Section 143(1) of Income Tax Act: What Your Intimation Notice Actually Means

My stomach dropped the first time I saw “Intimation under Section 143(1)” in my inbox. This was probably 2012. I’d filed my ITR-1 myself for the first time, clicked submit, felt proud about it, and then two months later got this email from the Income Tax Department with a PDF attached. My first thought was: did I do something wrong?

Turns out, I hadn’t. The intimation was routine. The amount payable column showed zero. All it meant was: “We got your return. We processed it. No issues.” That’s it. But I had no idea at the time, and I spent a genuinely stressful afternoon reading government circulars trying to figure out if I was about to get audited.

If you got one of these notices and you’re confused, this is the article I wish existed back then. I’ll explain what Section 143(1) actually does, what those columns in the intimation mean, when you need to act, and when you can just file it away and move on.

What Section 143(1) Actually Is

Section 143(1) of the Income Tax Act, 1961 is the law that authorizes the Centralized Processing Centre (CPC) in Bengaluru to process your Income Tax Return after you file it. It’s an automated, preliminary assessment, not a full scrutiny. No human ITO (Income Tax Officer) looks at your return at this stage.

The CPC runs a set of computer checks on your filed return. It compares your data against Form 26AS, AIS (Annual Information Statement), TIS (Taxpayer Information Summary), and its own internal calculations. If it finds anything off, it makes an “adjustment” and sends you the intimation notice. If everything matches, it confirms your return as filed.

The intimation under 143(1) isn’t a notice asking you to appear or explain anything. It’s more like a processed receipt. It says: here’s what you declared, here’s what we calculated, here’s the difference (if any). The government has 9 months from the end of the financial year in which you filed your return to send this intimation. So if you filed your ITR for FY 2023-24 in July 2024, they have until December 31, 2025 to send you the 143(1).

One more thing worth knowing: if you don’t receive any intimation within the time limit, your return is considered processed as filed. Silence, in this case, is a good thing.

How the 143(1) Intimation Process Works

The process follows a clear sequence. Understanding it removes a lot of anxiety.

- You file your ITR on the Income Tax e-Filing portal (incometax.gov.in). This could be ITR-1 for salaried individuals, ITR-2 if you have capital gains, ITR-3 or ITR-4 if you have business/professional income.

- Your return goes to the CPC in Bengaluru, which handles all electronically filed returns centrally. Paper returns go through a different process.

- CPC runs automated checks. It computes the total income, verifies TDS credits against Form 26AS/AIS, checks arithmetical accuracy, applies allowable deductions, and compares everything against the Income Tax database.

- Adjustments are made (if any). Under 143(1)(a), CPC can make specific adjustments: arithmetical errors, incorrect claims that are apparent from the return itself, disallowance of loss that exceeds income, and TDS/TCS mismatches. It can’t add income that you didn’t declare, or question the validity of your deductions beyond what’s apparent.

- Intimation is generated and sent. You get it on your registered email and on the e-Filing portal. The subject line is usually “Intimation under Section 143(1) of the Income Tax Act, 1961 for Assessment Year 20XX-XX.” The PDF is password protected: your PAN in lowercase followed by your date of birth in DDMMYYYY format. So for PAN ABCDE1234F and DOB 15 March 1985, the password is abcde1234f15031985.

The password to open your 143(1) intimation PDF is your PAN in lowercase + date of birth in DDMMYYYY format. Example: if PAN is ABCDE1234F and DOB is 15 March 1985, the password is abcde1234f15031985. Save this somewhere. You’ll use it every assessment year.

