The Complete Guide to Raising Startup Capital

Some businesses can be bootstrapped from savings and early revenue. Others require external capital to start. The difference often comes down to business model, growth speed requirements, and capital intensity. If you need money beyond what you can personally provide, you enter the world of startup fundraising.

I’ve been on both sides of this equation. I bootstrapped my own businesses from day one, growing entirely from revenue without a single external dollar. But I’ve also worked with clients who raised venture capital, angel funding, and everything in between. Watching their journeys taught me something important: raising capital is a skill most entrepreneurs have to learn the hard way. The process is time-consuming, often humbling, and distracting from actually building the business.

But for capital-intensive ventures or those requiring rapid scaling, outside funding may be the only path forward. This guide covers the fundamentals, what options exist, how to approach each, and what to expect from the experience.

Do You Need to Raise Capital?

This is the first question, and most people answer it wrong. They assume they need funding when they actually need better business model design.

Start by honestly assessing bootstrapping viability. Can the business generate revenue quickly enough to fund growth? Many businesses don’t need external capital, and the ones that take it often give up more than they realize.

Consider capital intensity. Does the business require significant upfront investment before any revenue flows? Manufacturing, inventory-heavy models, and research-intensive products genuinely need capital. A SaaS product or consulting practice usually doesn’t.

Think about speed requirements. Is there a genuine window of opportunity requiring faster growth than organic revenue allows? “We need to grow fast” isn’t the same as “the market window closes in 18 months.” The first is a preference. The second might justify fundraising.

Evaluate competitive pressure honestly. Are well-funded competitors forcing the pace of investment? Or are you just feeling anxious because someone else raised money? I’ve watched bootstrapped companies outperform venture-backed competitors because they were forced to find product-market fit before spending. That constraint turned out to be an advantage.

Consider your personal resources and revenue timeline. What can you invest yourself? How long until the business can sustain itself? Can you bridge that gap without investors?

Always weigh the equity cost. Raising capital means giving up ownership. I’ve seen founders end up with 15% of companies they built because they raised too much, too early, at too low a valuation. That’s a painful outcome.

Not every startup should raise capital. For those that should, understanding the options is essential.

