Tax Planning Strategies for Freelancers and Self-Employed

Nobody tells freelancers about taxes. You figure it out after your first year, usually with a painful surprise.

I owed $15,000 my first year freelancing. I’d been employed before, where taxes were automatic and invisible. Suddenly they weren’t. That lesson cost money, stress, and a lot of late nights with a calculator wondering how I’d missed something so fundamental. The answer was simple: nobody warned me. I’m warning you.

Tax planning for freelancers is fundamentally different from employees. You face self-employment taxes, quarterly payments, and a completely different set of deductions and opportunities. Understanding these differences can save thousands annually. And I mean thousands, not hundreds. Proper tax planning has been one of the biggest financial improvements in my freelance career. This is one of the must-have skills for freelancers managing their own business.

How Self-Employment Taxes Work

Here’s the first thing that shocks new freelancers: you owe an extra 15.3% tax that employees never think about.

Employees pay 7.65% of income toward Social Security and Medicare. Their employers quietly pay another 7.65%. Total: 15.3%. But the employee only sees 7.65% on their paycheck.

When you’re self-employed, you’re both the employee and the employer. You pay the full 15.3%. This applies to all net self-employment income regardless of whether you owe any regular income tax. Even if your income is low enough to pay zero federal income tax, you still owe self-employment tax.

This hits hard because it’s invisible until you file. Employees never think about the employer portion because it’s not on their paycheck. Freelancers feel the full weight of both sides.

For 2024, Social Security applies to the first $168,600 of earnings. Medicare applies to all earnings, with an additional 0.9% on income above $200,000 (single) or $250,000 (married filing jointly).

On $100,000 of freelance income, you’ll owe approximately $14,130 in self-employment taxes alone. That’s before considering federal and state income taxes. When I first calculated this number for my own income, I understood why that first year surprise was so brutal.

On $100,000 of freelance income, expect approximately $14,130 in self-employment taxes alone, before federal and state income taxes. This is the number that shocks every new freelancer.