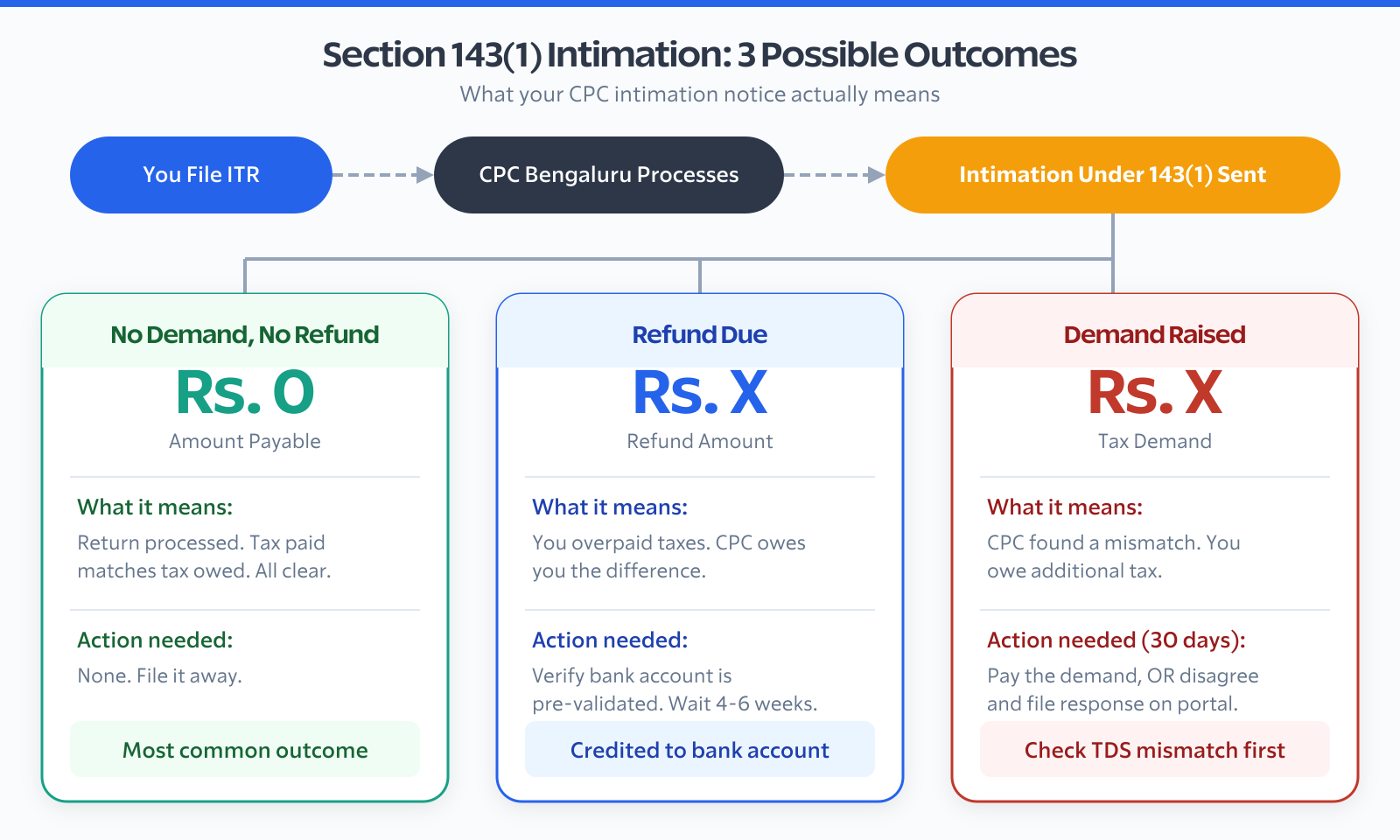

Reading Your 143(1) Intimation: What Each Column Means

The intimation notice has a comparison table. Two columns. Left side: “As provided by taxpayer in the Return of Income.” Right side: “As computed under Section 143(1).” This is where most people get confused.

The rows cover your gross total income, deductions claimed (Chapter VI-A deductions like 80C, 80D, 80G), net taxable income, tax liability, interest under Section 234A/B/C, TDS/TCS/advance tax paid, and the final amount payable or refundable.

Three outcomes are possible after you read that final row:

- Amount payable = 0, refund = 0: Your return is processed. No action needed. This is the most common outcome if your employer correctly deducted TDS and your Form 16 was accurate.

- Refund due: The CPC calculated that you overpaid taxes (usually because excess TDS was deducted). The refund gets credited to your pre-validated bank account, typically within 4-6 weeks. If it’s been more than 3 months, raise a refund reissue request on the portal.

- Demand raised: CPC calculated that you owe additional tax. This happens most often because of TDS mismatch, arithmetic errors, or a disallowance. You have 30 days from the date of the intimation to respond, either by paying the demand or disagreeing with it.

