Autonomous Technology: How Driverless Cars Will Reshape These Industries in 2026

Driverless cars stopped being science fiction sometime in the last two years, and most people missed the moment. In 2026 you can open an app in San Francisco, Phoenix, Los Angeles, Austin, Atlanta, Miami, Dallas, Houston, or Orlando and a car with no one in the driver’s seat pulls up to take you across town. Waymo alone now gives more than 500,000 paid driverless rides every week across 10 US cities, a tenfold jump in under two years. The technology arrived quietly, city by city, while the headlines argued about whether it ever would.

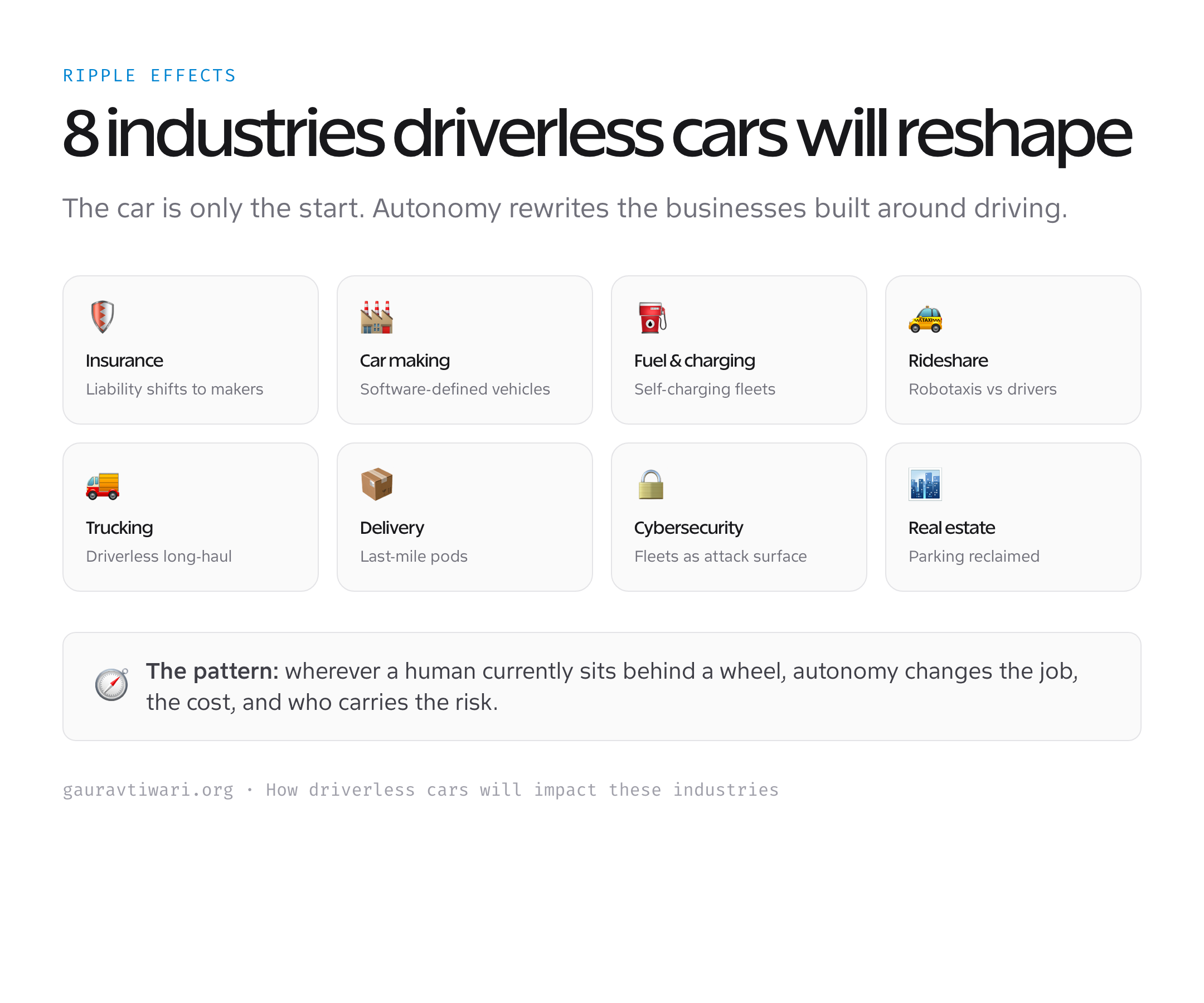

The reason this matters goes far beyond the novelty of a steering wheel turning itself. Autonomous technology doesn’t just change how we get around. It quietly rewires entire industries built on the assumption that a human sits behind every wheel. Insurance, car manufacturing, fuel and charging, rideshare, trucking, delivery, even real estate and cybersecurity all shift when the driver disappears.