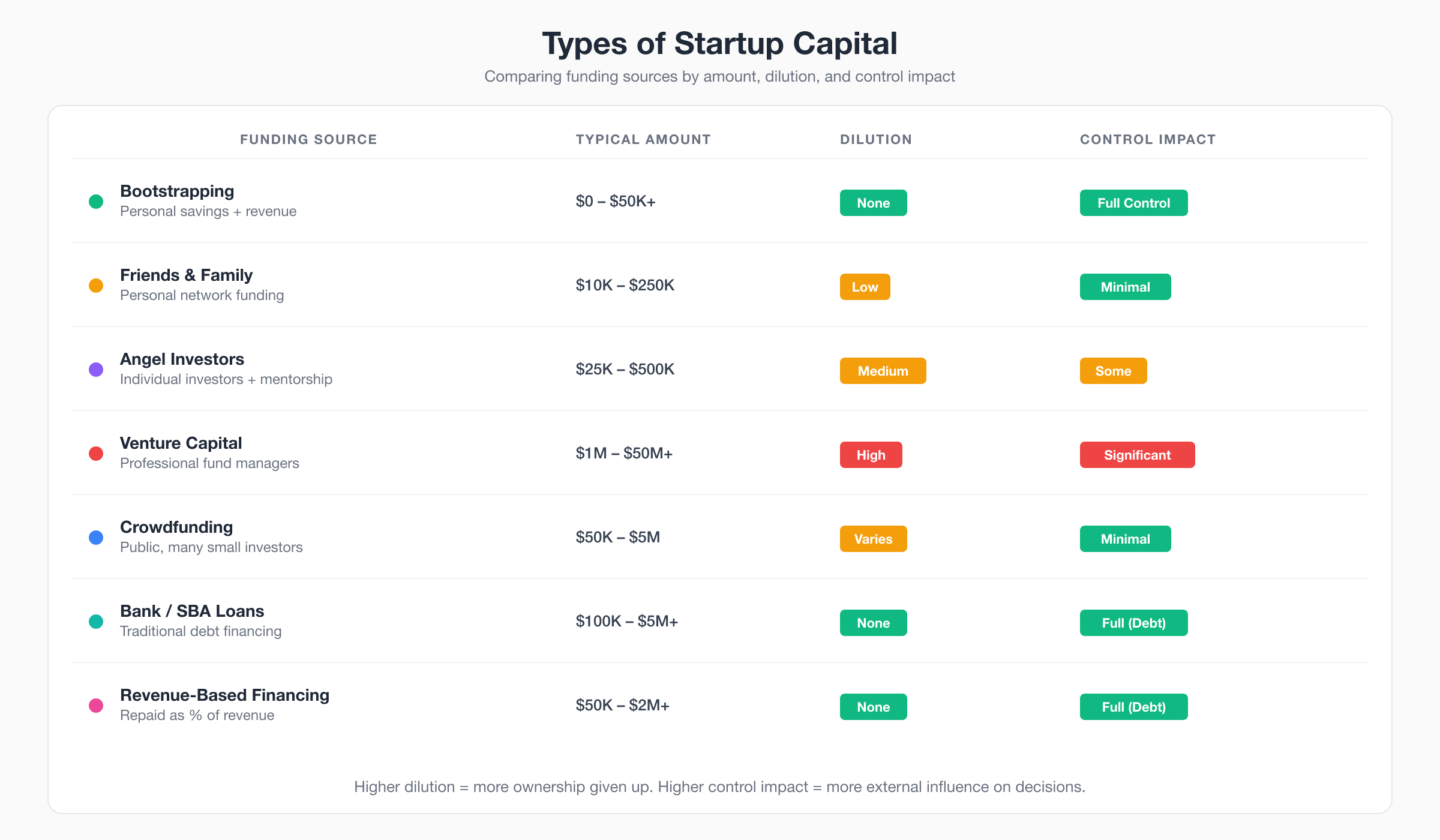

Types of Capital

The funding landscape has more options than most people realize.

Bootstrapping means using your own savings, credit, and early revenue. Full control, no external obligations. This is how I built my businesses, and I’d do it the same way again. The discipline of bootstrapping forces smart decisions that venture-funded companies often skip.

Friends and family funding is often the earliest outside capital. Money from personal relationships comes with simpler terms but higher relationship risk. I’ve watched friendships dissolve over failed startup investments. Be extremely clear about the risks before taking money from people you care about.

Angel investors are wealthy individuals investing personal funds at earlier stages, typically $25,000 to $500,000. They often provide expertise, connections, and mentorship alongside capital. Finding the right angel who understands your industry can be transformative.

Venture capital comes from professional investment firms. Larger amounts, significant structure and expectations. VCs manage funds from institutions and wealthy individuals, investing $1 million to $50 million or more depending on stage. This is appropriate for businesses with potential for very large outcomes and rapid scaling.

Crowdfunding raises many small investments from the public through various models, whether equity, rewards, or donation-based. Different regulations apply depending on the model and jurisdiction.

Bank loans and SBA loans represent traditional debt financing. Requires creditworthiness and often collateral. SBA loans are government-backed and more accessible, but both are still debt you’ll need to repay.

Revenue-based financing is a newer model gaining popularity. Capital gets repaid as a percentage of revenue, making it less dilutive than equity and more flexible than traditional debt.

And grants from government or foundations provide non-dilutive funding. Competitive and often come with specific requirements, but they’re free money if you qualify.

Different funding sources suit different stages, business types, and founder preferences.

Bootstrapping Considerations

If you can fund yourself, seriously consider it. I’m biased here because bootstrapping worked for me, but the advantages are real.

Personal savings represent what you can invest without devastating personal finances. The key word is “without devastating.” I’ve seen founders drain retirement accounts for startup ideas that weren’t validated. Don’t bet everything on an untested hypothesis.

Credit options like personal credit cards and lines of credit are risky but sometimes necessary for bridging short gaps. I used credit strategically during my early years, but I always had a clear plan for paying it off within months.

Side income from maintaining employment while building is the approach I recommend most. Longer timeline but dramatically lower risk. I built my first products while still taking client work, which meant slower growth but zero financial pressure.