A demand amount that looks alarming is often not a large number once you understand why it’s there. I’ve seen cases where the “demand” is just Rs. 100 in interest under Section 234B because the taxpayer didn’t pay advance tax on freelance income. Annoying, but not a crisis.

One specific thing to watch: the intimation also states an “intimation number.” Note this down. You need it if you want to file a rectification request under Section 154 later.

Section 143(1) vs 143(2) vs 143(3): The Difference Matters

Most people conflate all “income tax notices” into one scary category. They’re not the same. A 143(1) intimation is routine processing. A 143(2) notice is scrutiny. A 143(3) assessment is the most serious. Here’s how they compare:

| Feature | Section 143(1) | Section 143(2) | Section 143(3) |

|---|---|---|---|

| Type | Intimation (automated) | Scrutiny notice | Best judgment / Scrutiny assessment |

| Trigger | Every filed return gets this | Return selected for detailed scrutiny | Non-compliance with 143(2), or non-filing |

| Who processes | CPC Bengaluru (computer) | Assessing Officer (human) | Assessing Officer (human) |

| Action required? | Only if demand is raised or you disagree | Yes, must respond with documents | Yes, mandatory compliance |

| Time limit to issue | 9 months from end of FY of filing | 3 months from end of FY of filing | 12 months from end of FY of 143(2) notice |

| Scope | Limited to arithmetic errors, TDS mismatch, apparent incorrect claims | Can examine any aspect of the return | Can make additions based on AO’s best judgment |

| Severity | Low | Medium-High | High |

| Typical taxpayer | All salaried/self-employed filers | High-value transactions, large refund claims | Non-filers or those who ignored 143(2) |

If you get a 143(2) notice, that’s when you should seriously consider working with a CA. The AO can ask for supporting documents for every deduction you claimed, every transaction in your bank account, and every entry in your books. A 143(1) intimation doesn’t come close to that level.

A Section 143(1) intimation is NOT a scrutiny notice. Getting one doesn’t mean you’re being audited. It means your return was processed. Only if the intimation shows a demand amount do you need to take action. Panic is optional, but definitely not required.

Common Reasons You Get a 143(1) Demand Notice

When the 143(1) does show a demand, here are the most common reasons. I’ve seen most of these personally, either in my own filings or while helping employees and friends sort out their returns.

TDS Mismatch with Form 26AS or AIS

You claimed Rs. 45,000 as TDS credit, but your Form 26AS only shows Rs. 42,000 deposited by your employer. That Rs. 3,000 gap will show up as a demand. This happens when your employer made a mistake in TDS filing, or filed late, or you switched jobs mid-year and the new employer’s TDS hasn’t reflected yet.

Fix: Get your employer to file a corrected TDS return (24Q/26Q). Once the correction is processed, the Form 26AS/AIS updates, and the demand disappears. Don’t just pay the demand without checking this first.

Section 80C Deduction Mismatch

You claimed Rs. 1,50,000 under Section 80C (the maximum), but you forgot that you’d already crossed the limit. Or you claimed a PPF deposit that’s still “pending” and not reflected in your AIS. CPC will disallow the portion it can’t verify.

Incorrect Deduction Codes in ITR Form

This is a surprisingly common issue in ITR-1. You entered a deduction under the wrong schedule, or the ITR utility auto-filled a wrong code. CPC reads the codes, not the intent. If your 80D health insurance premium ended up in the wrong field, it gets ignored.

Interest Income Not Fully Declared

Your savings account interest (above Rs. 10,000 per year for non-senior citizens) is taxable under “Income from Other Sources.” If your bank reported it to the AIS and you didn’t include it, CPC will add it back and recalculate your tax.

Arithmetic Errors

You computed your total income as Rs. 8,50,000 but your ITR form totals actually add up to Rs. 8,65,000. CPC will use the correct figure. Most tax filing software catches this automatically, but if you filled manually or overrode a pre-filled value, this can slip through.

AIS/26AS Mismatch on Capital Gains

You sold mutual fund units and the broker reported the redemption to AIS. If your declared capital gains figure doesn’t match what AIS shows, CPC flags it. This is more common now that AIS includes detailed mutual fund and equity transaction data from depositories and AMCs.

