Understanding Stock Market Basics for Beginners

The stock market intimidates people. News channels flash numbers and percentages. Experts debate whether markets will rise or fall. Terms like “bull market,” “P/E ratio,” and “market capitalization” get thrown around casually. This wall of complexity keeps many people from ever starting to invest, and they miss years of potential compound growth as a result.

But here’s what I wish someone had told me when I was starting out: the fundamentals aren’t complicated. The stock market is simply a place where people buy and sell ownership in companies. That’s it. Understanding the basics requires no finance degree, no special software, and no insider knowledge. I’ve been investing for years, and the core principles I use today are the same ones any beginner can learn in an afternoon.

This guide covers what you actually need to know to start investing confidently. Not everything there’s to know. Just what matters.

What Stocks Actually Are

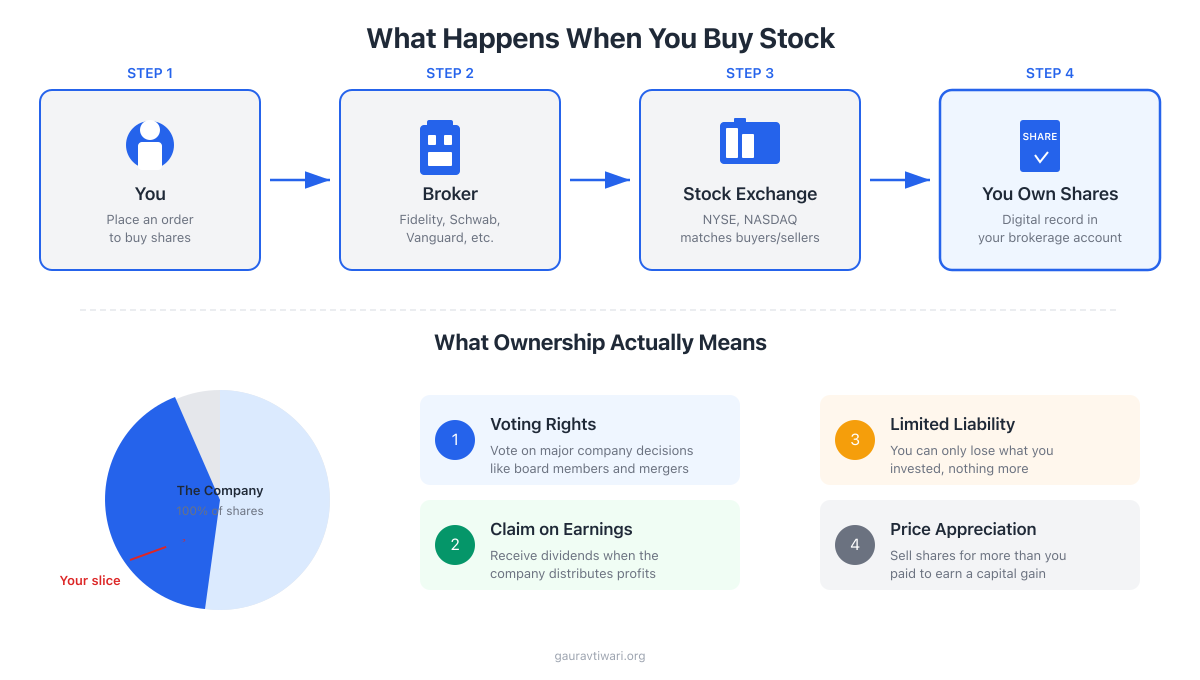

When you buy stock, you’re buying ownership in a company. Real ownership.

A stock represents a small piece of a business. If a company has 1 million shares outstanding and you own 100, you own 0.01% of that company. You have equity in the business, a claim on its assets and earnings, and usually voting rights on major company decisions.

The beauty of stock ownership is limited liability. If the company fails completely, the most you can lose is what you invested. Nobody comes after you for the company’s debts. You risk your investment, nothing more.

Companies issue stock to raise money for growth, operations, and expansion. Investors buy stock hoping the company will grow and their shares will become more valuable over time. When the company prospers, shareholders prosper. When it struggles, so do they.

I remember buying my first shares and realizing I was an actual part-owner of businesses I used every day. It shifted how I thought about investing. You’re not gambling on numbers. You’re buying pieces of real businesses run by real people making real products.

Why Stock Prices Move

Stock prices change based on supply and demand. More buyers than sellers push prices up. More sellers than buyers push prices down. Everything else is just explaining why people want to buy or sell.

