a daily routine. It took a while for the economy to fully recover, say 2 years.

In 2019 people got used to digital methods of payments. With Jan Dhan Yojana and other banking schemes, over 90% of the population in India had bank accounts. People were getting used to UPI payments and online banking. Zerodha like brokers had landed to the market to make investments easier. Ecommerce shopping was on rise. People were using digital means to make, spend or save money.

It was the ideal time for Cryptocurrencies to land properly in India.

The digital money attracted people of India as it seemed a safer option for investing, that lay far apart from government rules and regulations and from political and economic disturbances.

But the Government had no interest in paying any attention to the matter. All they did was to prohibit transactions by quoting the regulation and risk in investing in Cryptocurrencies.

Cryptocurrency in India: The Present

Also read: Using cryptocurrencies to promote your business

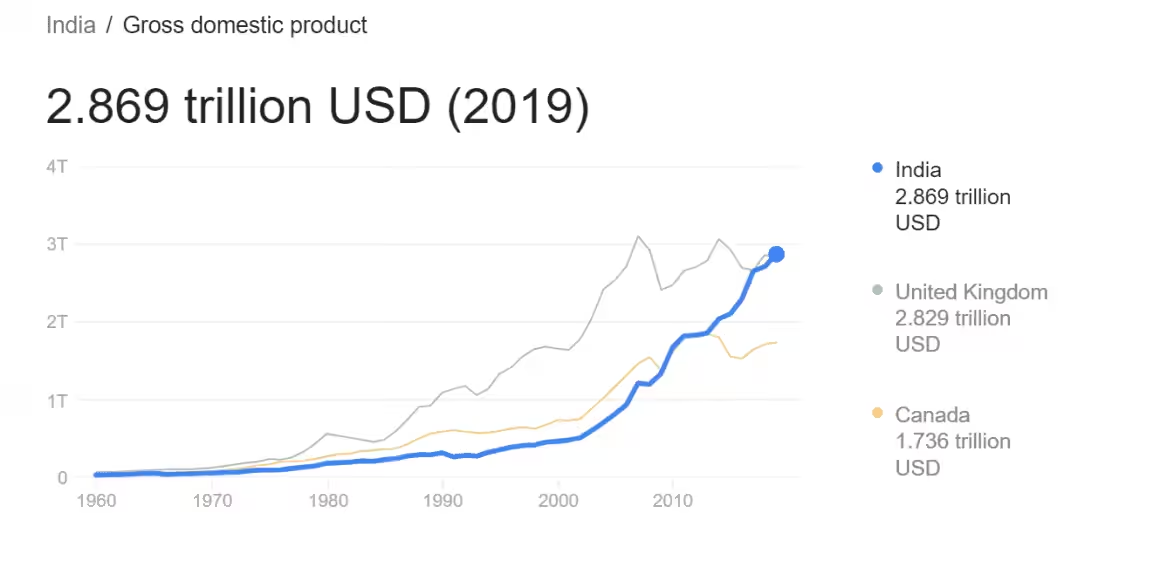

India is the 5th largest economy in the world as per the World Bank with a GDP of 2.87 Trillion USD. But on the ground the reality is somewhat different. Many people, especially the youth, don’t have bank accounts. Youth knows and understands the complexities as well the importance of Cryptocurrencies. With more young people with bank accounts, we can expect more investments to things like Stocks and Crypto.

Now, Bitcoin, in this case, can turn out to be a great success as it provides a method of transacting and making deals across the globe cheaply and securely without requiring a bank account. No doubt, as of now, more than 8 million Indians own cryptocurrency in some or other form which accounts for thousands of crores, according to Nischal Shetty, founder and CEO of crypto-exchange agency WazirX.

Also read: Planning to Start using Bitcoins: Save Transactions Cost with Discount Codes

Bitcoin usage by Indian companies

In 2018, more than 500 merchants and several big companies in India, including Dell, gave an option of paying in cryptocurrency, as told by GBminers co-founder Amit Bhardwaj. Of course, Bitcoin still has miles to conquer before it can be labeled as . popular among Indians as most of us prefer direct money. But the numbers are increasing with each passing day. As already said, cryptocurrency now holds more than 5 million users in the country.

Stand of Indian Government on Cryptocurrency

The Reserve Bank of India (RBI) has continuously warned cryptocurrency users and traders about the risks associated with this new system, however, the Indian Prime Minister, Narendra Modi, indirectly gave a thumbs up to cryptocurrency on 2nd July 2018 with his ambitious picture of Digital India. Several meeting sessions have been held for discussing the scope of cryptocurrency in Indian economy and to formulate regulations and a proper system to govern this.

A while back in 2018, the government formed an inter-disciplinary committee to study the structure of digital currency and set up a forum MyGov to collect public opinions regarding cryptocurrency.

