Medical Debt and Reverse Mortgages: What Actually Works (and What Doesn’t)

A $47,000 hospital bill hits differently when you’re 68 years old and on a fixed income. I’ve seen this up close. A family friend had a three-week cardiac procedure in 2022. Good Medicare coverage. Still walked out with $47,000 in out-of-pocket costs after coinsurance, gaps, and specialist fees Medicare doesn’t cover. The hospital’s payment plan was $800/month. Social Security was $1,640/month. The math didn’t work.

One option kept coming up in the financial forums she was browsing: a reverse mortgage credit line. The suggestions ranged from “it’s a lifesaver” to “it’s a predatory scam.” Nobody gave her a straight answer about what it actually does, when it makes sense, and when it’s a trap. So I spent a few weeks reading through HECM documentation, HUD counselor guides, and real case studies to write the article I wish existed.

The Scale of Medical Debt in America

Medical debt is the number one cause of personal bankruptcy in the United States. About 100 million Americans carry some form of it, according to KFF Health System Tracker data from 2022. The median amount? Around $2,500. But for people over 60 who’ve had a serious procedure, five-figure bills are common. The average hospital stay now costs $15,734 per day. A cardiac catheterization averages $28,200. A hip replacement runs $35,000 to $50,000 depending on complications.

Medicare covers a lot, but not everything. Part A covers hospital stays after a $1,600 deductible (2023 rate). Part B covers 80% of outpatient services after a $226 annual deductible, which means you’re on the hook for 20% of every specialist visit, imaging scan, and therapy session. No cap. That 20% with no ceiling is what creates the $40,000-plus bills that wreck retirement budgets.

Social Security’s average monthly benefit in 2024 sits at $1,907. Most retirees don’t have substantial savings. The Federal Reserve’s 2022 Survey of Consumer Finances found that the median retirement savings for households age 65-74 is $200,000. That sounds okay until you realize healthcare costs for a couple retiring at 65 are estimated at $315,000 over their lifetime, according to Fidelity. The gap is real, and it’s why medical debt becomes a housing and retirement security issue.

What Is a Reverse Mortgage Credit Line?

A reverse mortgage lets homeowners 62 and older borrow against their home equity without selling the home or making monthly payments. The most common type is the Home Equity Conversion Mortgage (HECM), which is insured by the Federal Housing Administration (FHA) and regulated by HUD.

The credit line option is one of three ways to receive funds (the others being a lump sum or monthly payments). With a credit line, you draw what you need when you need it, like a home equity line of credit. But there’s a critical difference: the unused portion of a reverse mortgage credit line grows over time at the same interest rate the loan is accruing. That’s not a typo. If you open a $150,000 credit line and don’t touch it for five years, the available balance grows, potentially to $180,000 or more, even though you haven’t paid anything in.

How much you can borrow depends on three things: your age (older = more), your home’s appraised value, and current interest rates (lower rates = more). For 2024, the HECM lending limit is $1,149,825. You won’t borrow the full value of your home; the principal limit factor tables set the actual percentage, typically 40-60% of home value for borrowers in their mid-60s to mid-70s. On a $400,000 home, that’s a credit line of roughly $160,000 to $240,000.

You must live in the home as your primary residence. You must keep paying property taxes, homeowner’s insurance, and basic maintenance. Fail any of those, and the loan becomes due immediately. That’s not a small detail. It’s the clause that trips people up.

How a Reverse Mortgage Credit Line Can Help with Medical Debt

For someone sitting on $300,000 in home equity with a $47,000 medical bill and $1,900/month in Social Security income, the math case for a reverse mortgage credit line is straightforward. Draw $47,000 from the credit line, pay off the hospital, and owe nothing monthly. The loan balance grows over time, but there’s no immediate cash flow hit.

That’s the core appeal. You’re converting illiquid equity (your house, which you can’t spend) into liquid cash (funds you can use now) without a monthly payment obligation. For someone whose budget has no room for an $800/month hospital payment plan, this creates breathing room that literally doesn’t exist with other options.

The growing credit line feature is legitimately useful if you use it strategically. Open the line early, before a medical crisis, and let the available balance grow. A $200,000 credit line opened at 63 at a 6% interest rate could grow to roughly $268,000 by the time you’re 68 and actually need it, based on the compound growth formula on unused credit lines. That’s meaningful. Most financial advisors who recommend reverse mortgages at all recommend this approach: open it as a contingency fund, not as a first resort.