Expectations matter more than current reality. Prices reflect what investors expect a company to earn in the future, not just what it earns today. A company can report great earnings and still see its stock drop if investors expected even better. I’ve watched this confuse new investors many times. The stock market is always looking forward.

News impacts prices instantly. Company announcements, economic data, regulatory changes, even tweets from influential people can move prices within seconds. Modern markets process information faster than any individual can.

Earnings drive long-term value. Over months and years, stock prices generally follow business fundamentals. Companies that consistently grow profits see their share prices rise. Companies that lose money see prices decline. Short-term moves can be random, but long-term trends follow the business.

Emotion plays a real role. Fear and greed push prices beyond what fundamentals justify. During panics, quality stocks sell for absurdly low prices. During manias, mediocre companies trade at absurd valuations. If you can stay rational while others aren’t, that’s actually an advantage.

Short-term price movements are essentially unpredictable. Long-term movements tend to follow business fundamentals. This is why time in the market matters so much more than timing the market.

How the Stock Market Works

The market provides a system for buyers and sellers to transact efficiently.

Stock exchanges like the NYSE and NASDAQ are where trading happens. In the old days, humans shouted orders on a trading floor. Today, everything is electronic. Computers match buyers and sellers instantly. When you click “buy” in your brokerage app, your order gets routed to an exchange and executed in milliseconds.

Major US exchanges operate from 9:30 AM to 4:00 PM Eastern, Monday through Friday. Limited trading occurs outside regular hours (pre-market and after-hours), but with less liquidity and wider price spreads. For most investors, regular hours are all that matter.

Market makers are firms that ensure there’s always someone willing to buy or sell, providing liquidity so the system functions smoothly. They profit from the tiny difference between buy and sell prices (the bid-ask spread).

When you place an order, you have options. A market order executes immediately at the current price. A limit order only executes at a price you specify or better. For most long-term investors buying index funds, market orders work fine. If you’re buying individual stocks, limit orders give you more control.

You don’t interact with exchanges directly. Your broker handles all the mechanics. All you do is decide what to buy, how much, and click a button. The infrastructure is invisible.

Key Stock Market Terms

Understanding the vocabulary helps you navigate investment discussions without feeling lost.

Bull market is an extended period of rising prices, generally defined as 20% or more up from recent lows. When people say “we’re in a bull market,” they mean prices have been going up for a while and sentiment is optimistic.

Bear market is the opposite. Extended decline of 20% or more from recent highs. Bear markets are scary but temporary. Every bear market in history has eventually been followed by a bull market.

Market capitalization (market cap) is a company’s total value, calculated as share price times total shares outstanding. Apple’s $3 trillion market cap means the market values the entire company at $3 trillion. Companies are categorized as large-cap (over $10 billion), mid-cap ($2-10 billion), or small-cap (under $2 billion).

Volume is the number of shares traded in a given period. High volume means lots of buying and selling activity. Low volume can mean wider spreads and harder execution.

Dividend is a cash payment companies make to shareholders from profits. Not all companies pay dividends, but many established ones do.

P/E ratio (price-to-earnings) compares a company’s share price to its earnings per share. It tells you how much investors are willing to pay per dollar of earnings. A P/E of 20 means investors pay $20 for every $1 of annual earnings.

Index is a basket of stocks representing a market segment. The S&P 500 represents 500 large US companies. The Dow Jones represents 30 blue-chip stocks.

You don’t need to master every term before investing. I certainly didn’t. You learn as you go, and the important terms stick naturally.

Types of Stocks

Stocks come in different flavors, and understanding the categories helps you build a balanced portfolio.

Large cap, mid cap, small cap refers to company size. Large caps like Apple and Microsoft are more stable but grow slower. Small caps are more volatile but offer higher growth potential. Mid caps sit in between. Most beginners should focus on large caps or broad market funds that include all sizes.

Growth stocks are companies expected to grow faster than average. They typically reinvest all profits into expansion rather than paying dividends. Think technology companies and innovative startups. Higher potential returns, but also higher risk and more volatility.

Value stocks are companies trading below what their fundamentals suggest they’re worth. They’re often mature businesses in less glamorous industries. Value investing means buying these “bargains” and waiting for the market to recognize their true worth.

Dividend stocks pay regular cash dividends to shareholders. They’re typically established companies with stable earnings. The income provides a cushion during market downturns.

Domestic vs. international simply means US companies versus companies based in other countries. Both have a place in a diversified portfolio.

