Short-Term Loans: 7 Benefits, 5 Risks, and How to Decide in 2026

Running a business with irregular cash flow is exhausting. One month you’re flush, the next you’re staring at invoices you can’t pay because three clients are 30 days late. I’ve been there. And the first time I seriously looked at short-term loans, I almost got burned by an offer that looked reasonable on the surface but carried a 94% APR buried in the fine print.

Short-term loans are useful tools. But like most financial tools, the outcome depends almost entirely on whether you understand them before you sign. This article breaks down exactly what these loans do, who they’re actually right for, and where the real risks live, including the ones lenders don’t put on the homepage.

I’m not a financial advisor, and this isn’t financial advice. But I’ve run businesses for 16+ years, managed cash flow across multiple income streams, and spent way more time than I’d like studying how debt products actually work. What follows is what I wish I’d known earlier.

What Are Short-Term Loans?

A short-term loan is any loan with a repayment period under 24 months, though most fall in the 3 to 18 month range. You borrow a fixed amount, pay it back in scheduled installments (weekly or monthly), and the loan closes. That’s the whole mechanic.

The category is broader than most people realize. Short-term loans include personal installment loans, business cash advance products, payday loans (at the worst end), invoice financing, merchant cash advances, and some lines of credit. Not all of these are equally useful or equally dangerous.

Typical loan amounts range from $100 to $10,000 for personal borrowers, and up to $100,000+ for business products. Repayment terms usually run 3 to 18 months. APRs swing wildly, from around 20% at the responsible end to 1,500%+ for payday loans. That range is the whole story.

The lenders worth paying attention to are regulated ones. In the US, state laws vary significantly regarding interest rate caps and lending practices. The Consumer Financial Protection Bureau (CFPB) provides oversight at the federal level. Always check your state regulator first before signing anything.

7 Benefits of Short-Term Loans

Short-term loans get a bad reputation because payday lending gets lumped in with the whole category. But responsible, regulated short-term borrowing has real advantages, especially for people who need speed over size.

1. Fast Approval and Funding

Traditional bank loans take 2 to 6 weeks to process. Short-term lenders typically decide within hours, sometimes minutes, and fund within 24 to 48 hours. For a business facing a cash shortfall on a Tuesday, that speed isn’t a luxury, it’s the whole point.

Online lenders like Quidmarket run automated affordability checks that flag decisions fast. They’re FCA-regulated, which means the speed doesn’t come at the cost of basic consumer protections. That matters more than most people check for.

2. Flexible Use of Funds

Most short-term personal loans are unsecured and unrestricted. You can use the money for a car repair, a medical bill, a business supply order, or covering payroll during a slow month. Lenders don’t require you to justify the specific use the way a mortgage or business grant would.

That flexibility is genuinely valuable. A $1,500 loan to cover three invoices while waiting on client payments is a legitimate use case. So is a $500 loan to fix the laptop you need to keep working. The loan serves a real function.

3. Lower Total Interest vs. Long-Term Loans

This one surprises people. Short-term loans often carry higher APRs, but because the repayment window is short, the total interest paid can be less than a long-term loan at a lower rate. A $1,000 loan at 50% APR repaid in 6 months might cost $130 in total interest. The same $1,000 on a 5-year personal loan at 8% APR could cost you $215 over its lifetime.

The APR comparison is misleading when terms differ. Always look at the total repayment figure, not just the rate. That’s the number that actually leaves your bank account.

4. Credit Building Potential

For someone rebuilding their credit history, a small short-term loan repaid on time adds positive payment history to their file. Credit bureaus like Experian, Equifax, and TransUnion all factor payment consistency into credit scoring models. Six months of on-time repayments on a $500 loan is more useful than six months of doing nothing.

This only works if the lender reports to credit bureaus. Most regulated lenders do. Always confirm before borrowing if credit building is part of your goal.

5. Less Documentation Than Traditional Lending

A bank loan or SBA loan requires tax returns, business financials, 2+ years of income history, and often collateral. Short-term lenders typically need proof of income, a bank account, and ID. The bar is lower by design, because these products target people who fall outside traditional credit criteria.

Freelancers, sole traders, and gig workers who can’t produce W-2s or standard payslips can often still qualify. That fills a real gap in the credit market that banks won’t touch.