Open a reverse mortgage credit line before you need it. The unused portion grows at the loan’s interest rate, so a $180,000 credit line opened at 65 could be worth $230,000+ by 70. This is the strategy Wade Pfau, Ph.D. (a retirement income researcher at The American College of Financial Services) has written about extensively: use it as a standby fund, not a debt-clearing emergency button. You can find lenders who specialize in HECM products at reverse.mortgage.

Reverse Mortgage vs. Other Ways to Handle Medical Debt

Before committing to any strategy, compare it against the alternatives. Every option has a different cost structure, eligibility requirement, and risk profile.

| Option | Monthly Payment | Eligibility | Interest Rate (2024) | Impact on Home | Best For |

|---|---|---|---|---|---|

| Reverse Mortgage Credit Line | $0 (deferred) | 62+, home equity, primary residence | 6.5-8.5% (variable) | Reduces equity over time | Homeowners 62+ with significant equity, no heirs dependent on estate |

| HELOC | Interest-only during draw, then P+I | Good credit, income to qualify | 8.5-10% (variable) | Lien on home; missed payments = foreclosure | Homeowners with stable income who can make payments |

| Personal Loan | $400-$900/month on $30K loan | Credit score 640+, income proof | 11-24% | None (unsecured) | Smaller debts under $20K with good credit |