Customer funding through pre-orders, deposits, and early contracts uses revenue as capital. This is my favorite form of funding because it validates demand while providing capital. If customers won’t pay in advance, that tells you something important.

Building with a minimal viable approach, investing the absolute minimum to validate before committing heavily, is smart regardless of your funding source. I’ve watched clients spend hundreds of thousands building products nobody wanted. Validate first.

And consider lifestyle business design. Models that work with limited capital, like consulting and services, often require less upfront investment than people assume.

Bootstrapping preserves equity and control. It’s often underrated as a strategy, especially in a culture that celebrates fundraising as an achievement rather than the trade-off it actually is.

The Fundraising Process

If you decide to raise capital, here’s what actually happens.

Preparation comes first. You’ll need a pitch deck, a financial model, and a data room with key documents like corporate structure, contracts, and team information. Have your business plan articulated clearly. It doesn’t need to be 50 pages, but it needs to demonstrate you understand the opportunity and your approach.

Targeting means identifying appropriate investors who match your stage, sector, and fit. Not all money is the same. Wrong investors create wrong incentives. Do your research on who invests in businesses like yours.

Warm introductions get you in the door. Cold outreach rarely works. The best path is through other founders, advisors, or mutual connections who can vouch for you.

First meetings are usually 30 to 60 minutes. You’re telling your story, answering questions, and trying to build genuine interest. Think of it as a conversation, not a presentation.

Follow-up conversations go deeper with interested investors. Multiple meetings are typical. Each one gets more detailed about your business, market, and plans.

Due diligence is the detailed investigation of your business, market, team, and claims. Be honest, because anything you misrepresent will surface here.

The term sheet outlines investment terms. It’s non-binding but sets the framework for negotiation. This is where having legal counsel becomes critical.

And closing involves final documents, signatures, and wire transfer. It often takes weeks after the term sheet, sometimes longer.

The entire process typically takes 3 to 6 months from first meetings to closing. Sometimes longer. This is full-time work alongside running your actual business, which is why fundraising is so exhausting.

The Pitch Deck

Your pitch deck is your primary tool for generating investor interest.

Start with the problem statement. What problem are you solving? Why does it matter? The best pitch decks make the problem feel urgent and personal.

Then your solution. Your approach and why it’s better than alternatives. Be specific about what makes your approach different.

Market opportunity covers how big the opportunity is and who the customers are. Investors need to see a path to significant returns.

Your business model explains how you make money. Pricing and revenue streams should be clear and defensible.

Traction shows what you’ve achieved so far, whether that’s revenue, users, partnerships, or product progress. Something beyond ideas. The more traction you have, the better your terms will be.

Competition covers who else is doing this and why you’ll win. Saying “no competition” is a red flag. Every idea has competition or alternatives.

Team explains why these specific people are uniquely positioned to succeed. Demonstrate capability and relevant experience.

Financials show projections with a path to returns. Usually optimistic but defensible. Investors expect ambition but also want to see you understand the numbers.

And the ask states how much you’re raising and what you’ll do with the capital. Be specific about milestones.

Keep the deck to 10 to 15 slides. Investors see hundreds of pitches. Respect their time.

