10 Best Stripe Alternatives in 2026 for Entrepreneurs and Small Businesses

Stripe is the default payment processor for most online businesses in 2026, and for good reason. It works, the developer experience is excellent, and the documentation is the best in the industry. The problem is that Stripe’s defaults aren’t always the cheapest, safest, or most convenient option, depending on your business model. If you’re running a subscription SaaS out of the US, Stripe is probably fine. If you’re a freelancer getting paid from clients in 6 countries, a brick-and-mortar retailer, a high-volume merchant paying $4,000 a month in Stripe fees, or a SaaS founder tired of handling your own global sales tax, there’s almost certainly a better fit for you.

I’ve used or integrated most of the payment processors on this list across client projects over the past decade. Below are the 10 I’d actually recommend as Stripe alternatives in 2026, with real fee breakdowns, honest comparisons, and clear recommendations on who should use which. I’ve also added a later section with 15 more processors worth knowing, because the merchant-of-record and regional-processor categories have exploded in the last two years. A whole new generation of tools (Polar.sh, Dodo Payments, Creem.io, Paddle, LemonSqueezy) has emerged specifically to serve indie developers and SaaS founders tired of dealing with Stripe plus tax compliance plus Chargebee plus their own legal entity. By the end of this article you’ll have seen 25+ real Stripe alternatives with current pricing and honest use-case recommendations.

Skip to:

Stripe alternatives at a glance

Before the deep dives, here’s the one-table summary of how the 10 main alternatives compare on price, best use case, and key differentiator. All fees are the standard advertised rates as of April 2026 and can vary based on country, volume, and negotiated pricing.

| Processor | Standard fee | Monthly fee | Best for | Category |

|---|---|---|---|---|

| Stripe (benchmark) | 2.9% + 30¢ | $0 | SaaS, online stores | Payment processor |

| Wise | ~0.5-1% transfer fee | $0 | Freelancers, international invoicing | Money transfer |

| Payoneer | 3% card, 1% eCheck | $0 | Marketplaces (Upwork, Amazon), cross-border | Cross-border payout |

| PayPal | 3.49% + 49¢ | $0 | Consumer trust, invoicing, global reach | Payment processor |

| Square | 2.6% + 10¢ (in-person) | $0 | Brick-and-mortar retail, service businesses | POS + processor |

| Stax | Interchange + small markup | $99+ | High-volume merchants ($15K+/mo) | Subscription pricing |

| WePay (Chase) | 2.9% + 30¢ | $0 | SaaS platforms, marketplaces | Platform processor |

| Adyen | Interchange + $0.12 | $120 min | Enterprise, omnichannel | Enterprise processor |

| Authorize.Net | 2.9% + 30¢ | $25 | Traditional merchants needing gateway control | Payment gateway |

| 2Checkout (Verifone) | 3.5% + 35¢ | $0 | Global sellers needing 200+ country support | Merchant of record |

| ChargeBee | No processing fee | Free → $599+ | Subscription billing on top of Stripe/Braintree | Billing platform |

What Stripe actually charges (so you have something to compare against)

Most “Stripe alternatives” articles skip the step of telling you what Stripe charges in the first place. Here’s the current US pricing so the comparisons below have real context. Other regions are similar but not identical.

- Online card payments (US): 2.9% + $0.30 per successful charge. This is the number most comparisons anchor on.

- In-person card payments (US): 2.7% + $0.05 via Stripe Terminal.

- International card surcharge: +1.5% if the customer’s card is issued outside your account country.

- Currency conversion: +1% if Stripe needs to convert the charge to your payout currency.

- ACH Direct Debit: 0.8% capped at $5 per transaction. Cheap for large invoices.

- Stripe Billing (subscriptions): +0.5% on top of base processing, or +0.8% for advanced recurring logic.

- Stripe Tax: 0.5% of each transaction for automated sales tax handling in supported regions.

- Disputes/chargebacks: $15 per dispute (refunded if you win).