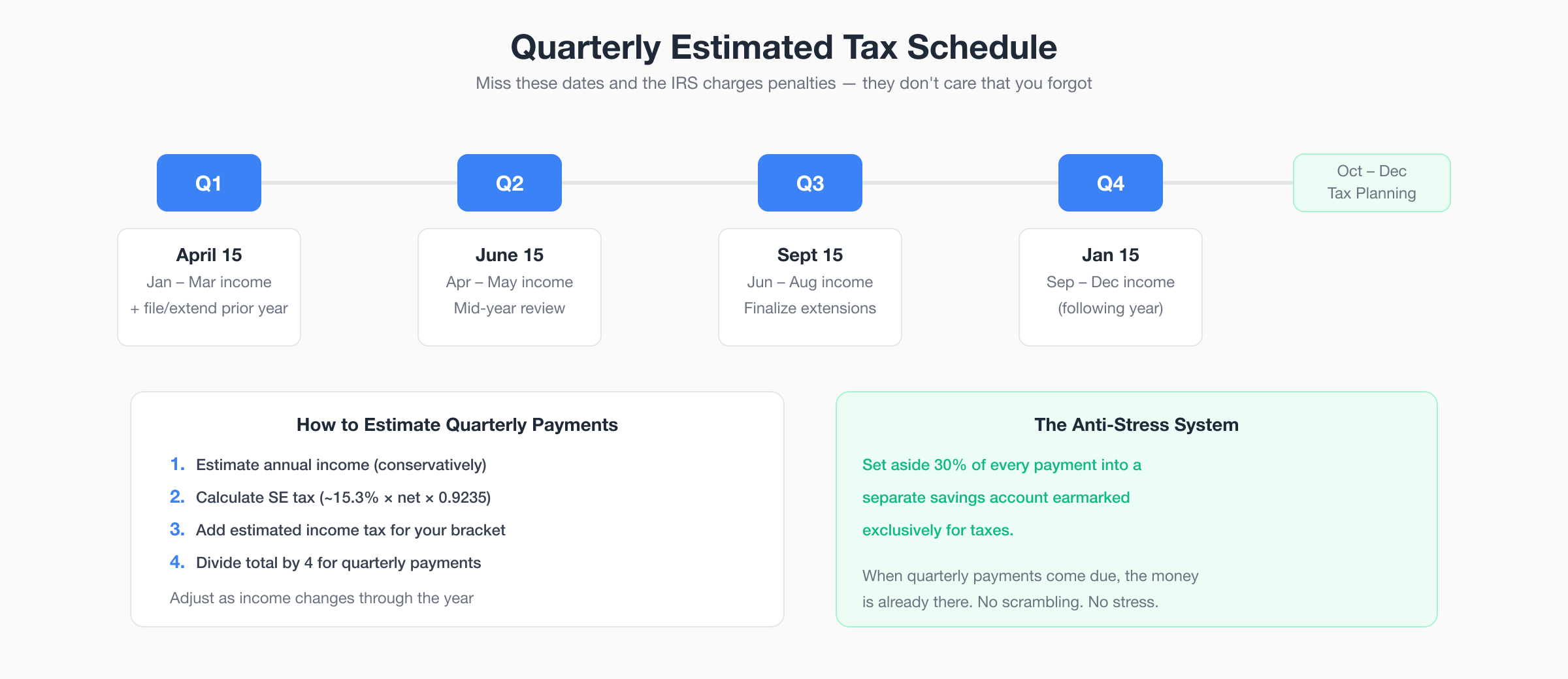

Quarterly Estimated Taxes

Employees have taxes withheld from each paycheck automatically. Freelancers don’t have that luxury. You must pay quarterly estimated taxes throughout the year or face penalties.

The due dates are fixed:

- Q1: April 15

- Q2: June 15

- Q3: September 15

- Q4: January 15 (following year)

You’re required to pay quarterly if you expect to owe over $1,000 for the year. Missing payments or underpaying results in interest charges and penalties from the IRS. They don’t care that you forgot or that your income was unpredictable.

Here’s how to estimate your quarterly payments:

- Estimate your annual income (conservatively)

- Calculate self-employment tax (roughly 15.3% of net income times 0.9235)

- Add estimated income tax based on your bracket

- Divide by four for quarterly payments

This is rough by design. Income fluctuates, especially for freelancers. Adjust quarterly payments as you get better information throughout the year. Pay more in quarters where you earned more, less when income was lower.

My system: I set aside 30% of every payment I receive into a separate savings account earmarked exclusively for taxes. When quarterly payments come due, the money is already sitting there. No scrambling, no cash flow crisis. This single habit eliminated all tax-related stress from my freelance life.

The Self-Employment Tax Deduction

One bright spot in the self-employment tax picture: you can deduct half of your self-employment tax from your income.

If your SE tax is $14,000, you deduct $7,000 from your taxable income. This is an above-the-line deduction, which means it’s available whether you itemize deductions or take the standard deduction.

It doesn’t eliminate the SE tax burden, but it softens it meaningfully. On a 22% marginal tax rate, that $7,000 deduction saves you about $1,540 in income tax. Not nothing.