I’ve watched this space for years, and the gap between the hype and the reality is the most interesting part. So this guide does two things: it tells you where driverless cars actually are in 2026, not where a keynote promised they’d be, and then it walks through the industries this technology will reshape, with the second-order effects most people haven’t thought about. If you’re weighing a career, an investment, or just trying to understand the road ahead, this is the map.

Where this comes from: I’ve tracked autonomous technology as a working developer and analyst for years, riding driverless cars firsthand and reading the regulatory filings most coverage skips. Every claim below is pinned to a Level (SAE J3016), a city, or a dated fact, not a keynote promise, and I flag the limits as plainly as the wins.

What changed in 2026: Waymo crossed 500,000 paid robotaxi rides a week across 10 US cities and is targeting one million weekly rides plus 20+ new metros, including its first overseas launch in London (Automotive World; TechCrunch, March 2026). Tesla pulled the safety monitor from some Austin robotaxis on January 22, 2026 and went metro-wide unsupervised in June, though its active fleet is still only about 20 cars (CNBC; Teslarati, 2026). On the rules, the US House introduced the SELF DRIVE Act of 2026 (H.R. 7390) and NHTSA advanced its national AV framework to replace the state-by-state patchwork (NHTSA; act-news, 2026).

Where driverless cars actually are in 2026

The honest answer: further than skeptics admit, and less far than the boldest promises. Waymo, Alphabet’s self-driving arm, is the clear leader, running fully driverless robotaxis in 10 US cities and targeting more than 20 new metros plus its first overseas market, London, by the end of 2026. These cars carry no safety driver at all in their service areas, and they now log over 500,000 paid rides a week. That’s genuine Level 4 autonomy operating commercially, today, at scale.

Tesla is the loudest name but, by the numbers, the underdog in robotaxis. Its Austin pilot pulled the safety monitor from some cars in January 2026 and went metro-wide unsupervised that June, but the active driverless fleet is still only around 20 vehicles, a tiny fraction of Waymo’s, and most Tesla vehicles on the road operate at Level 2, meaning a human is legally responsible at all times. Tesla’s bet is that camera-only software will scale faster and cheaper than Waymo’s sensor-heavy approach. That bet hasn’t paid off yet, but it’s far from settled.

Elsewhere, the picture is just as telling. China’s Baidu runs large Apollo Go robotaxi fleets in cities like Wuhan, Amazon’s Zoox is rolling out purpose-built vehicles with no steering wheel at all, and a wave of companies including Aurora and Kodiak are pushing driverless trucks on Texas highways. Meanwhile, GM shut down its Cruise robotaxi business in late 2024 after a high-profile safety incident, a reminder that this race has casualties. The takeaway: driverless cars are real and growing fast, but unevenly, and the leaderboard isn’t who you’d guess from the headlines.