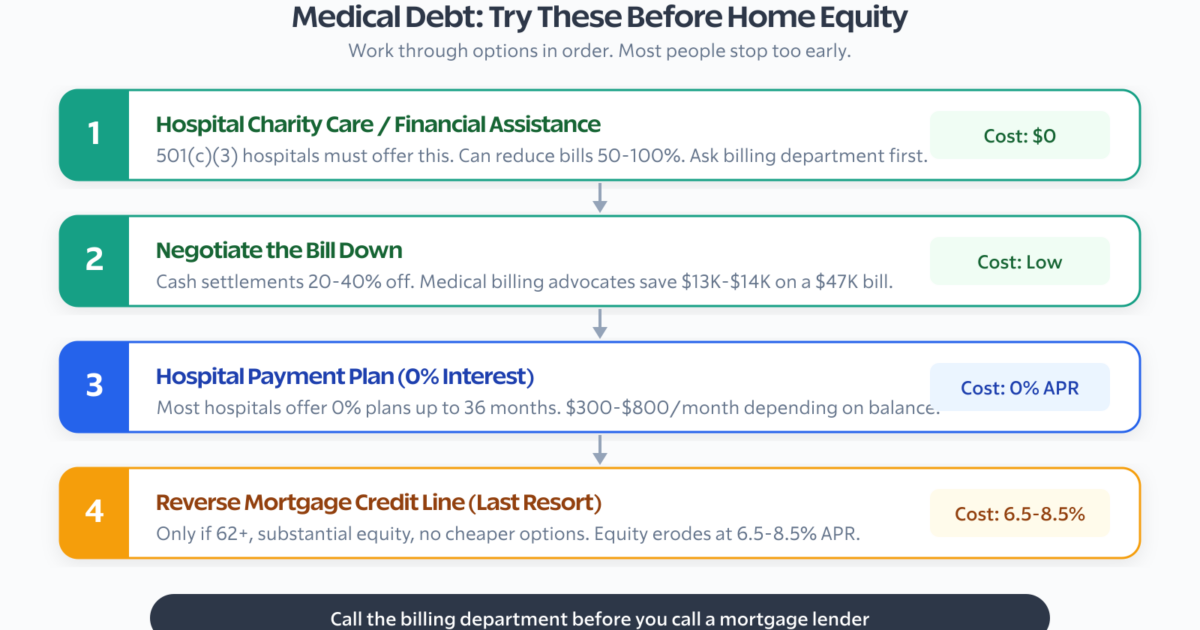

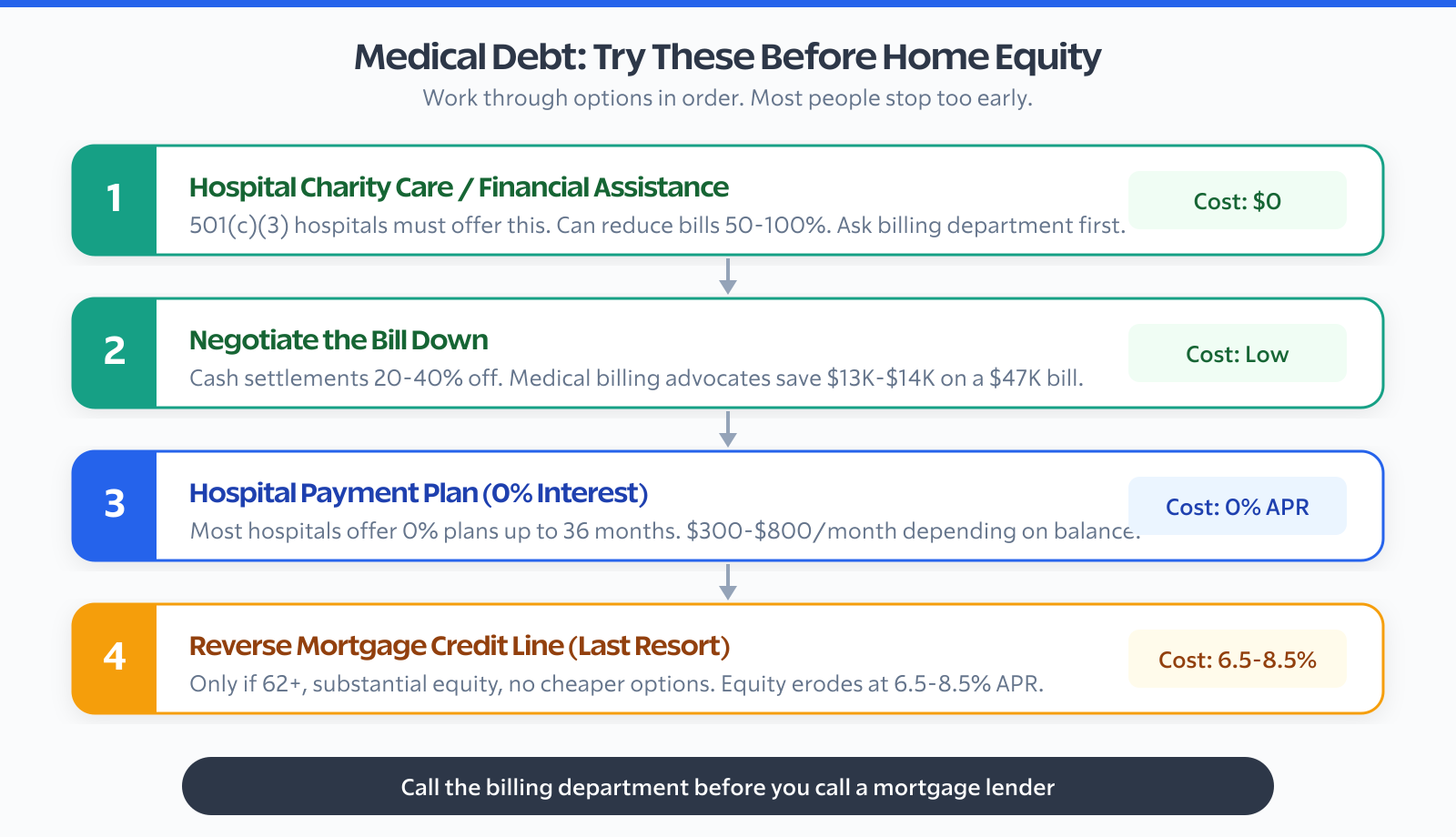

| Hospital Payment Plan | Negotiated ($100-$800+) | Anyone with a hospital bill | 0% (most plans) or up to 5% | None | Bills under $20K where monthly payment fits budget |

| Medical Credit Card (CareCredit) | Minimum payment varies | Credit approval required | 0% promo, then 26.99% deferred | None, but deferred interest is brutal | Short-term bridge if paid in full by promo end |

| Bankruptcy (Chapter 7) | $0 post-discharge | Income below state median | N/A | Home may be protected under state exemption | Debt truly unpayable, credit damage acceptable |

A few things stand out in that comparison. Hospital payment plans at 0% interest are almost always worth trying first, before touching home equity. Hospitals negotiate. A $47,000 bill can often be reduced by 20-40% for cash payment, and many hospitals have charity care programs that wipe out debt entirely for households under 250-400% of the federal poverty level. Call the billing department before you do anything else.