6. No Collateral Required

Most short-term personal loans are unsecured. You’re not putting your car, home, or equipment on the line. If things go wrong, it’s a collections and credit-score problem, not a repossession problem. That’s a meaningful distinction for anyone who’d otherwise be risking assets they depend on.

7. Bridges Specific Cash Flow Gaps

I’ve used short-term financing twice in business contexts. Once to cover a supplier payment while waiting on a large retainer to clear. Once to fund a software license I needed before a project kicked off. Both times, the loan paid for itself within the period it was active because I could take the work I otherwise would have turned down.

Bridging is the highest-value use case. The loan exists to close a time gap between money owed and money received, not to fund consumption you can’t afford.

Before borrowing, calculate the exact total repayment amount, not the monthly payment. Lenders display monthly figures because they look manageable. The total is what tells you whether the loan actually makes financial sense for your situation.

5 Risks of Short-Term Loans

Every benefit above comes with a counterpart risk. Ignore these and you’ll end up worse off than before you borrowed.

1. High APRs That Stack Fast

Short-term loans for people with poor credit regularly carry APRs of 100% to 400%. Payday loans hit 1,500% or more when expressed as annualized rates. Even FCA-regulated payday loans in the UK are capped at 0.8% per day, which works out to 292% APR annualized. That’s the best-case regulated scenario.

If you miss a payment, late fees compound on top of that. What starts as a $300 loan can spiral into $600+ in debt inside a few months if you’re not disciplined. I’ve seen this happen to people who thought they had a handle on it.

2. Debt Cycle Risk

The most dangerous pattern with short-term loans is rolling them over. You borrow $500, can’t fully repay at the end of the term, so you take out another $500 to cover the first one. Then another. Within three cycles you’ve paid $400+ in fees and still owe the original principal. This is how people end up trapped.

UK regulators cap rollovers at two for payday products specifically because of this pattern. But not all lenders follow the spirit of that rule, and international borrowers have far fewer protections. If you’re borrowing to repay a loan, stop. That’s the signal that something structurally wrong is happening with your finances.

3. Predatory Lending Practices

Not every lender marketing a “short-term loan” is operating legally or ethically. Red flags include lenders that guarantee approval without any credit or income check, lenders based in unregulated jurisdictions, upfront fee requests before any funds are disbursed, and contracts that bury the true APR in footnotes using non-standard rate calculations.

In the US, check your state regulator and the CFPB database. In the UK, check the FCA Register at register.fca.org.uk before handing over any personal information. If a lender isn’t registered, don’t borrow from them, regardless of how good the offer looks.

4. Cash Flow Pressure During Repayment

A short repayment window means large relative payments. A $1,000 loan repaid over 6 months is roughly $185 per month including interest. If your income is irregular, that fixed obligation can create its own cash flow problem. You borrowed to fix a cash flow gap and now you’ve created a new, recurring one.

Before you borrow, map out 6 months of projected income and expenses. If the repayment takes more than 20-25% of your average monthly income, the term is probably too short or the amount too large for your situation.

5. Hidden Fees

Origination fees (charged upfront as a percentage of the loan), early repayment fees (yes, some lenders penalize you for paying off early), NSF fees when a payment bounces, and insurance add-ons that inflate the effective cost. These are the profit levers that make some short-term loans far more expensive than their advertised APR suggests.

Read the full loan agreement before signing. Specifically look for: origination fee percentage, any prepayment penalty, late payment fee amount, and whether automatic payment is required (which can cause issues if your account has a different balance than expected).

If a lender asks for an upfront fee before releasing your funds, that’s a scam. Legitimate lenders deduct any fees from the loan amount or add them to the repayment schedule. They never ask for payment before you’ve received the loan.

Short-Term Loans vs Other Borrowing Options

Before committing to a short-term loan, you should know what else is on the table. Here’s a direct comparison across the six most common options people consider when they need money fast.

| Feature | Short-Term Loan | Personal Loan | Credit Card | Payday Loan | Credit Union Loan | 401k Loan |

|---|---|---|---|---|---|---|

| Typical APR | 20%-400% | 6%-36% | 18%-30% | 292%-1,500%+ | 6%-18% | Prime rate +1% |

| Funding speed | 24-48 hours | 2-7 days | Instant (if approved) | Same day | 1-5 days | 5-10 business days |

| Loan amounts | $100-$10,000 | $1,000-$50,000 | Up to credit limit | $100-$1,500 | $500-$25,000 | Up to 50% of balance |

| Repayment term | 3-18 months | 1-7 years | Revolving | 2-4 weeks | 6-60 months | 5 years |

| Credit check | Soft or hard | Hard | Hard | Minimal or none | Hard | None |

| Collateral required | Usually no | Usually no | No | No | Sometimes | Your retirement savings |

| Debt cycle risk | Medium | Low | High (revolving) | Very high | Low | Medium |

| Best for | Cash flow gaps, 3-12 months | Large planned expenses | Everyday spending | Last resort only | Lower rates if eligible | No other options |