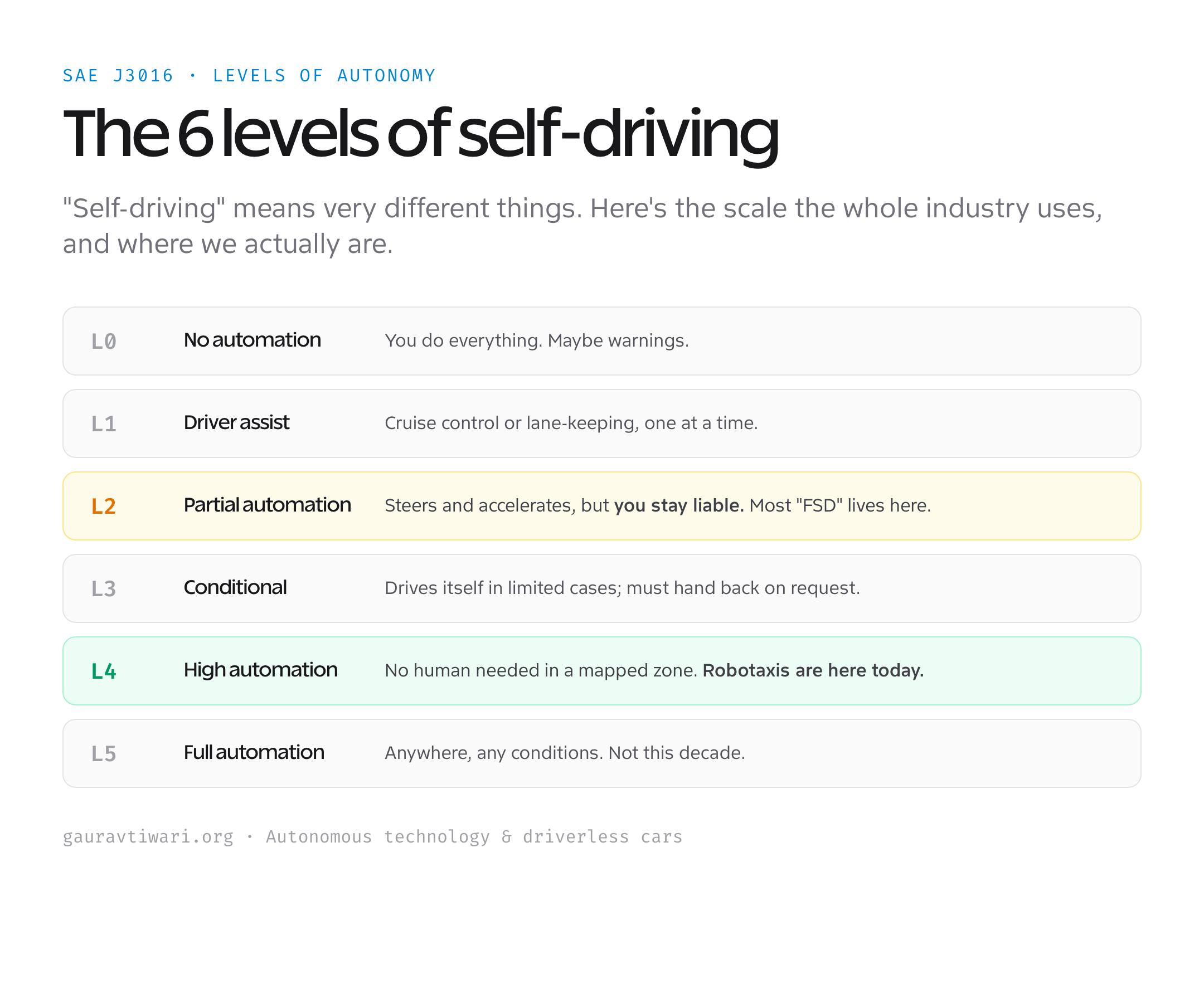

The SAE levels of autonomy, explained

Before we get to the industries, you need one piece of vocabulary, because “self-driving” is used to mean wildly different things. The industry standard is the SAE J3016 scale, six levels from 0 to 5. Knowing where a car sits on it tells you the single most important thing: who is legally responsible when something goes wrong.

The crucial line runs between Level 2 and Level 4. At Level 2, the car steers and accelerates, but you are driving and you are liable, this is where most “Full Self-Driving” and “Autopilot” systems actually sit, despite the names. At Level 4, the vehicle drives itself with no human needed inside a mapped, geofenced area, and the operator carries the liability. That single shift in responsibility is what makes Level 4 a genuine revolution and Level 2 a convenience feature. Level 5, a car that drives anywhere in any conditions, probably isn’t arriving this decade.

The intelligence behind all of this is machine learning, the same family of techniques reshaping every other industry. If you want the foundation, my primer on machine learning and deep learning explains how these systems actually learn to see and decide. And because nearly every robotaxi is electric, the autonomous shift is tangled up with the EV transition I covered in are electric cars the future of driving.

Automobile insurance

Auto insurance is a massive industry built on a simple premise: humans crash, and you pay to cover that risk. Take the human out and the whole model wobbles. The optimistic case is obvious, since most accidents are caused by human error, safer autonomous cars should mean fewer claims and lower premiums. But it’s not that simple, and the second-order effects are where it gets interesting.