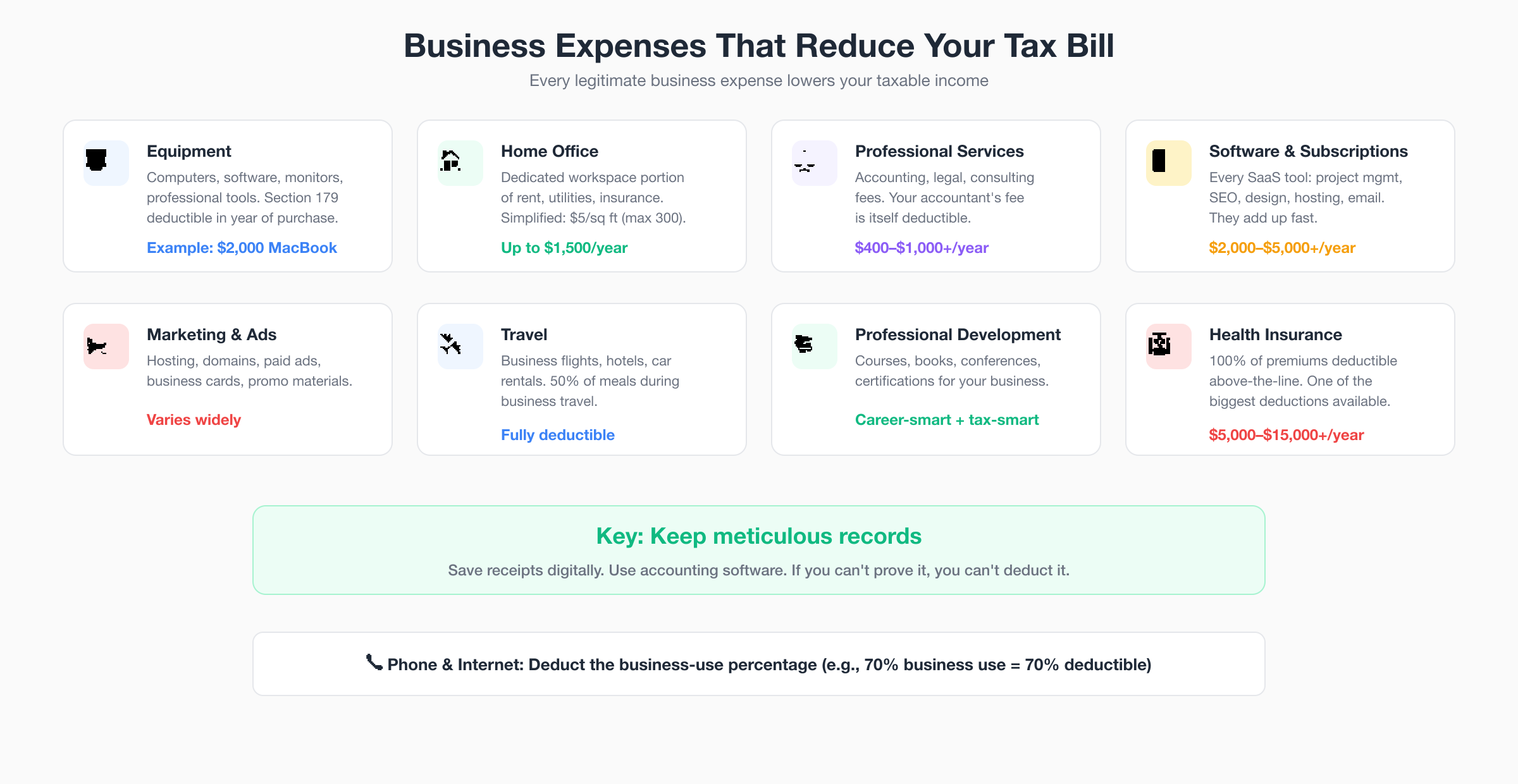

Business Expenses That Reduce Your Tax Bill

Every legitimate business expense reduces your taxable income. The more expenses you document properly, the lower your tax bill. This is where freelancing actually offers advantages over employment.

Equipment. Computers, monitors, software, cameras, professional tools. Often deductible in full in the year of purchase under Section 179. That $2,000 MacBook you need for work? Deductible. It reduces your taxable income by $2,000, saving you roughly $500-700 in taxes depending on your bracket.

Home office. If you work from home regularly and exclusively in a dedicated space, you can deduct a portion of rent or mortgage interest, utilities, and insurance. The simplified method allows $5 per square foot up to 300 square feet ($1,500 deduction). The actual expense method can be higher but requires more record-keeping. I use the simplified method because it’s easier and the difference is small for my office size.

Professional services. Accounting, legal, consulting fees related to your business. Your accountant’s fee is itself a deductible business expense.

Software and subscriptions. Every business tool you pay for is deductible. Project management tools like ClickUp, SEO tools like Semrush, design software, hosting, email services. I deduct every SaaS subscription that supports my business, and they add up to several thousand dollars annually.

Marketing and advertising. Website hosting, domain names, paid advertising, business cards, promotional materials.