The takeaway: credit union loans are almost always cheaper if you’re eligible. Personal loans beat short-term loans on rate for larger amounts. Short-term loans win only on speed and accessibility when other options aren’t available or practical.

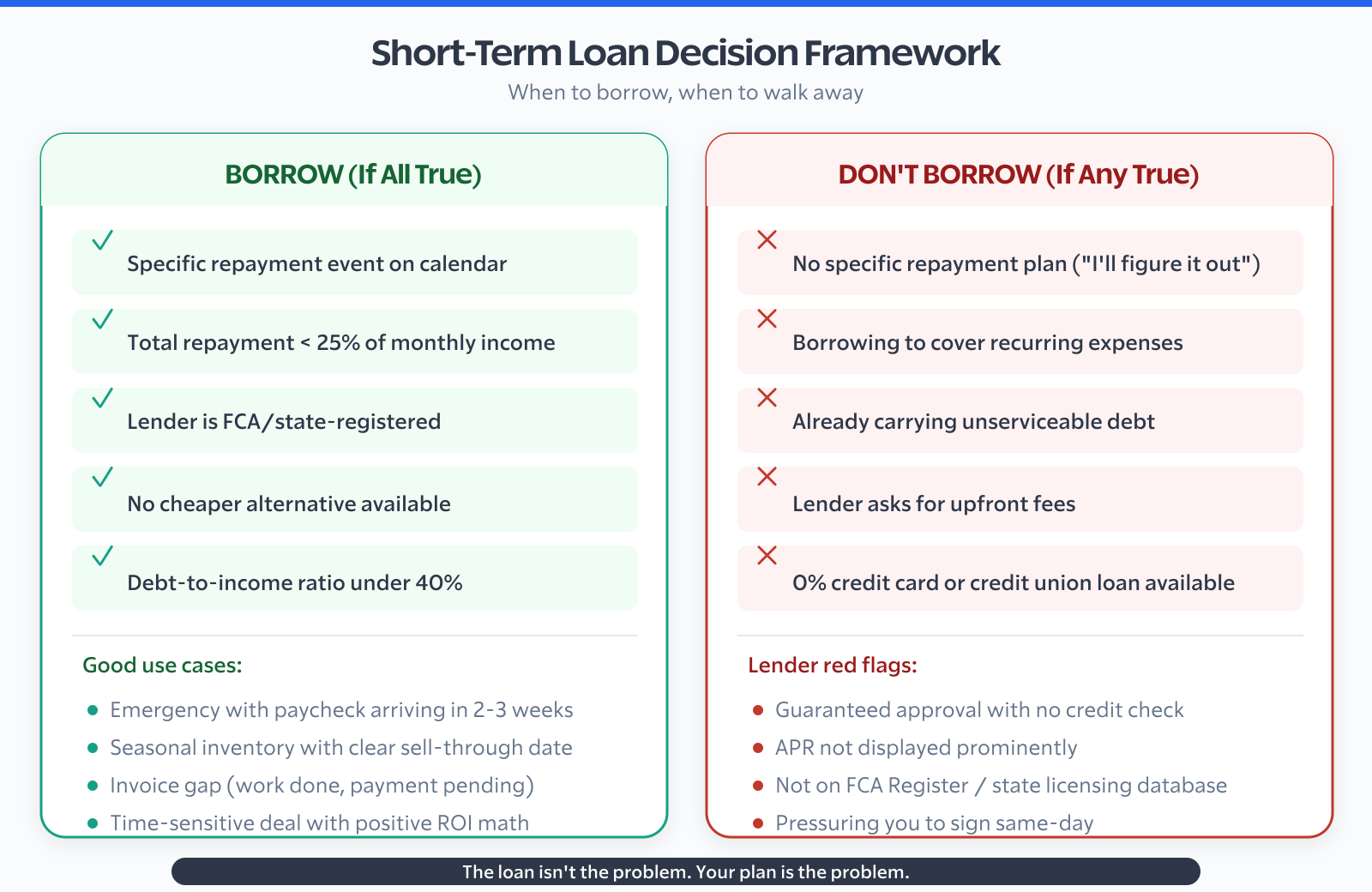

When Short-Term Loans Actually Make Sense

There are specific situations where a short-term loan is the right call. Not every situation. Specific ones.