The biggest shift is who pays. When a Level 4 car crashes itself, the fault isn’t the “driver”, it’s the manufacturer or the software operator. That moves liability from millions of individual policies toward a handful of corporate product-liability claims. Personal premiums may fall, but the cars themselves get expensive to insure, a fender that’s a $300 fix on an old sedan can be a $3,000 repair when it’s packed with lidar, radar, and cameras. Insurers are already rethinking commercial-versus-personal coverage, a distinction I broke down in commercial vs private car insurance, and usage-based pricing will only accelerate.

For the millions of people who work as actuaries, claims adjusters, and agents, the work doesn’t vanish, but it changes shape. Expect more demand for people who can model software risk and cyber exposure, and less for those who price routine human-driver policies. The industry won’t disappear. It’ll be unrecognizable.

Automobile manufacturing

Carmakers face the most existential change of all, because the car stops being a mechanical product and becomes a computer on wheels. The value of a vehicle is migrating from the engine and chassis to the software stack, the sensors, and the AI that drives it. That’s why the industry now talks about “software-defined vehicles”, and why traditional OEMs are scrambling to compete with tech companies on a field that favors code over horsepower.

It reshapes the factory too. Quality control for an autonomous car isn’t just checking torque specs and panel gaps, it’s validating millions of lines of safety-critical code and the behavior of a neural network in edge cases no test track can fully cover. The skill mix on the line and in engineering shifts hard toward software, sensors, and systems integration. Henry Ford cut assembly time from twelve hours to ninety minutes with the moving line; the next leap is measured in software updates pushed overnight, not minutes saved on a chassis.

There’s also a business-model twist. If robotaxi fleets, not individuals, buy most cars, manufacturers sell fewer units to consumers and more to fleet operators, or run the fleets themselves and sell rides. That changes everything from dealerships to financing to how cars are designed in the first place.

Gas, charging, and service stations

This is a quietly huge one. The corner gas station survives on more than fuel, it sells coffee, snacks, and convenience to people who have to stop anyway. Now picture an autonomous electric fleet that charges itself at a depot overnight and never pulls into a forecourt. The impulse-buy economy that funds those stations takes a real hit.

Because almost every autonomous vehicle is electric, the autonomy shift and the charging shift arrive together. Expect dedicated fleet charging depots, robotic charging arms, and battery-swap experiments aimed at keeping robotaxis earning instead of sitting plugged in. Traditional service stations will have to reinvent as charging-plus-experience destinations or fade, the same pivot Europe started years ago and the US is now racing to catch up on.

Maintenance changes too. Electric drivetrains have far fewer moving parts than combustion engines, so the oil-change-and-muffler economy shrinks, while demand grows for technicians who can service sensors, calibrate cameras, and diagnose software faults. The grease monkey becomes a diagnostics specialist.

Taxis, rideshare, and public transport

This is the industry feeling it first, and hardest. Uber and Lyft built empires on human drivers using their own cars. Robotaxis remove the single biggest cost in that equation, the driver, which is exactly why both companies have pivoted from competing with autonomy to partnering with it, listing Waymo and others inside their apps. The math is brutal: a fleet that never sleeps, never takes a cut, and never calls in sick is hard to beat on price.

The human cost is real and immediate. Millions of people drive taxis, rideshares, and delivery vehicles for a living, and “wait and see” is not a comfortable place to stand. The transition won’t be overnight, robotaxis are still geofenced to specific cities and conditions, but the direction is set. Public transport faces a subtler version: autonomous shuttles and buses could extend coverage and cut operating costs, yet they raise hard questions about jobs, access, and who controls the network.

My honest read: rideshare driving as a stable income disappears in major cities within this decade, while edge cases, bad weather, rural routes, and complex pickups, keep humans in the loop longer than the optimists claim. If you drive for a living, the smart move is to start building skills the robots can’t yet touch.

Trucking and logistics

If you want to see where autonomy makes money first, look at trucking, not taxis. Highway driving is the easiest problem in autonomy, long, predictable stretches with no pedestrians or traffic lights, and the economics are enormous. Companies like Aurora and Kodiak have begun running driverless trucks on Texas interstates, hauling freight on the simplest, most lucrative legs while humans handle the messy first and last miles.