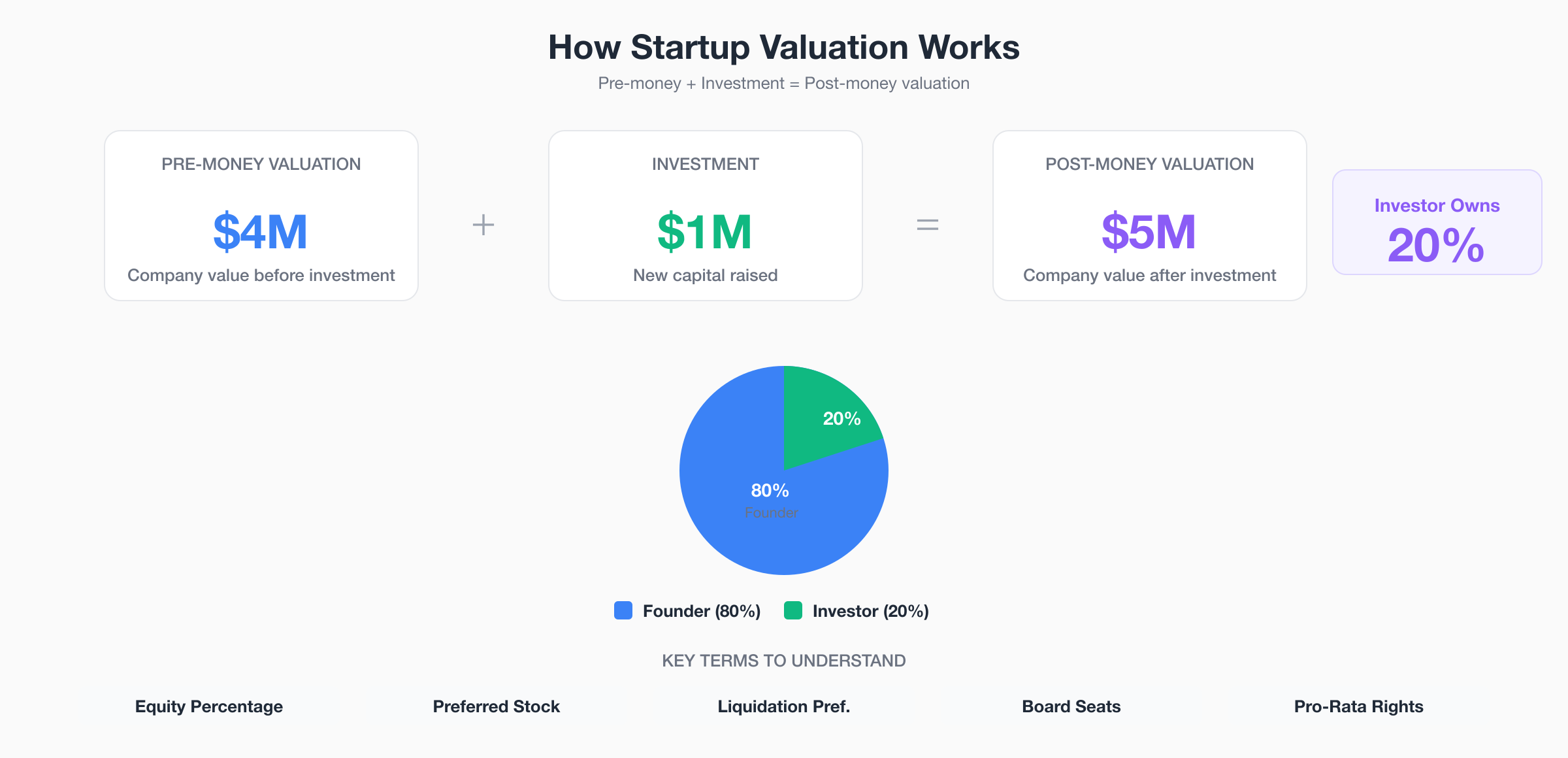

Valuation and Terms

Understanding valuation math and investment terms is essential for negotiating effectively.

Pre-money valuation is your company’s value before new investment. Post-money valuation is that plus the investment amount. If your pre-money is $4 million and someone invests $1 million, the post-money is $5 million and the investor owns 20%.

Early stage valuation is more art than science. It’s based on market conditions, team strength, traction, and comparable deals in your sector. Don’t optimize only for maximum valuation. Investor quality, terms, and partnership matter more than the number on the term sheet. I’ve seen founders accept terrible terms at high valuations and regret it later.

Key terms to understand include equity percentage (what investors receive), preferred stock (investor shares with special rights), liquidation preference (how proceeds are distributed in exits, with investors often getting their money back first), board seats (governance rights), pro-rata rights (maintaining ownership in future rounds), anti-dilution provisions, and vesting schedules for founder shares.

Get legal counsel who knows startup financing. Terms matter more than they seem during the excitement of receiving an investment offer.