Excess Loss Claim

Under 143(1)(a)(iv), CPC can disallow a loss that has been set off against income in contravention of the Act. For example, if you tried to set off a speculative business loss against salary income (which isn’t allowed), CPC will disallow it.

How to Respond to a 143(1) Intimation Notice

If your intimation shows “Amount Payable = 0” and “Refund = 0,” you don’t need to do anything. Your return is processed. But if there’s a demand or you disagree with the CPC’s calculation, here’s the exact process.

Option 1: Accept the Demand and Pay

If the demand is valid (say, you genuinely forgot to include interest income), the fastest path is to pay. Log in to incometax.gov.in, go to “e-Pay Tax,” select “Income Tax” as the tax applicable, fill in Assessment Year, and choose the correct minor head. Pay via net banking or UPI. Once payment is confirmed, update the response on the portal under “Pending Actions” > “Response to Outstanding Demand.”

Option 2: Disagree and File a Response

If you think the demand is wrong, you can disagree. On the portal, go to “Pending Actions” > “Response to Outstanding Demand” > click on the demand reference number > select “Demand is not correct.” You’ll be asked to select a reason (TDS mismatch, already paid, return under rectification, etc.) and upload supporting documents.

You have 30 days to respond. If you don’t respond, the CPC can adjust the demand against any future refund you’re owed. That means your FY 2024-25 refund could be withheld to recover a demand from FY 2023-24.

Option 3: File a Revised Return (Before the Deadline)

If the intimation highlights an error in your return and you’re within the revised return deadline (December 31 of the Assessment Year), file a revised return instead. A revised return under Section 139(5) supersedes the original. Once processed, a fresh 143(1) intimation will be issued for the revised return.

I’ve done this twice. Once because I forgot to include interest from a post office savings account. Once because I noticed I’d entered the wrong HRA amount. Filing the revised return felt scary at first, but it’s genuinely straightforward if you’re using ClearTax, Taxbuddy, or the government’s own filing utility.

Speaking of which, if you’re dealing with a complex mismatch, Taxbuddy’s guide on responding to 143(1) intimations is worth reading for a step-by-step portal walkthrough. And if you’ve received a formal notice (not just an intimation), their income tax notice response service can help you figure out next steps.

What to Do If You Disagree with the Intimation

Sometimes the demand in the 143(1) is a genuine CPC error, not yours. This happens more often than you’d expect, especially with TDS credits. In that case, you have two routes.

File a Rectification Request Under Section 154

A rectification under Section 154 is the right tool when there’s a “mistake apparent from the record.” This includes situations where CPC didn’t give credit for TDS that’s clearly showing in Form 26AS, or made an arithmetic error in the intimation itself.

On the portal: go to “Services” > “Rectification” > “New Request.” Select the Assessment Year, choose the type of rectification (tax credit mismatch or return data correction), upload the relevant documents, and submit. CPC typically processes rectification requests within 30-90 days. You’ll get a fresh intimation after processing.

One thing to know: a rectification request is not the same as an appeal. You can’t use it to dispute the law or claim a deduction CPC correctly disallowed. It’s only for errors that are apparent and demonstrable from existing records.

Raise a Grievance on the CPC Portal

If your rectification request is stuck or denied incorrectly, raise a grievance through the e-Filing portal under “Grievances” > “Submit Grievance.” Alternatively, call CPC’s helpline at 1800-103-4455 (toll-free) or use the Income Tax Department’s contact page. In my experience, raising a written grievance gets faster results than the helpline because you get a tracking number.

For broader financial context, if you’re a blogger, freelancer, or entrepreneur trying to optimize your tax situation while building multiple income streams, it’s worth understanding that income tax compliance is just one piece. The bigger picture is building passive wealth strategies that reduce your overall tax burden legally through the right instruments.

How to Avoid 143(1) Demands in Future Years

Honestly, the best way to avoid a demand notice is to do your homework before filing, not after. Here’s what I do every year before I submit my ITR.

First, I download my AIS and Form 26AS from the portal and cross-check them against my own records. Income your bank reported, interest from FDs, mutual fund redemptions, credit card high-value transactions, everything is in AIS now. The technology behind e-filing has gotten sophisticated enough that almost all third-party income data flows into the AIS automatically.