Travel. Business travel expenses including flights, hotels, car rentals, and 50% of meals during business travel. Client meetings, conferences, and industry events all qualify.

Professional development. Courses, books, conferences, certifications relevant to your business. Investing in your skills is both career-smart and tax-smart.

Health insurance. Self-employed individuals can deduct 100% of health insurance premiums as an above-the-line deduction. This is one of the most significant deductions available. My health insurance premium deduction saves me thousands annually.

Phone and internet. The business-use percentage of your phone and internet bills. If you use your phone 70% for business, 70% of the bill is deductible.

The key to all of this: keep meticulous records. Save receipts (digital photos are fine). Use accounting software to categorize expenses throughout the year, not just at tax time. If you can’t prove an expense to the IRS, you can’t deduct it.

The QBI Deduction (Qualified Business Income)

This deduction is one of the biggest tax benefits for freelancers, and many don’t even know it exists.

If you’re a sole proprietor, partnership member, or S-Corp shareholder, you may deduct up to 20% of your qualified business income from your taxable income. That’s huge.

On $100,000 in qualified business income, you could get a $20,000 deduction. Depending on your bracket, that saves $4,000-6,000 in taxes. For doing nothing except being self-employed.

Limitations apply, and this is where it gets complicated:

Specified service businesses (consulting, law, health, financial services, performing arts, and similar) see the deduction phase out as taxable income exceeds $182,100 (single) or $364,200 (married filing jointly) for 2024. Below those thresholds, you get the full deduction. Above them, it reduces and eventually disappears.

W-2 wage limitations apply for high earners in non-specified businesses. If you don’t have employees, this can limit the deduction at higher income levels.

The rules are genuinely complex. This is one area where paying an accountant absolutely pays for itself. The QBI deduction alone can save more than an accountant costs.

The QBI deduction alone saves me more every year than my accountant’s entire fee. If you’re not claiming it, you’re leaving thousands on the table. This is the single biggest argument for working with a tax professional who understands self-employment.