Different stock types serve different purposes. Diversification across types reduces risk, which is why broad market index funds are so popular. One fund, all the categories, zero decision fatigue.

Stock Market Indexes

Indexes track segments of the market and serve as benchmarks for measuring performance. When someone says “the market was up 2% today,” they’re almost always referring to an index.

S&P 500 tracks 500 large US companies and represents about 80% of total US stock market value. It’s the most commonly referenced benchmark for US stock performance. When financial news mentions “the market,” they usually mean this.

Dow Jones Industrial Average tracks 30 large US companies. It’s older and more recognizable but less representative than the S&P 500 because it only includes 30 stocks.

Nasdaq Composite includes all stocks listed on the Nasdaq exchange, which skews heavily toward technology companies. When tech stocks move, the Nasdaq moves more than other indexes.

Russell 2000 tracks 2,000 smaller US companies. It’s the benchmark for small-cap performance.

International indexes like MSCI EAFE (developed markets outside North America) and MSCI Emerging Markets track non-US stocks.

These indexes matter because index funds are built to track them. When you buy an S&P 500 index fund, you’re buying a small piece of all 500 companies in that index.

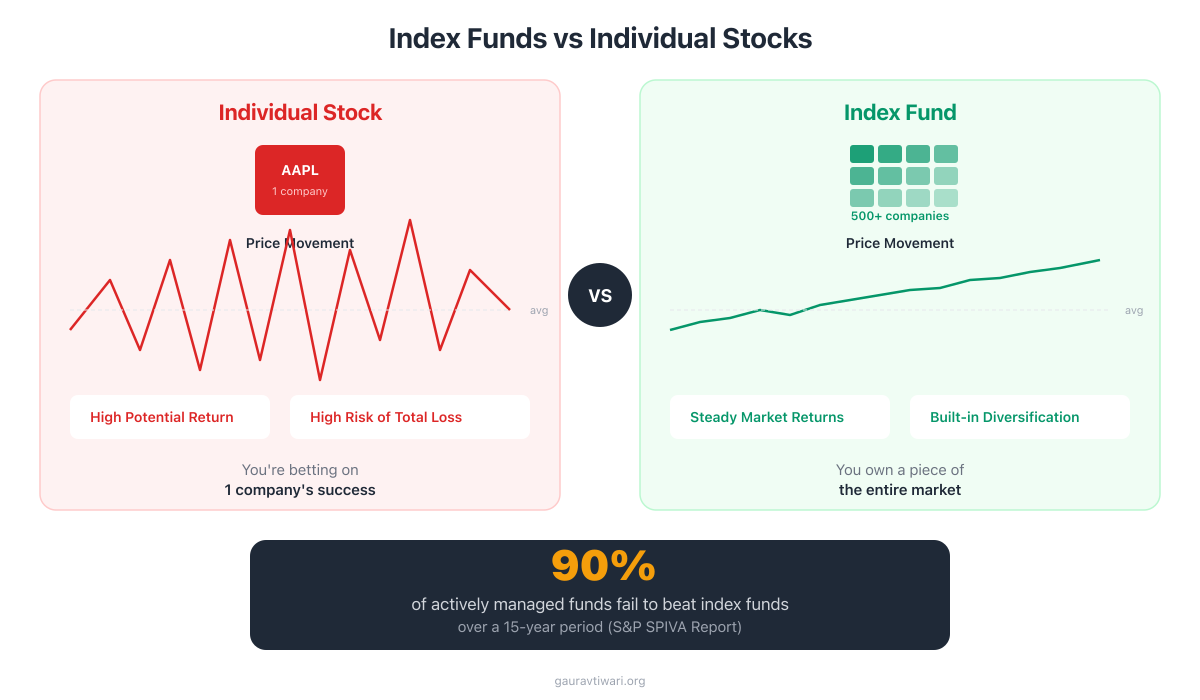

Index funds outperform 90% of actively managed funds over 15-year periods. You don’t need to pick stocks. A single S&P 500 or total market index fund gives you instant diversification across hundreds or thousands of companies with near-zero fees.

How to Start Investing in Stocks

Getting started requires just a few steps. I’m always surprised how people overthink this part.

Open a brokerage account. Online brokers like Fidelity, Schwab, or Vanguard let you buy and sell stocks and funds with zero commissions. The account opening process takes about 15 minutes. You’ll need basic personal information and a bank account for transfers.

Fund your account. Transfer money from your bank. Most brokers allow electronic transfers that take 1-3 business days. Start with whatever you’re comfortable with. There’s no minimum required at most major brokers.