Personal loans at 20%+ APR on a $40,000 medical bill will cost you $8,000-$10,000 per year in interest. That’s not a solution. That’s a different crisis. Medical credit cards with deferred interest are worse if you miss the promotional period, because the full interest from day one gets added back, often at 26.99%. Read the fine print before you touch those.

The Real Risks of Using a Reverse Mortgage for Medical Bills

I want to be direct about this section, because most reverse mortgage content online is written by lenders who want to sell you one. The risks are real and they’re worth understanding before you sign anything.

Equity erosion compounds quickly. You’re not just borrowing the principal. You’re borrowing at 6.5-8.5% annually, with interest accruing on interest. A $150,000 reverse mortgage balance at 7% becomes roughly $295,000 in 10 years and $581,000 in 20 years. If your home appreciates at 3-4% annually, your equity still shrinks. At some point, the loan balance can exceed the home’s value. FHA insurance covers the difference so you don’t owe more than the home is worth, but your heirs inherit nothing in that scenario.

The homeowner obligations clause is serious. You must maintain the home, pay property taxes, and pay homeowner’s insurance continuously. Skip a property tax payment, and the lender can call the loan due. I’ve read cases where people in their 80s, dealing with cognitive decline, missed a tax payment and faced foreclosure on a home they’d owned for 40 years. This isn’t a hypothetical risk.

The upfront costs are high. Origination fees can run up to $6,000. Mortgage insurance premiums start at 2% of the appraised value (that’s $8,000 on a $400,000 home) plus 0.5% annually on the outstanding balance. Closing costs add another $2,000-$5,000. Total upfront costs on a $400,000 home can easily hit $15,000-$18,000. That’s money that comes directly off your available equity from day one.

It complicates Medicaid eligibility. If you ever need Medicaid to cover long-term care, reverse mortgage proceeds sitting in your bank account as assets could disqualify you. Medicaid has asset limits (typically $2,000 for individuals). You’d need to spend down those funds before qualifying. This is a situation where talking to an elder law attorney before taking any money out is not optional.

Your heirs inherit the obligation. When you die or permanently move out, heirs have 30 days to decide what to do (extendable to 12 months while they sell). They can pay off the loan and keep the house, sell the house and keep the difference, or walk away. If the loan balance exceeds the home’s value, they walk away with nothing. For families where the home is the primary inheritance, this conversation needs to happen before you sign.

Never use a reverse mortgage as your first move against medical debt. Call the hospital billing department first and ask about charity care, financial hardship programs, and negotiated cash settlements. Many hospitals are required by IRS 501(c)(3) status to offer charity care. A $47,000 bill can sometimes be reduced to $12,000-$15,000 for households with low income. Only after exhausting those options does it make sense to consider home equity strategies.

When a Reverse Mortgage Actually Makes Sense for Medical Debt

This isn’t a product everyone should avoid. There are specific situations where a reverse mortgage credit line is genuinely the right move for managing medical costs.

You’re 70+ with substantial equity and no heirs depending on the home. If you’re 72, own your home free and clear (or close to it), have $400,000+ in equity, and your children are financially established and not counting on the inheritance, the risk profile changes. You have significant room to borrow without exhausting equity, and the monthly-payment-free structure genuinely improves your cash flow without forcing you to sell or move.

Medical costs are ongoing, not a one-time bill. Chronic conditions, cancer treatment, dialysis, or long-term medication costs can run $2,000-$5,000 per month indefinitely. A hospital payment plan doesn’t help with ongoing costs. A reverse mortgage credit line that you draw from monthly acts like a supplement to Social Security for healthcare spending.

You’ve already negotiated the bill down and still can’t pay. If the hospital’s already at their lowest price, you’ve applied for charity care and didn’t qualify, and the remaining balance is $20,000-$60,000 that you genuinely cannot pay from income or savings, the reverse mortgage credit line becomes a real option. At least the interest rate (6.5-8.5%) is lower than a personal loan (11-24%).

You’re using it as a planned retirement income supplement. The most financially sound use of a reverse mortgage credit line isn’t to pay off existing debt in a crisis. It’s to open the line at 63-65, let it grow, and use it strategically alongside other retirement income. Think of it as a fourth leg of retirement income: Social Security, pension or 401(k), savings, and home equity credit line. This approach is what achieving real financial freedom in retirement looks like for homeowners.