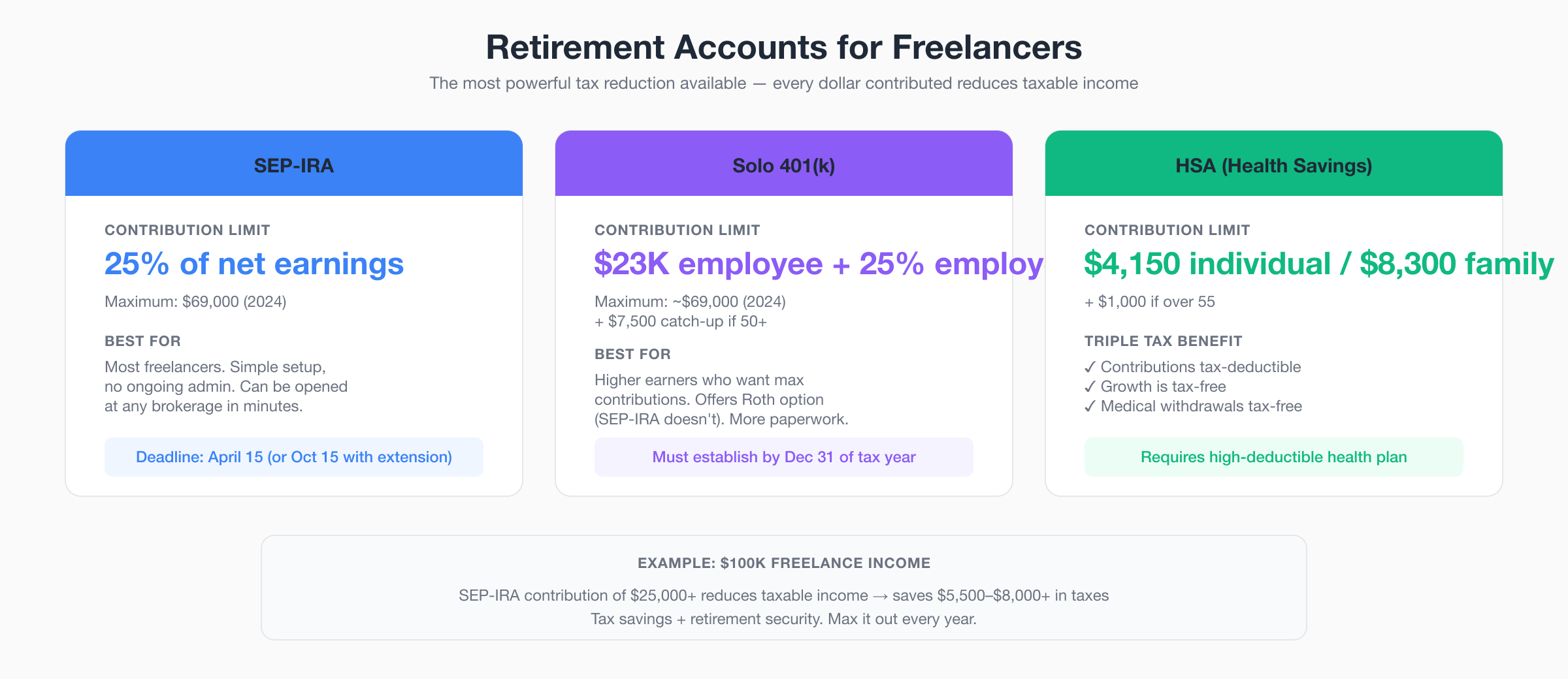

Retirement Account Contributions

Retirement accounts provide the most powerful tax reduction available to self-employed people. The contribution limits are generous, and every dollar contributed reduces your taxable income.

SEP-IRA. You can contribute up to 25% of net self-employment earnings, with a maximum of $69,000 for 2024. Contributions are fully tax-deductible. Setup is simple (most brokers can open one in minutes), and there’s no ongoing administration. This is where I started, and it’s what I recommend for most freelancers.

Solo 401(k). Even higher potential contribution than a SEP-IRA. You can make both an employee contribution ($23,000 for 2024, plus $7,500 catch-up if over 50) and an employer contribution (25% of net earnings). Total maximum is around $69,000. The Solo 401(k) also offers a Roth option, which the SEP-IRA doesn’t. More paperwork, but more flexibility.

SIMPLE IRA. Lower limits than SEP or Solo 401(k), but it allows employee contributions and is a good bridge if you’re planning to hire employees eventually.

A freelancer earning $100,000 could contribute over $25,000 to a SEP-IRA, reducing taxable income by that amount and cutting taxes by $5,500-8,000+ depending on bracket. That’s real money saved while simultaneously building retirement security.

The deadline for opening and funding a SEP-IRA is April 15 (or October 15 with an extension) for the prior tax year. Solo 401(k) must be established by December 31 of the tax year, though contributions can be made until the filing deadline.

I max out my retirement contributions every year. It’s the single most effective tax strategy available to freelancers.

S-Corporation Election

For higher-earning freelancers, electing S-Corp status can reduce self-employment taxes by thousands annually. This is the most sophisticated strategy in this guide, and it’s worth understanding.

As a sole proprietor, all net income is subject to self-employment tax (15.3%). Every dollar you earn, the full 15.3% applies.

As an S-Corp, only the salary you pay yourself is subject to employment taxes. Remaining profits pass through as distributions, which avoid self-employment taxes entirely.

Example: $150,000 in freelance income.

As sole proprietor: approximately $21,000 in self-employment taxes.

As S-Corp with $75,000 salary and $75,000 in distributions:

- Employment taxes on $75,000 salary: approximately $11,500

- Self-employment taxes on $75,000 distribution: $0

- Savings: approximately $9,500 per year

That’s real money. But there are requirements and costs:

Reasonable salary. The IRS requires you to pay yourself “reasonable compensation” for the work you do. You can’t take a $10,000 salary and $140,000 in distributions. The IRS knows this trick and will audit it. The salary should be comparable to what you’d pay someone else to do your job.