- Instant payouts: 1% of the payout amount (minimum $0.50).

- Monthly fee: $0. No minimums, no setup fees, pay as you go.

Put another way: a US SaaS that processes $50,000/month in recurring card payments through Stripe Billing with standard Stripe Tax is paying roughly 2.9% + 0.5% + 0.5% = 3.9% plus the fixed per-transaction fees. On $50K that’s around $1,950/month. At $500K/month you’re paying ~$19,500/month just in Stripe fees. That’s the number you have to beat for an alternative to actually save you money.

Why You Should Consider Alternatives to Stripe

Stripe is popular for a reason: clean developer tooling, solid documentation, and a huge ecosystem of integrations. But there are four recurring reasons I’ve seen clients leave or never adopt Stripe, and at least one of them probably applies to your business.

1. Stripe’s ecosystem is more complex than it looks

Stripe is one layer in your payment stack. If you run a real business on it, you’re usually also paying for Stripe Billing for subscriptions, Stripe Tax for sales tax compliance, Stripe Radar for fraud, Stripe Terminal for in-person, and integrating a separate accounting tool for bookkeeping. Each of those adds either a percentage, a monthly fee, or both. The “free to start” pitch is accurate for a landing page with a single product, but the real total cost of a production Stripe setup scales faster than most founders expect. It’s also missing native PayPal support, which still matters for a non-trivial slice of consumer purchases even in 2026.

2. Account freezes and reserve holds can break growth

The single biggest reason businesses leave Stripe is also the one that hits hardest: Stripe’s risk-management engine can freeze your account, hold a rolling reserve on your payouts, or ban your business entirely without much warning and with very limited recourse. This happens disproportionately to businesses that look unusual to automated risk models: coaching, adult content, supplements, anything with a high chargeback rate, anything that suddenly 10xs its volume in a week. If your revenue depends on cash flow (and whose doesn’t?), an unexpected 90-day reserve can sink you. Alternatives like Adyen, Authorize.Net plus a direct merchant account, Braintree (PayPal-owned, but a different risk engine), and Stax are often more forgiving here, especially for higher-risk or non-standard categories.

3. Sales tax and VAT compliance is your problem, not Stripe’s

Stripe collects the money. You (or Stripe Tax, at 0.5%) figure out how much sales tax, VAT, or GST to charge each customer, then you file returns in every jurisdiction where you have a nexus. For a US-only store selling physical goods, that’s manageable. For a global SaaS selling digital products, it’s a nightmare: VAT MOSS in the EU, digital services tax in the UK, GST in Australia, GST in India, state-by-state sales tax in the US. The alternative is a merchant of record (MoR) setup like Paddle, LemonSqueezy, 2Checkout, or Gumroad. The MoR becomes the legal seller on every invoice, collects and remits every tax worldwide, and sends you a clean payout minus their fee. If your business sells digital products globally, switching to a MoR isn’t about price. It’s about never thinking about tax again.

4. Stripe’s regional support has real gaps

Stripe supports many countries but not all, and in the ones it does support, it doesn’t always cover every local payment method your customers actually use. India is the loudest example: Razorpay is the default payment processor for Indian businesses, not Stripe, because it handles UPI, Paytm, net banking, and RuPay natively and clears payments to Indian bank accounts the same day. Europe has similar stories with iDEAL (Netherlands), Bancontact (Belgium), SOFORT (Germany), and SEPA direct debits, where Mollie and Adyen often have deeper support than Stripe. For direct debit at scale, GoCardless owns the category with its 1% flat fee on ACH and UK Bacs. Whichever region you live in, there’s usually a local-first alternative that beats Stripe on fees, payment methods, or settlement speed.

The 3 types of Stripe alternatives (and why the distinction matters)

Not every “Stripe alternative” does the same job. Before you start comparing fees, you need to understand which category each tool falls into, because they solve very different problems.