The promise is freight that moves around the clock without mandated rest breaks, cutting costs and easing a chronic driver shortage. The threat is to one of the most common jobs in many regions. Most likely is a hybrid model for years: autonomous trucks handle the highway middle, human drivers handle depots and cities, and the job shifts from long-haul solitude to local, technical work. I dug into the broader shift in how AI is transforming transportation and logistics, and trucking is the clearest near-term proof of it.

Delivery services

Last-mile delivery is being attacked from two directions at once: small autonomous sidewalk and road pods from companies like Nuro, and aerial drones from operators including Amazon and Wing. Both target the most expensive part of the supply chain, the final stretch to your door, where labor costs are highest and routes are densest.

For now, traditional carriers, USPS, UPS, FedEx, still move the bulk of parcels, and they will for years. But in dense urban zones, expect autonomous pods to handle a growing slice of local deliveries, especially food and small packages, while human couriers concentrate on complex or rural drops. International and cross-country freight stays human-led far longer. The realistic future isn’t robots replacing every delivery driver, it’s a layered system where autonomy takes the predictable volume and people take the rest.

Cybersecurity

Here’s the risk that grows in lockstep with the benefits. A driverless car is a networked computer that can move at 70 mph, which makes it a target unlike any laptop. A compromised vehicle isn’t just a data breach, it’s a physical-safety threat. Scale that to a fleet of thousands sharing the same software, and a single vulnerability becomes a fleet-wide emergency.

The attack surface is broad: the car’s onboard systems, the over-the-air update pipeline, the fleet’s cloud backend, and the vehicle-to-everything communication links. Theft takes on a new meaning when a car could, in theory, be remotely started and driven away. This is why automotive cybersecurity is one of the fastest-growing specialties in the field, and why the principles in my guide to proven cybersecurity practices apply to vehicles as much as to servers. Expect regulation, mandatory security standards, and a hiring boom for people who can secure machines that carry passengers.

Real estate and urban planning

This is the impact almost no one anticipates, and it might be the biggest of all. Cities devote staggering amounts of land to parking, by some estimates a third of the land in dense urban cores. Autonomous fleets don’t need to park near their passengers; they drop you off and move on to the next ride or retreat to a depot. Reclaim that land and you change the shape of the city itself.

Garages convert to housing and retail, curbs shift from parking to pickup zones, and homes no longer need two-car driveways. Commute tolerance changes too, if you can work or sleep during the ride, living farther out costs you less, which ripples into housing prices and suburban sprawl. Urban planners are already sketching post-parking cities. It won’t happen fast, but autonomy quietly hands back some of the most valuable real estate we own.

Jobs and the workforce

Cutting across every industry above is the question everyone actually worries about: jobs. Driving is one of the most common occupations on earth, and autonomy will reshape it. But “robots take all the jobs” is too lazy a story. What really happens is a shift, work moves from operating vehicles to building, maintaining, securing, and overseeing the systems that operate them.

The growth is in machine-learning engineering, sensor and robotics work, fleet operations, remote vehicle monitoring, cybersecurity, and the technical service roles that keep autonomous fleets running. The decline is in pure driving jobs, slowly at first, then faster as geofences widen. If you’re planning a career, this is the time to skill toward the technology, not away from it, a theme I explore in the future of work and digital transformation. The people who thrive won’t be the ones who resist autonomy, but the ones who learn to build and run it.

The roadblocks: why full autonomy is taking longer than promised

For all the progress, anyone who tells you fully autonomous cars are everywhere next year is selling something. The remaining problems are genuinely hard, and they’re why Level 5 stays over the horizon.

- Edge cases. The last 1% of driving, a child chasing a ball, an ambiguous hand signal from a traffic cop, a flooded road, is where autonomy still struggles. And that 1% is where lives are at stake.

- Weather. Heavy rain, snow, and fog degrade the sensors these cars rely on. Most robotaxis are still limited to favorable conditions and well-mapped areas.

- Regulation and liability. Laws vary by state and country, and the question of who’s at fault in a crash is still being written. The US House introduced the SELF DRIVE Act of 2026 and NHTSA is advancing a national framework to replace the state-by-state patchwork, but it isn’t settled law yet.