Payroll complexity. You must run actual payroll, withhold taxes, file payroll tax returns, and handle year-end W-2s. This means payroll software or a payroll service.

Additional costs. Payroll services run $30-100/month. You’ll need more accounting support. Some states charge additional S-Corp fees.

When it makes sense. Generally above $60,000-80,000 in net self-employment income, the tax savings outweigh the additional costs and complexity. Below that, the savings are too small to justify the hassle.

I consulted with a tax professional before making this decision, and I’d recommend the same for anyone considering it. The math depends on your specific situation.

Health Savings Account (HSA)

If you have a high-deductible health plan (HDHP), an HSA is the single most tax-advantaged account in the entire tax code.

Triple tax benefit: contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. No other account offers this combination. Not a 401(k). Not a Roth IRA. Only the HSA.

For 2024, individuals can contribute up to $4,150; families up to $8,300. Add $1,000 if over 55.

For freelancers who already deduct health insurance premiums, the HSA adds additional tax reduction while building funds for future medical expenses. It’s an extra layer of tax efficiency on top of the insurance deduction.

Here’s the power move: if you can afford to pay medical expenses out of pocket, let the HSA grow invested. After 65, HSA funds can be used for any purpose, taxed as ordinary income like a traditional IRA. Before 65, non-medical withdrawals face taxes plus a 20% penalty, so keep the funds for medical use until then.

Record Keeping and Documentation

Every deduction you claim needs to survive an audit. The IRS can audit returns from the past three years (or six if they suspect significant underreporting). Prepare accordingly.

Separate business banking. This is non-negotiable. Don’t mix personal and business expenses. Separate checking accounts and credit cards for business make record keeping clear and audits simple. I opened a dedicated business checking account and credit card my first year freelancing, and it’s saved me hours of sorting every tax season.

Use accounting software. FreshBooks, Zoho Books, Wave, or QuickBooks. Categorize expenses throughout the year, not just at tax time. The January scramble to sort 12 months of expenses is miserable and error-prone.

Keep receipts digitally. Paper receipts fade and get lost. Take photos of every business receipt immediately. Apps like Expensify capture and organize automatically. I snap a photo within 30 seconds of any business purchase. It’s become automatic.

Log mileage. If you deduct vehicle expenses using the standard mileage rate, log every business trip. Date, destination, purpose, miles. Apps like MileIQ automate this with GPS tracking.

Document home office. Measure your dedicated workspace. Keep records of total housing expenses. The IRS may ask for proof that the space is used regularly and exclusively for business.

Good records make tax preparation faster, cheaper, and safer. They also save you money by ensuring you don’t miss legitimate deductions.

Common Freelancer Tax Mistakes

Not setting aside money for quarterly payments. This is the number one mistake I see. April’s tax bill shouldn’t be a surprise. Set aside 25-30% of every payment received throughout the year. Separate account. Don’t touch it except for tax payments.

Missing legitimate deductions. If it’s a business expense, deduct it. Many freelancers leave thousands on the table by not tracking expenses carefully. That conference ticket, that software subscription, that business book. All deductible. All often forgotten.

Mixing personal and business finances. Creates audit risk and makes record keeping exponentially harder. One business account, one personal account. Clean separation.

Skipping retirement contributions. It’s free tax reduction combined with retirement security. There’s no reason to skip it. Even small contributions add up, and the tax savings are immediate.

DIY when complexity warrants help. A good accountant saves more than they cost for most freelancers earning above $50,000-75,000. The deductions they find, the strategies they suggest, and the mistakes they prevent more than justify their fee.

Not paying quarterly. Penalties accumulate. The IRS charges interest on underpayments. Just automate the quarterly payments and avoid the headache entirely.

Working With a Tax Professional

At some point, professional help pays for itself. For me, that point came in year two of freelancing when my accountant found deductions I’d completely missed, saving me more than double his fee.

Signs you need professional help:

- Income above $75,000+

- Considering S-Corp election

- Multiple income streams

- Business-related legal structure decisions (LLC, S-Corp)

- Prior audit or complex tax situation

- Significant business expenses to categorize

Find a CPA or Enrolled Agent experienced with self-employment taxes. Ask specifically about experience with freelancers and solo businesses. Not all accountants understand the freelance world.