When to Skip It Entirely

There are clear scenarios where a reverse mortgage is the wrong answer, even if the math technically allows it.

You plan to move within 5-7 years. The upfront costs alone ($15,000-$18,000 on a $400,000 home) make a reverse mortgage a terrible deal for short-term borrowing. If there’s any chance you’ll downsize, move to assisted living, or relocate in the next several years, the costs won’t amortize. A personal loan is cheaper for a 3-year horizon despite the higher interest rate.

You have a younger spouse or a non-borrowing spouse under 62. If one spouse is 68 and the other is 58, the younger spouse isn’t on the HECM. If the older borrower dies first, the non-borrowing spouse can stay in the home under HUD rules established in 2015, but they can’t draw additional funds. This severely limits the usefulness of the credit line for couples with age gaps. Talk to an elder law attorney and a HUD-approved counselor before proceeding.

The medical debt is actually payable with other options. If the hospital will take $300/month at 0% interest and your budget can handle $300/month, that’s a better deal than a loan accruing 7% annually. Don’t reach for home equity when a payment plan fits.

You have significant retirement accounts you haven’t tapped. If you have a $200,000 IRA and $40,000 in medical debt, withdrawing from the IRA (even with taxes and penalties) likely costs less than a reverse mortgage’s compounding interest over 10-15 years. Run the numbers with an accountant before deciding.

You’re considering it without telling your family. This is a red flag. If you’re keeping the reverse mortgage from adult children because you know they’d object, that’s a sign you haven’t fully worked through the estate implications. The conversation is uncomfortable, but skipping it creates bigger problems later. Independent financial planning is part of any good passive wealth strategy, but this decision affects more than just you.

Step-by-Step: Applying for a Reverse Mortgage Credit Line

If you’ve weighed the options and a HECM credit line is the right move, here’s the actual process. It’s not fast. Budget 60-90 days from start to funding.

Step 1: Get HUD counseling first. This is federally required, not optional. You must complete a session with a HUD-approved HECM counselor before a lender can take your application. Counseling costs $125-$200 (sometimes waived for low-income borrowers). The counselor will go through alternatives, risks, costs, and your specific situation. Treat this as a genuine financial planning session, not a box to check. Call 1-800-569-4287 to find a HUD-approved counselor.

Step 2: Choose a lender. Shop at least three lenders. HECM interest rates and origination fees vary. The margin (the lender’s markup above the index rate) can differ by 0.5-1.0% between lenders, which adds up over decades. Get loan comparisons in writing before committing.

Step 3: Complete the application and financial assessment. Since 2015, lenders run a financial assessment on HECM applicants. They verify income, credit history, and ability to maintain ongoing obligations (taxes, insurance, maintenance). A poor history of paying property taxes can get your application denied or require a Life Expectancy Set-Aside (LESA), which reserves a portion of your available funds specifically for future tax and insurance payments, reducing what you can actually use.

Step 4: Home appraisal. An FHA-approved appraiser values the home. The appraised value determines your maximum loan amount. If your home needs significant repairs, the lender may require them before closing or set aside funds for repairs.

Step 5: Underwriting and closing. The underwriter reviews everything: appraisal, financial assessment, title, insurance. Closing includes signing all documents in front of a notary. You then have a 3-day right of rescission, meaning you can cancel without penalty within 3 business days of closing. Use this window to review everything carefully.

Step 6: Draw funds as needed. With the credit line option, funds aren’t automatically disbursed. You request draws as needed. Keep the unused balance as large as possible for as long as possible to benefit from the credit line growth feature.

The entire process is one part of a broader set of tools for investment diversity in retirement. Home equity via a reverse mortgage can work alongside other income streams, but it works best when it’s planned, not reactive.

What to Do Before You Touch Home Equity

Before any home equity conversation, exhaust these options in order. Most people don’t, because they don’t know they exist.

Hospital charity care and financial assistance programs. Nonprofit hospitals are required by the IRS to have these programs. Eligibility typically goes up to 250-400% of the federal poverty level ($36,450-$58,320 for a single person in 2024). Call the billing department, ask specifically for “financial assistance” or “charity care,” and request the application. This can reduce bills by 50-100%.

Medical billing advocates. These professionals negotiate on your behalf, typically for 25-35% of the amount saved. On a $47,000 bill, if they get it to $28,000, you pay them about $5,000-$6,750 and save $13,000-$14,000 net. Worth the call.