Second, I verify all TDS credits. Form 26AS Part A shows what your employers and banks deducted. If any TDS isn’t showing, I chase the deductor to file a corrected TDS return before I file my ITR.

Third, I don’t overstuff deductions. Section 80C has a ceiling of Rs. 1,50,000. Section 80D for health insurance premiums goes up to Rs. 25,000 (Rs. 50,000 for senior citizens). If you’re claiming the maximum, make sure you have receipts or investment proof. CPC may not ask for them now, but a 143(2) scrutiny could.

Fourth, pre-fill and verify. The government’s pre-filled ITR now pulls data from Form 16, Form 26AS, and AIS automatically. Use it as a starting point, but verify every pre-filled field. It’s not always right, especially if you switched employers or have multiple Form 16s.

This kind of discipline isn’t just about avoiding tax notices. It’s a basic habit of financial clarity that feeds into bigger goals like achieving financial freedom on your own terms. You can’t optimize what you’re not tracking.

Frequently Asked Questions

Is a Section 143(1) intimation the same as a tax notice?

No. A 143(1) intimation is a processing communication, not a scrutiny notice. It tells you that CPC has processed your return and whether there’s any difference between what you declared and what CPC calculated. Only a 143(2) notice initiates actual scrutiny where an Assessing Officer gets involved.

How long does it take to get a 143(1) intimation after filing ITR?

CPC has 9 months from the end of the financial year in which you file your return. In practice, most intimations arrive within 2-4 months of filing. If you filed your ITR for FY 2024-25 in July 2025, expect the intimation by September-October 2025 at the latest, though it often comes sooner.

What is the password to open the 143(1) PDF?

The password is your PAN number in lowercase followed by your date of birth in DDMMYYYY format. For example, if your PAN is ABCDE1234F and your DOB is 15 March 1985, the password is abcde1234f15031985. No spaces, no special characters.

I got a demand notice in my 143(1). What happens if I don’t respond?

If you don’t respond within 30 days, the demand becomes a confirmed outstanding demand. CPC can then adjust this against any future refund due to you. If the demand amount exceeds your future refunds, it can be sent for recovery proceedings. Always respond, even if just to disagree with the demand, within the 30-day window.

Can I get a refund even after receiving a 143(1) intimation showing a demand?

Yes, but only if you successfully dispute the demand. If CPC agrees with your rectification request and the demand is reduced to zero, any refund due will be processed. If both a demand and a refund show up in the same intimation (from different assessment years), CPC will typically net them off.

My intimation shows ‘No Demand No Refund.’ Is my return fully processed?

Yes. ‘No Demand No Refund’ means CPC processed your return and the taxes paid match the taxes owed. Your return is considered processed under 143(1). You don’t need to take any action. This is the most common and desirable outcome for salaried taxpayers whose employers correctly deducted TDS throughout the year.

How is Section 143(1) different from Section 143(1)(a)?

Section 143(1) is the parent provision authorizing CPC to process returns. Section 143(1)(a) specifically lists the adjustments CPC is allowed to make: arithmetic errors, incorrect claims apparent from the return, disallowance of losses exceeding income, and TDS/TCS mismatches. CPC cannot go beyond these permitted adjustments at the 143(1) stage. That’s why it’s considered a limited assessment, not a full scrutiny.

The Bottom Line on Section 143(1)

Most 143(1) intimations require zero action from you. The CPC processes millions of returns, sends out intimations, and most of them just say “your return checks out.” That initial panic I felt back in 2012 was completely unnecessary.

When there is a demand, read it carefully before reacting. Check your TDS first. Compare the CPC computation with your Form 26AS and AIS. Most mismatches have an explanation, and most explanations point to either a deductor error or something you can fix with a rectification request. Paying a demand you don’t actually owe is money gone that you probably won’t recover without significant effort.

The only situation where you need to move fast is when the intimation shows a demand and you’re close to the 30-day response deadline. Miss that window and you’ve handed CPC the right to adjust the demand against your future refunds without your consent.

File on time. Check your AIS before filing. Verify your TDS credits. Respond to demands within 30 days. That’s genuinely all it takes to stay out of trouble with 143(1). It’s not complicated once you know what the process actually is.