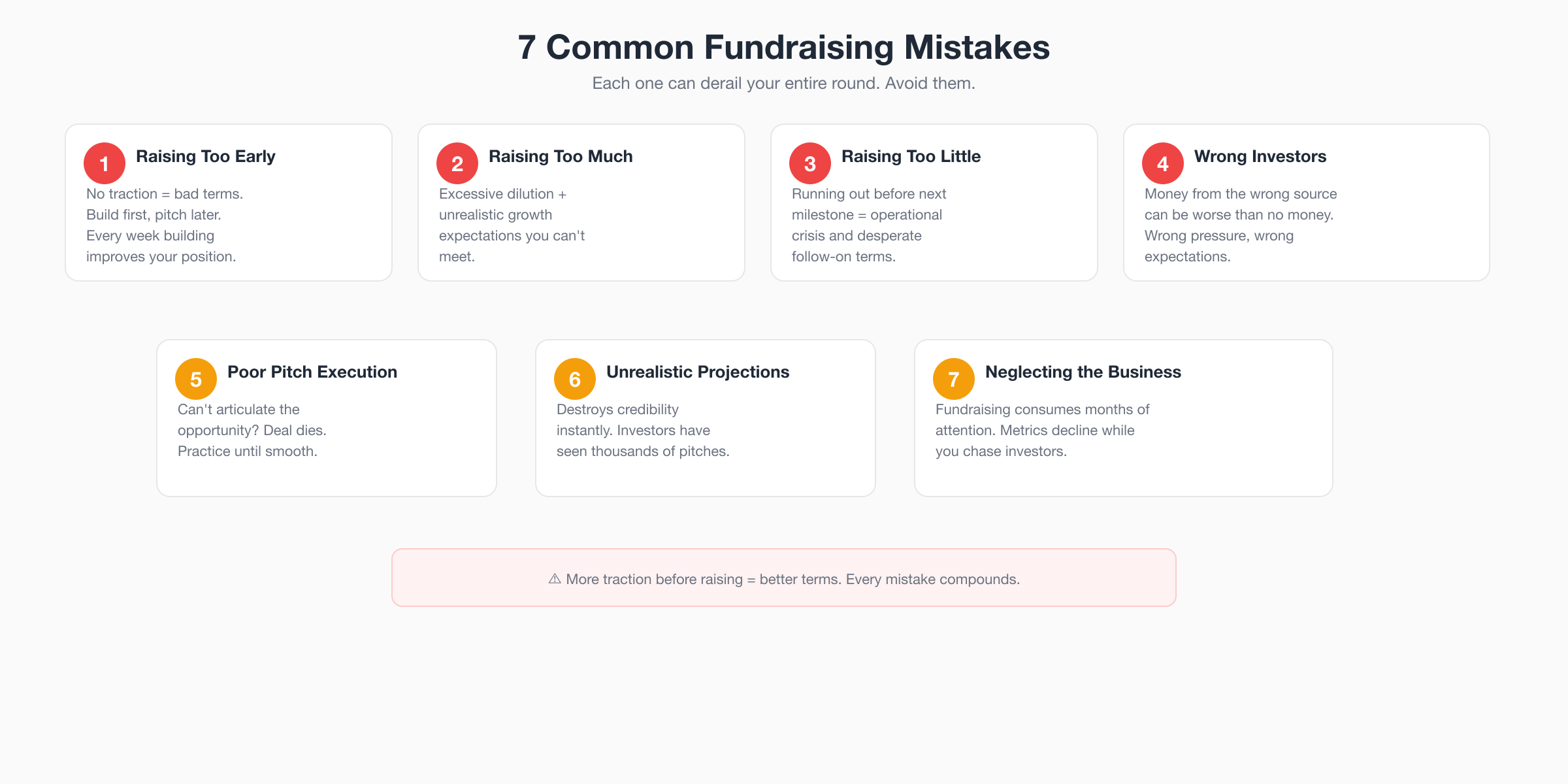

Common Fundraising Mistakes

I’ve watched clients and colleagues make these mistakes, and some are devastating.

Raising too early, before having anything to show, is the most common. More traction means better terms. Every week you build before raising improves your negotiating position.

Raising too much creates excessive dilution and unrealistic growth expectations. And raising too little means running out before reaching the next milestone, which creates operational crisis.

Choosing wrong investors who don’t understand your business or add the wrong kind of pressure is surprisingly common. Money from the wrong source can be worse than no money at all.

Poor pitch execution, where you can’t clearly articulate your opportunity, kills deals. Practice until your pitch is smooth and compelling.