Choose investments. Individual stocks, index funds, or ETFs. For beginners, I strongly recommend starting with a total stock market index fund. One purchase gives you exposure to thousands of companies.

I invest primarily in index funds. I tried picking individual stocks for a while and realized I was spending hours researching for returns that barely matched the S&P 500. Now I automate monthly index fund purchases and spend that time on my business instead. The returns are better and the stress is zero.

Place orders. Decide what to buy and how many shares (or how many dollars to invest, since most brokers offer fractional shares). Click buy. Done.

Monitor and adjust. Review periodically, but resist the urge to check daily. More on this below.

Most beginners are better served by index funds than individual stocks. Index funds provide instant diversification and require no stock-picking skill. I wish I’d started with index funds instead of trying to pick winners. Would have saved me time and made me more money.

Individual Stocks vs. Index Funds

This is the most important decision for new investors, and the answer is usually straightforward.

Individual stocks means you select specific companies to invest in. You might buy Apple, Microsoft, and Amazon because you believe in those businesses. The potential for higher returns exists, but it requires research, time, and genuine skill. You’re competing against professional investors with more resources, more data, and more experience.

Index funds and ETFs are baskets of stocks that track market indexes. A total US stock market index fund holds every publicly traded US company. You don’t pick winners because you own them all. The cost is minimal (often 0.03% annually), and the diversification is automatic.

The evidence is clear. Most professional stock pickers fail to beat index funds over periods of 15+ years. If the professionals can’t do it consistently, individual investors almost certainly can’t either. I tried for years before accepting this reality.

My recommendation for beginners: start with index funds. Build the habit of investing regularly. Learn how markets work by watching your portfolio through ups and downs. If, after a year or two, you want to allocate a small portion (10-15%) to individual stocks as a learning exercise, go ahead. But keep the core in index funds.

A simple portfolio of a total US stock market index fund and a total international stock market index fund gives you exposure to thousands of companies worldwide with minimal effort.

Understanding Risk and Return

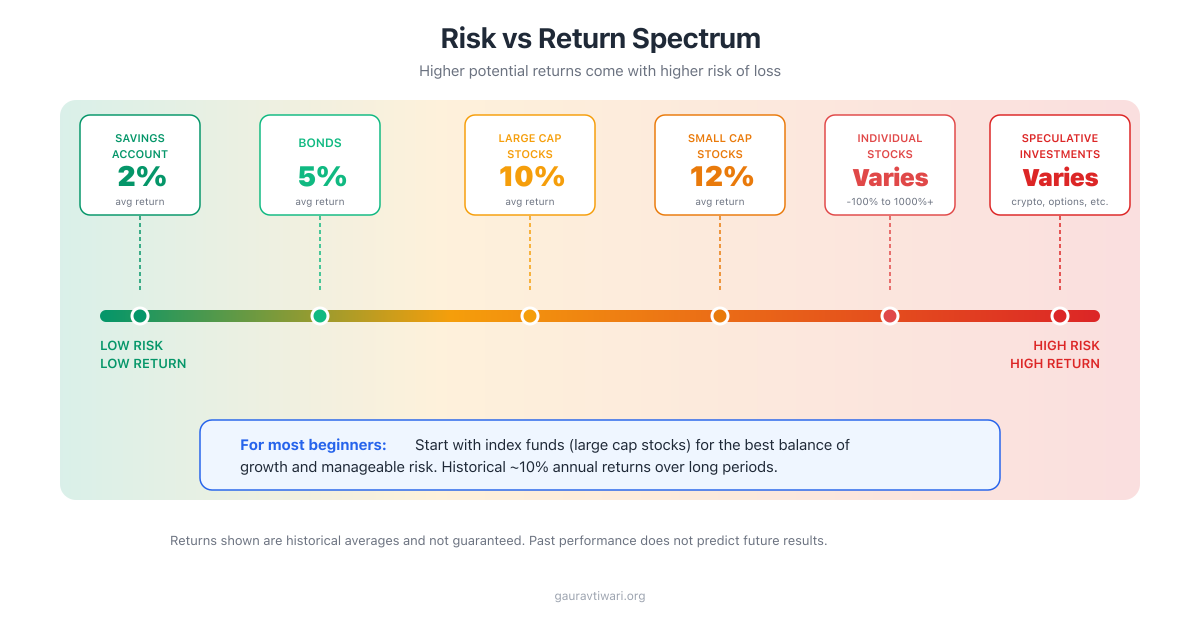

Higher potential returns come with higher risk. This tradeoff is fundamental to all investing.