Expect to pay $400-1,000+ for annual tax preparation. That investment typically recovers through proper deductions and avoided mistakes.

A good tax professional does more than file returns. They help with planning throughout the year, quarterly estimate calculations, business structure decisions, and proactive strategies that reduce your tax burden before December 31. Mine has saved me more money than any other professional relationship in my business.

Tax Planning Calendar for Freelancers

Proactive planning all year beats reactive scrambling in April. Here’s the rhythm I follow.

January. Review the prior year. Gather all documents for tax filing. Fund retirement accounts for the prior year if not yet maxed. Start planning for the current year’s strategy.

April 15. File or extend the prior year return. Pay Q1 estimated taxes for the current year. Last chance to fund prior year’s SEP-IRA contributions.

June 15. Pay Q2 estimated taxes. Mid-year review of income and expenses. Adjust estimated payments if income is tracking higher or lower than expected.

September 15. Pay Q3 estimated taxes. Finalize any extensions from April. Start thinking about year-end tax planning.

October through December. This is tax planning season. Estimate final annual income. Maximize deductions before December 31 (equipment purchases, retirement contributions, charitable giving). Consider timing of expenses and income for optimal tax treatment.

January 15. Pay Q4 estimated taxes. The cycle restarts.

The Bottom Line

Freelance taxes are more complex than employee taxes. No argument there. But they also offer more opportunities for reducing what you owe.

Self-employment taxes add burden, but business expense deductions, the QBI deduction, retirement accounts, health insurance deductions, and potentially S-Corp savings can significantly reduce your effective tax rate compared to employees earning the same income.

The key is understanding the rules and planning proactively. Many freelancers pay more than necessary because they don’t know the opportunities available. Don’t be one of them.

Invest in learning the basics. Invest in professional help when the complexity warrants it. And never, ever let April’s tax bill be a surprise. I learned that lesson once. It cost me $15,000 and months of stress. You can learn it from reading this instead.

Frequently Asked Questions

What is self-employment tax?

Self-employment tax is the Social Security and Medicare tax for self-employed individuals. Employees pay 7.65% with employers matching. As a freelancer, you pay both portions: 15.3% on net self-employment income. This applies regardless of whether you owe income tax. On $100,000 of freelance income, expect approximately $14,130 in self-employment taxes.

How much should freelancers set aside for taxes?

Set aside 25-30% of each payment in a separate savings account for taxes. This covers both self-employment tax (15.3%) and federal income tax. Your actual rate depends on income level and deductions, but 25-30% provides safe coverage. Use this fund for quarterly estimated payments due April 15, June 15, September 15, and January 15.

What is the QBI deduction for self-employed?

The Qualified Business Income deduction allows self-employed individuals to deduct up to 20% of qualified business income from taxable income. On $100,000, this could mean a $20,000 deduction, reducing taxes by $4,000-6,000. Limitations apply for specified service businesses (consulting, law, health) at higher income levels. The rules are complex but the savings are substantial.

Should freelancers elect S-Corp status?

S-Corp election can reduce self-employment taxes significantly for higher earners. Only salary is subject to employment taxes, not distributions. Generally makes sense above $60,000-80,000 in net self-employment income where savings outweigh added complexity. Requires reasonable salary, payroll administration, and additional filings. Consult a tax professional before electing.

What retirement accounts can freelancers use?

SEP-IRA allows contributions up to 25% of net self-employment earnings, maximum $69,000 for 2024. Solo 401(k) allows even higher contributions with both employee and employer portions. Both reduce taxable income dollar-for-dollar. A freelancer earning $100,000 could contribute over $25,000, cutting taxes by $5,500-8,000+ while building retirement savings.

Disclaimer: This site is reader-supported. If you buy through some links, I may earn a small commission at no extra cost to you. I only recommend tools I trust and would use myself. Your support helps keep gauravtiwari.org free and focused on real-world advice. Thanks. - Gaurav Tiwari