Emergency expenses with a clear repayment path. Your boiler breaks in January, you have no emergency fund, and you have a paycheck arriving in three weeks that covers the repair cost. A short-term loan bridges that three-week gap. That’s a legitimate use case because you have a defined repayment source.

Seasonal businesses with predictable income peaks. A Christmas gift retailer needing to stock inventory in October, who will clear that stock by December 31, has a clear repayment event on the horizon. The loan finances inventory that generates the cash to repay it. This is textbook short-term business financing.

Invoice gaps for freelancers and contractors. You’ve done the work. The invoice is approved. The client pays in 45 days. You need to pay your own bills in 15. Invoice financing or a short-term bridge loan against that invoice is a reasonable option, assuming the loan cost is less than the value of not defaulting on your own obligations.

Time-sensitive opportunities with positive ROI. A supplier is offering a 20% discount on a bulk order, but only for the next 72 hours. You can fund the order with a short-term loan at a total cost of 8%. The math works. You take the loan, take the discount, net 12%. That’s a use case where borrowing actually generates money.

If you want to think through how to decide wisely before borrowing, my deeper guide on how to choose short-term loans wisely covers the full evaluation framework I use.

When to Avoid Short-Term Loans

Short-term loans are not the answer in most situations where people reach for them. Here’s where they go wrong.

You’re already carrying debt you can’t service. Adding a new loan to an existing debt pile that’s already straining your cash flow doesn’t fix the underlying problem. It delays it while making it more expensive. If your current debt-to-income ratio is above 40%, a short-term loan is the wrong tool.

You have no concrete repayment plan. “I’ll figure it out” isn’t a repayment plan. “I’ll use my salary on the 25th” is. If you can’t point to a specific income event that covers the repayment, don’t borrow.

You’re funding ongoing consumption. Rent every month. Groceries. Subscriptions. A short-term loan for recurring expenses is a structure that will collapse. You’re borrowing $500 this month to pay rent because you don’t have enough income. Next month you’ll need to repay the $500 plus interest AND cover rent again. The math only gets worse.

Better alternatives are available. A 0% credit card offer, a family loan, a salary advance from your employer, or a credit union loan at 8% APR are all better options than a 200% APR short-term loan. Check these first. Actually check them, don’t just assume you won’t qualify.

Building financial freedom is largely about not borrowing your way into holes you can’t climb out of. The discipline of asking “do I actually need this loan or do I need better cash flow planning” is worth developing early.

How to Choose a Legitimate Short-Term Lender

Assuming you’ve decided a short-term loan is the right move, here’s how to pick a lender you can trust.

Check regulatory status first. In the US, check your state’s Department of Financial Institutions or the CFPB (Consumer Financial Protection Bureau) database. In the UK, use the FCA Register (register.fca.org.uk). This is the single most important step. If a lender isn’t licensed to operate in your jurisdiction, every other detail is irrelevant.

Look for representative APR, not just monthly rate. Responsible lenders display their representative APR prominently. If a lender shows you a daily or weekly rate but obscures the annualized figure, that’s a yellow flag. You want to see: total loan amount, total amount repayable, representative APR, and payment schedule, all before you commit.

Check how they handle affordability assessment. Legitimate lenders run an affordability check to confirm you can repay. They ask about income, expenses, and existing credit commitments. Any lender that skips this entirely is either irresponsible or fishing for people who are likely to default and pay late fees. Neither is good for you.

Read the late payment policy. Specifically: what’s the late fee, what happens at 30 days past due, and when do they report to credit bureaus? This tells you the real cost of uncertainty in your repayment plan.

Check reviews, but filter carefully. Trustpilot reviews are useful for pattern recognition. A lender with 2,000 reviews averaging 4.1 stars with consistent comments about transparency is different from one with 200 reviews averaging 4.8 with generic phrasing. Read the negative reviews, not the positive ones. The negative ones tell you how lenders behave when things go wrong.