Stock market risk is real. The market can and does decline, sometimes dramatically. In 2008, stocks dropped about 50%. In 2020, they fell 34% in a month. If you’re not prepared for that possibility, you’ll panic-sell at the worst time.

Historical returns are encouraging. US stocks have returned roughly 10% annually on average over the long term. After adjusting for inflation, that’s about 7%. No other widely accessible asset class has matched that over decades.

Volatility is the price of admission. Stock prices swing dramatically in short periods. That volatility is uncomfortable, but it’s why stocks earn more than savings accounts. The premium return compensates you for enduring the ride.

Time horizon matters enormously. The longer you can stay invested, the more volatility you can tolerate. Over any 20-year period in US market history, stocks have produced positive returns. Over any single year, anything can happen.

Risk tolerance is your emotional ability to handle portfolio declines without making rash decisions. Risk capacity is your financial ability to absorb losses based on your timeline and goals. Both matter.

Young investors with decades until retirement can afford heavy stock exposure. Retirees who need their money soon can’t. Match your stock allocation to your timeline, not your enthusiasm.

Common Beginner Mistakes

I’ve made most of these myself. Learning from my experience is cheaper than learning from your own.

Trying to time the market. Nobody consistently predicts short-term market movements. Not the experts on TV, not the analysts at major banks, not your friend who “called” the last crash. Stay invested. Buy regularly. Stop trying to guess what happens next week.

Panic selling. When markets drop 20-30%, selling feels like the smart move. It’s actually the worst move. You’re locking in losses and missing the recovery that follows. Every major crash has been followed by a recovery. The investors who held through made money. The ones who sold at the bottom didn’t.

Chasing performance. Buying whatever went up the most last year is a recipe for buying high and selling low. Past performance genuinely doesn’t predict future results.

Overtrading. Frequent buying and selling increases costs, triggers tax events, and usually hurts returns. The best investment strategy is boring. Buy, hold, add more, repeat.

Insufficient diversification. Putting all your money in three stocks feels exciting until one of them drops 60%. Diversify broadly. Index funds do this automatically.

Ignoring costs. High fees compound against you over time. A 1% annual fee might sound small, but it can cost you hundreds of thousands over a career of investing.

Making emotional decisions. Fear and greed are the worst investment advisors. Build a plan when you’re calm and rational, then follow it regardless of how you feel day to day.

The best investment approach for most people is simple: buy diversified index funds, contribute regularly, and don’t touch it. Boring? Yes. Effective? Extremely.

How Much to Invest

Start with what you can consistently invest. Consistency matters more than amount.

Build an emergency fund first. Have 3-6 months of expenses saved before investing in stocks. You don’t want to sell investments during an emergency because you have no cash reserves.

Capture employer matches. If your employer matches 401(k) contributions, contribute at least enough to get the full match. That’s an immediate 50-100% return on your money. Nothing else gives you that.

Invest regularly. Dollar-cost averaging, which means investing fixed amounts at regular intervals, removes timing pressure and builds the habit. Set up automatic investments every payday and forget about it.

A common target is saving 15-20% of income for retirement. If that feels impossible right now, start with whatever you can afford. 5% is better than 0%. 10% is better than 5%. Increase it over time as income grows.

Start small if needed. Even $50 or $100 per month builds the habit and begins compounding. The amount matters less than starting. I started with modest amounts that felt almost silly at the time. They don’t feel silly now.

Tax-Advantaged Accounts

Where you invest affects your tax bill significantly. Use the right accounts and you’ll keep more of your returns.

401(k)/403(b) are employer-sponsored retirement accounts. Traditional contributions are tax-deductible now, with taxes paid on withdrawals in retirement. Many employers match contributions up to a certain percentage. Always capture the match.

Traditional IRA is an individual retirement account with potential tax deduction on contributions. Growth is tax-deferred until withdrawal.

Roth IRA is the opposite. Contributions aren’t deductible, but growth and withdrawals are completely tax-free in retirement. If you expect to be in a higher tax bracket later, Roth accounts are powerful.

Taxable brokerage accounts have no tax advantages but also no restrictions on when you can access the money. Use these after you’ve maxed out tax-advantaged options.

The general priority: employer match first, then Roth IRA (if eligible), then max out 401(k), then taxable accounts. The tax savings in retirement accounts compound significantly over decades. I wish I’d understood this priority order in my twenties instead of my thirties.