Unrealistic projections destroy credibility instantly. Investors have seen thousands of pitches. They know when numbers don’t make sense.

Overvaluing valuation at the expense of terms is a mistake I’ve seen hurt founders badly. A high valuation with aggressive liquidation preferences can mean the founder gets nothing in most exit scenarios.

And neglecting the actual business while fundraising is the cruel irony. The fundraising process consumes months of full-time attention, but the business still needs to operate and grow. Some of my clients have watched metrics decline during fundraising because all their attention shifted to investor meetings.

After You Raise

Raising capital changes the business fundamentally. You now have investor relations, regular updates, board meetings, and accountability to outside stakeholders.

Capital should fuel growth, and investors expect deployment. There’s spending pressure that didn’t exist before. This can be healthy (investing in hiring and growth) or unhealthy (spending to hit milestones rather than building sustainably).

Growth pressure is real. Investors expect returns, and this creates urgency that can drive great execution or terrible decisions depending on how you manage it.

You’re no longer the sole decision-maker. Board oversight, reporting requirements, and approval rights change how decisions get made. This is a significant psychological shift for founders who started as solo operators.

And each round sets up the next. The milestones you hit between rounds determine your negotiating position for future fundraising. The pressure never really stops until you exit or become self-sustaining.

Alternatives to Traditional Equity

The startup funding landscape continues to evolve with new models worth considering.

Revenue-based financing, where capital is repaid as a percentage of revenue, is less dilutive than equity. It’s gaining popularity for businesses with predictable revenue streams.

Grants from government and foundations provide non-dilutive funding. They’re competitive but worth investigating, especially for specific sectors like clean tech, healthcare, or education.

Strategic investment from industry players often includes partnerships alongside capital. This can be powerful when the strategic fit is genuine.

Consulting revenue that funds product development is one of my favorite approaches. You sell your expertise as services while building your product on the side. The services generate revenue and market intelligence simultaneously.

And customer prepayment, where customers pay in advance for future delivery, validates demand while providing capital. If customers won’t prepay, you might not have the product-market fit you think you do.

Making the Decision

Should you raise capital? Honestly assess whether you can achieve your goals without external funding. Understand the real cost in equity, control, stress, and distraction. It’s not free money, and the strings attached are significant. Raising capital is a tool, not a goal. Use it only when it genuinely serves your business objectives.

Evaluate alternatives like bootstrapping, slower growth, or a different business model entirely. Consider whether you’re comfortable with investor expectations and board oversight for years to come.

And think long-term. What does success look like for you personally? Does fundraising serve that vision? Some founders want to build empires. Others want to build sustainable businesses that support good lives. Neither goal is wrong, but they lead to very different funding decisions.

The right decision depends entirely on your specific situation, your ambitions, and your honest definition of success.

Frequently Asked Questions

What’s the difference between angel investors and venture capital?

Angel investors are wealthy individuals investing their personal funds, typically $25,000-$500,000 at early stages. Venture capitalists manage professional investment funds, investing $1 million to $50+ million at various stages. Angels often provide more mentorship; VCs bring more structure and expectations. Different firms focus on different stages and industries.

How long does it take to raise startup capital?

The fundraising process typically takes 3-6 months from first meetings to closing, sometimes longer. This includes targeting investors, multiple meetings, due diligence, term sheet negotiation, and closing documentation. Warm introductions speed the process—cold outreach rarely works.

What should be in a pitch deck?

Key elements include: problem statement, your solution, market opportunity, business model, traction to date, competitive landscape, team credentials, financial projections, and specific fundraising ask. Keep it to 10-15 slides. The goal is generating interest for deeper conversations, not answering every question.

How do startup valuations work?

Pre-money valuation is company value before investment; post-money is pre-money plus investment amount. Early-stage valuation is largely negotiated based on team, market, traction, and comparable deals. Valuation determines what equity percentage investors receive. Don’t optimize only for valuation—investor quality and terms often matter more.

Do I need to raise venture capital?

Many businesses don’t need external capital and can bootstrap through personal savings and early revenue. VC is appropriate for capital-intensive businesses requiring rapid scaling with potential for very large outcomes. Consider the cost in equity, control, and expectations. Raising capital is a tool, not a goal—use it only when it genuinely serves your business objectives.