From a broader financial health perspective, I’d point you toward my piece on passive wealth strategies if you’re thinking about how to reduce your dependence on borrowed capital long-term. Short-term loans are a tool, but they shouldn’t be a permanent fixture of your financial life.

Short-Term Loans and Your Overall Financial Strategy

One thing I don’t see written about enough: how short-term loans fit, or don’t fit, into a deliberate financial strategy. Most coverage treats them as isolated transactions. They’re not.

Every loan you take creates a liability that competes with other financial goals. Repaying a short-term loan at 80% APR means money that could go toward an emergency fund, an investment, or paying down cheaper debt is going to interest instead. That opportunity cost is real, even if it doesn’t show up on a balance sheet.

I diversify my income across several streams specifically to reduce the situations where I’d need a loan. When one channel slows, others compensate. That’s not luck, it’s structure. If you’re building toward income resilience, the approach I cover in my blog income diversification guide applies beyond blogging to any independent income model.

The goal isn’t to never need credit. It’s to need it rarely, use it deliberately, and exit it fast. Short-term loans, used correctly, fit that model. Used as a recurring crutch, they become a drag on everything else you’re trying to build.

One adjacent conversation worth having: don’t chase high-return “investments” to pay off debt faster. The crypto space is full of promises that attract people who are financially stretched and looking for a shortcut. My breakdown of common crypto myths debunked is worth reading before you make any decisions in that direction.

Frequently Asked Questions

What is the typical repayment period for a short-term loan?

Most short-term loans carry repayment terms between 3 and 18 months. Payday loans are the exception, with 2 to 4 week terms. Some short-term business loans extend to 24 months. The shorter the term, the higher the monthly payment, so match the term length to what your cash flow can actually sustain.

Do short-term loans hurt your credit score?

Applying for a short-term loan usually triggers a hard credit inquiry, which can drop your score by 5 to 10 points temporarily. If you repay on time, the positive payment history offsets this over 6 to 12 months. If you miss payments, the negative marks stay on your credit file for up to 7 years. The net effect depends entirely on repayment behavior.

Can I get a short-term loan with bad credit?

Yes, many short-term lenders specifically serve borrowers with poor or thin credit histories. The tradeoff is a higher APR, since the lender prices in the default risk. A 580 credit score might qualify you for a loan at 150% APR where a 720 score would get you 35%. If you have bad credit, compare multiple lenders and use an eligibility checker that runs a soft pull before applying formally.

What’s the difference between a short-term loan and a payday loan?

A payday loan is a type of short-term loan, but with specific characteristics: very short repayment window (typically your next payday, so 2 to 4 weeks), very small amounts (usually under $1,500), and extremely high APRs (292% to 1,500%+). Installment-based short-term loans spread repayment across 3 to 18 months and generally carry lower APRs. Payday loans are the most dangerous variant in the short-term loan category.

How much can I borrow with a short-term loan?

For personal short-term loans, most lenders offer between $100 and $10,000. Some online lenders cap at $5,000. The amount you qualify for depends on your income, credit score, and existing debt obligations. Business short-term loans can reach $100,000 or more, particularly for invoice financing and merchant cash advances where the loan is secured against future revenue.

Can I repay a short-term loan early?

Usually yes, and many jurisdictions protect your right to settle loans early. However, some lenders charge an early repayment fee (ERF), typically 1 to 2 months of interest. Read your loan agreement before repaying early to calculate whether the fee wipes out the interest savings. Most regulated lenders don’t charge ERFs, but always check.

What happens if I can’t repay a short-term loan?

If you miss a payment, the lender will typically charge a late fee, attempt the payment again, and then contact you. At 30 to 60 days past due, many lenders report to credit bureaus. At 90+ days, the account may go to collections. Contact your lender before you miss a payment, not after. Most will work with you on a payment arrangement if you’re proactive.

The Bottom Line

Short-term loans aren’t inherently good or bad. They’re fast, accessible, and flexible, and those same properties make them dangerous when used without a clear repayment plan. The lender isn’t your problem. Your problem is your plan.

If you’ve got a defined cash flow gap, a specific repayment event on the horizon, and you’ve checked that better alternatives aren’t available, a regulated short-term loan from a licensed lender is a reasonable tool. Use it, repay it fast, and move on.

If you’re borrowing because your expenses exceed your income on a recurring basis, no loan fixes that. The math gets worse, not better. The harder work, building income that outlasts any single gap, is what actually changes the picture over time.