Post this, India’s Department of Economic Affairs arranged for a meeting to discuss regulation of Bitcoin and it was decided that cryptocurrencies too, should be regulated under The Reserve Bank of India Act 1934 as per which, investment in Bitcoin (or any such cryptocurrency) should be taxed and guidelines for such any transactions with virtual currencies should be properly drafted and Foreign Exchange Management Act 1999 (FEMA) should be extended to cross-border cryptocurrency transactions, by IRB.

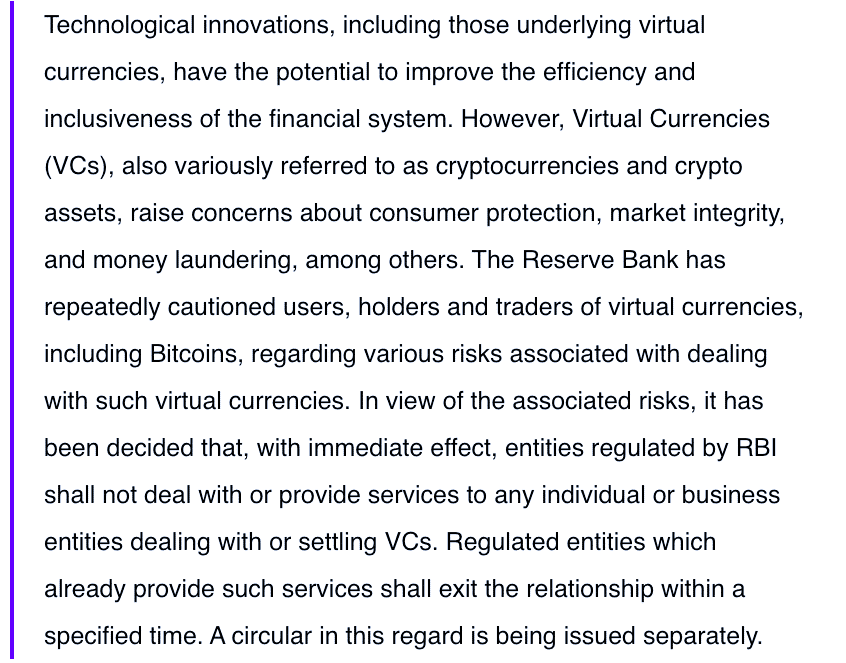

Now, this whole discussion about future of cryptocurrency in India has recently become a hot topic as RBI filed a draft under the title “Banning of Cryptocurrency and Regulation of Official Digital Currency Bill 2019” for banning cryptocurrency from India and issuing as much as a 10-year imprisonment to those dealing, holding or selling cryptocurrency in any form. The press release by RBI regarding this matter says that:

However, on 4th March 2020, the Supreme Court ruled that the warning by RBI on banning cryptocurrency trading, in the financial institutions being regulated by RBI itself, was simply unconstitutional. This provides a green signal to dealing and transacting in cryptocurrencies like Bitcoin and Ethereum, however, the actual trading is still cloudy until RBI’s final announcement on the issue.

The Global Picture

As per the 2018 cryptocurrency statistics, the world market witnessed more than 1500 cryptocurrencies with over 9400 verified transactions. The estimated cumulative market value of all cryptocurrencies across the globe has raised up to $237.1 billion. Bitcoin shares as much as 40% of the cryptocurrency market holding a market price of 5,12,461 INR as of today.

With such a huge population of more than 1.3 billion people and an economy still growing and flourishing by the day, India holds a huge chance of success for cryptocurrencies. The economy of India is undergoing a complete renewal after the International Monetary Fund labeled it as the fastest growing economy. With over 600 million or 45% of its population having internet access, cryptocurrency has high chances of becoming an important financial asset in the near future.

The Future of Cryptocurrency in India

Cryptocurrency is now used to make online purchases or even physical products and hence provides a great opportunity for business holders and companies to monetize various digital applications. It is also a probable option for getting used in social networks, loyalty games and P2P networks. For online gamers, some offer reward cryptocurrencies for watching advertisements, taking informative surveys or winning social games. This helps to increase the use of cryptocurrency not just as a financial token but also as a marketing tool. This offer-based distribution of cryptocurrency by companies to users, who successfully complete a given task, allows the companies to establish efficient and secure loyalty schemes.

Till date, more than 8 million people in India have used cryptocurrency and the numbers are likely to grow exponentially in the coming years as a result of upcoming economic reforms. The fact that India is a great market for cryptocurrency such as Bitcoin has already been established and the Government of India seems to be ready to formulate a system for regulating cryptocurrency as part of the Indian economy. With so many companies and investors already dealing with and trading in cryptocurrency and the countless opportunities still remaining to be explored, little help and support from the government can turn cryptocurrency into a major asset for the Indian market in the coming future.