- Public trust. One viral incident can set adoption back years. People forgive human error far more readily than machine error, fairly or not.

- Cost. The sensors and computing aren’t cheap yet. Economics work for fleets in dense cities long before they work for the car in your driveway.

None of these is a dead end. All of them are reasons the rollout is happening city by city and use-case by use-case, rather than all at once. Progress is real, but it’s incremental, and that’s exactly why the industry impacts above will unfold over a decade, not a year.

What this means for you

Strip away the hype and a few practical takeaways remain. If you’re choosing a career, the opportunity is in the technology stack, machine learning, robotics, sensors, fleet operations, and automotive cybersecurity, not in roles that autonomy is set to absorb. These are well-paid, durable fields, and demand is climbing fast.

If you’re a consumer, you’ll likely ride in a robotaxi before you own a self-driving car, and that’s fine, the economics favor fleets first. If you’re an investor or business owner, watch the second-order plays: the insurers, chargers, chip makers, mapping firms, and security companies that profit no matter which carmaker wins. And if you simply want to keep up, treat autonomy as one thread in a broader shift I track in my latest technology trends roundup. The driverless future isn’t coming. In a handful of cities, it’s already here, and it’s spreading outward one street at a time.

Frequently asked questions

Are driverless cars actually available in 2026?

Yes, but only in specific cities. Waymo runs fully driverless robotaxis with no safety driver across 10 US metros including San Francisco, Phoenix, Los Angeles, Austin, Atlanta, Miami, Dallas, and Houston, now logs over 500,000 paid rides a week, and aims for 20-plus new cities by the end of 2026. These are genuine Level 4 vehicles operating commercially. You cannot yet buy a personally owned car that drives itself anywhere with no human, that is Level 5, and it is still years away.

Is Tesla Full Self-Driving truly autonomous?

Not in the legal sense. Most Tesla vehicles with Full Self-Driving operate at SAE Level 2, which means the system assists but the human driver must stay alert and remains legally responsible at all times. Tesla is piloting a small Level 4-style robotaxi service in Austin, but its authorized fleet is far smaller than Waymo’s, and the names Autopilot and Full Self-Driving describe ambition more than current legal capability.

Which industries will driverless cars affect the most?

The biggest near-term impacts hit auto insurance, car manufacturing, fuel and charging, rideshare and taxis, trucking and logistics, and delivery. Less obvious but large effects reach cybersecurity, real estate and urban planning, and the broader job market. Trucking and rideshare feel the changes first because the economics favor removing the driver from predictable, high-cost routes.

Will driverless cars take away jobs?

They will reshape jobs more than simply erase them. Pure driving roles in taxis, rideshare, and long-haul trucking will decline over time, slowly at first and faster as autonomous zones expand. At the same time, demand grows for machine-learning engineers, robotics and sensor specialists, fleet operators, remote vehicle monitors, and automotive cybersecurity experts. The smart move is to build skills around the technology rather than competing with it.

Are autonomous vehicles safe?

In their tested operating areas, leading robotaxis have strong safety records, and the core promise, removing human error that causes most crashes, is real. But they still struggle with edge cases, severe weather, and unmapped roads, which is why they stay geofenced. They also introduce new risks like cybersecurity threats. Safe within limits is the accurate description, and those limits are widening carefully rather than all at once.

When will I be able to buy a fully self-driving car?

A personally owned car that drives itself anywhere in any conditions, true Level 5, is probably more than a decade away, and some experts doubt it arrives at all in the form often promised. What you will see sooner is more capable Level 2 and Level 3 features in new cars, and far wider access to Level 4 robotaxi services you summon rather than own. For most people, riding in autonomy will come well before owning it.

The bottom line

Driverless cars are no longer a question of “if”. They’re already carrying millions of passengers in a handful of cities, and the only real questions are how fast they spread and how gracefully the industries around them adapt. Insurance, manufacturing, fuel, rideshare, trucking, delivery, cybersecurity, and even real estate are all being rewritten by a single change: the human stepping out of the driver’s seat.

The transition will be uneven, slower than the hype and faster than the skeptics, unfolding street by street and use-case by use-case. But the direction is set. Whether you’re planning a career, running a business, or just curious about the road ahead, the time to understand autonomous technology is now, while it’s still arriving, and not after it has already remade the world around you.