Long-Term Thinking

Successful stock investing requires patience. Not skill, not luck, not insider knowledge. Patience.

Time in market beats timing the market. Research consistently shows that staying invested beats trying to jump in and out. Missing just the 10 best days in a decade can cut your returns in half.

Compound growth accelerates. Earnings on your earnings create exponential growth over time. The magic happens in the later years, but you only get there by enduring the boring early years.

Short-term noise is just that. Daily price movements, analyst predictions, market commentary… it’s mostly irrelevant to long-term investors. I stopped watching financial news daily and my returns actually improved because I stopped making impulsive decisions.

Check infrequently. Watching your portfolio daily increases anxiety without improving outcomes. I check mine quarterly. That’s plenty.

Decades matter. Most wealth building happens in the final years of compounding, not the first. A 30-year investing timeline means the last 10 years produce more growth than the first 20 combined. That’s counterintuitive but mathematically true.

Think of stock investments as money you won’t need for 10+ years. This mindset helps you ride out volatility instead of reacting to it.

Building Your First Portfolio

Simple portfolios outperform complex ones. Don’t let anyone convince you that you need a complicated setup.

Three-fund portfolio. US stocks, international stocks, and bonds. That’s all most people need. Three funds covering the entire investable world.

Target-date funds are even simpler. These single funds automatically adjust asset allocation as you approach retirement. Pick the fund matching your expected retirement year. One fund, done.

Keep costs low. Expense ratios under 0.20% are reasonable. Under 0.10% is excellent. The difference between 0.03% and 1% seems small until you run the numbers over 30 years. It’s potentially hundreds of thousands of dollars.

Rebalance occasionally. Return to your target allocation annually or when significantly off target. Once per year takes maybe 20 minutes.

Don’t overcomplicate it. More holdings don’t necessarily mean better diversification. A total stock market fund already holds thousands of stocks. Adding more niche funds creates complexity without meaningful benefit.

A simple portfolio you stick with beats a complex portfolio you abandon. Every time.

Starting Today

The best time to start investing was years ago. The second best time is today.

Open an account. Choose a low-cost broker like Fidelity, Schwab, or Vanguard. Takes 15 minutes.

Start with an index fund. A total stock market index fund is an excellent first investment. One purchase, thousands of companies, minimal fees.

Set up automatic contributions. Remove the monthly decision. Money moves from your bank to your brokerage automatically. You’ll barely notice it after a month.

Stay the course. Markets will drop. Probably multiple times during your investing lifetime. Resist the urge to sell. The recovery always comes.

Keep learning. Build knowledge over time, but don’t let learning delay starting. You learn more from investing $100 with skin in the game than from reading 100 articles with nothing invested.

The stock market is how ordinary people build wealth over time. It’s not gambling if you approach it with knowledge, diversification, patience, and reasonable expectations. I started as a complete beginner with no financial background. You can too. The hardest part is clicking “buy” for the first time. Everything after that’s just repetition.

How much money do I need to start investing in stocks?

You can start with very little. Many brokers have no minimum requirements, and fractional shares let you buy portions of expensive stocks for just a few dollars. While you should have an emergency fund first, you don’t need thousands to begin investing. Even $50-100 per month invested in index funds can grow significantly over decades.

Should I buy individual stocks or index funds as a beginner?

Index funds are recommended for most beginners. They provide instant diversification across hundreds or thousands of stocks, require no research or stock-picking skill, and have lower costs. Studies show most professional fund managers fail to beat index funds over time. Start with index funds; add individual stocks later only if you want to dedicate significant time to research.

What’s the difference between a stock and a bond?

Stocks represent ownership in a company. When you buy stock, you own a piece of that company and share in its success or failure. Bonds are loans to a company or government. When you buy a bond, you’re lending money and receiving interest payments. Stocks offer higher potential returns with more risk; bonds offer more stability with lower returns.

Can I lose all my money in the stock market?

With individual stocks, yes—a single company can go bankrupt and its stock can become worthless. With diversified index funds, losing everything is virtually impossible because it would require every company in the index to fail simultaneously. This is why diversification is crucial. Markets can and do decline, sometimes significantly, but diversified portfolios recover over time.

How long should I keep my money in the stock market?

Money you might need within 3-5 years shouldn’t be in stocks—short-term market volatility could mean selling at a loss. For goals 10+ years away, stocks are appropriate despite short-term volatility. Historically, the longer you stay invested, the more likely you are to see positive returns. Think of stock investments as long-term commitments, not short-term plays.