State pharmaceutical assistance programs. If ongoing medication costs are driving the debt, programs like PACE in Pennsylvania, EPIC in New York, and SHIPP in other states provide significant prescription cost relief for seniors. These aren’t well-advertised.

Medicare Savings Programs. Four programs help low-income Medicare beneficiaries cover Part B premiums, deductibles, and coinsurance. The Qualified Medicare Beneficiary (QMB) program can eliminate all Medicare cost-sharing if income is at or below 100% of the federal poverty level. Many eligible people aren’t enrolled because they don’t know it exists.

If you’re looking at the broader picture of managing expenses and building resilience across multiple income streams, the approach I’ve written about in blog income diversification applies here too: don’t rely on one source, whether income or debt strategy.

Frequently Asked Questions

Can I use a reverse mortgage to pay off existing medical debt?

Yes, you can use reverse mortgage funds for any purpose, including paying off medical bills. There’s no restriction on how the money is used once distributed. But the question isn’t whether you can; it’s whether it’s the smartest move. Before drawing from a reverse mortgage credit line, exhaust hospital charity care programs, negotiate a payment plan, and check your eligibility for Medicare Savings Programs.

Does a reverse mortgage affect Medicaid eligibility?

It can. Reverse mortgage proceeds are not income (they’re loan funds), so they don’t count as income for Medicaid purposes. But if those funds sit in your bank account at the end of the month, they count as assets. Medicaid asset limits are typically $2,000 for individuals. If you draw $47,000 and don’t spend it in the same month, you’d likely be disqualified from Medicaid until you spend down below the asset limit. Talk to an elder law attorney before using a reverse mortgage if Medicaid is a possibility in your future.

What happens to the reverse mortgage when I die or move to a nursing home?

The loan becomes due when you permanently leave the home, whether from death, moving to a nursing home, or any other reason. You can be in a hospital or rehab facility for up to 12 months before the loan comes due. After death, heirs have 30 days to notify the lender and up to 12 months to sell or refinance. If the loan balance exceeds the home’s value, FHA insurance covers the difference and heirs owe nothing beyond the home itself.

Can I lose my home with a reverse mortgage?

Yes. The most common trigger is failing to pay property taxes or homeowner’s insurance. About 18% of HECM loans ended in default between 2009 and 2017, and the majority were tax and insurance failures. A Life Expectancy Set-Aside (LESA) can be built into the loan to automatically cover these costs, but it reduces the amount available to you.

Is reverse mortgage interest tax deductible?

Not while you’re living in the home. Reverse mortgage interest accrues but isn’t deductible until it’s actually paid, which typically happens at the end of the loan (when the home is sold or heirs pay it off). At that point, it may be deductible as home mortgage interest, but the rules are complex. Get a CPA involved before counting on a tax deduction from reverse mortgage interest.

What’s the minimum age for a reverse mortgage?

62 for a federally insured HECM. Some proprietary reverse mortgage products have lowered their minimum to 55, but these aren’t regulated the same way and typically carry higher costs. If you’re between 55 and 62, consider waiting until 62 for the HECM. The older you are when you open the loan, the higher your principal limit factor, meaning you can borrow a larger percentage of your home’s value.

The Bottom Line on Medical Debt and Reverse Mortgages

A reverse mortgage credit line isn’t a predatory scam. It’s also not a magic fix. It’s a specific financial tool that works well for a specific profile: homeowners 68+, with substantial equity, no income to qualify for conventional loans, ongoing or large medical costs, and no near-term plans to move. Outside that profile, the costs and risks usually outweigh the benefits.

The family friend I mentioned at the start? She ended up not needing the reverse mortgage. The hospital had a charity care program she didn’t know about. Her bill dropped to $11,200. She put $400/month toward it on a 28-month hospital payment plan at 0% interest. Her home equity stayed intact.

That’s not always how it works out. But it happens more often than people think, because most people never ask. Call the billing department before you call a mortgage lender. The best financial tool is the one that costs the least and preserves the most options. Start there.

If you’re thinking about this as part of a larger retirement income plan, the framework I use for reducing financial anxiety applies here too: clarity on what you actually owe, what options actually exist, and what the real cost of each option is over time. That clarity is what lets you make a decision you won’t regret in five years.