- Payment processors / PSPs. The direct competitors to Stripe. They take your customer’s card, authorize it with the card networks, and deposit money in your bank account. Examples: Square, Adyen, Braintree, Authorize.Net, PayPal, Helcim, Checkout.com, Razorpay, Mollie. You’re legally the seller; sales tax, chargebacks, and compliance are your problem. This is where most of this article sits.

- Merchants of record (MoRs). A completely different model. The MoR is the legal seller on the invoice. Your customer pays the MoR, which handles all global sales tax, VAT, fraud, and chargebacks, then pays you the net amount. Examples: Paddle, LemonSqueezy, 2Checkout, Gumroad. You pay a higher percentage (typically 5%+) but you never think about tax compliance again. Dominant for indie SaaS, digital downloads, and solo founders who can’t afford a CFO.

- Billing platforms (subscription management). These sit on top of a payment processor like Stripe or Braintree and add complex subscription logic: trials, proration, coupons, multi-currency pricing, revenue recognition, and dunning. Examples: ChargeBee, Recurly, Zuora. They don’t replace Stripe, they wrap it.

The single biggest mistake I see founders make is picking a tool from one category when they needed one from another. If you’re tired of dealing with sales tax, a PSP won’t help. If you’re paying too much in processing fees, a billing platform won’t help. Figure out which problem you’re actually trying to solve first.

Top 10 Stripe Alternatives in 2026

These are the 10 alternatives that cover the broadest set of use cases. I’ve ordered them roughly by how often I end up recommending each one to real businesses, not alphabetically.

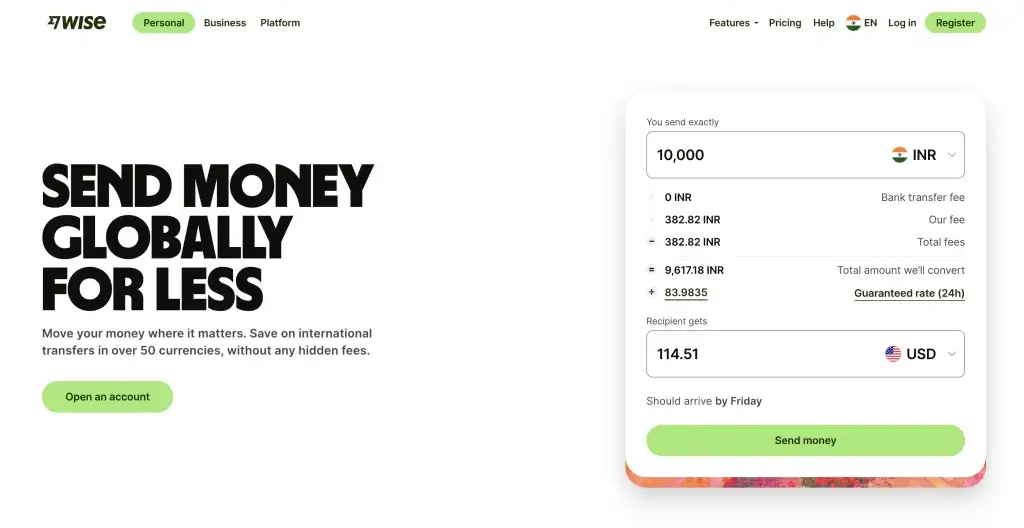

Wise (formerly TransferWise)

- Real mid-market exchange rate

- Multi-currency account

- Transparent, low fees

Wise isn’t a full-stack payment processor in the Stripe sense. It’s a money-transfer and multi-currency banking service, and that’s exactly why I recommend it as the first alternative for a very specific group: freelancers and service businesses who invoice international clients. Wise gives you a free multi-currency business account with local bank details in USD, EUR, GBP, AUD, CAD, SGD, NZD, and HUF, so your European clients can pay you in EUR to a real European bank account, your US clients can ACH-transfer USD to a real US routing number, and you hold the funds in whichever currency you want until you decide to convert.

Wise vs Stripe

- Transaction fees: Wise doesn’t charge for receiving payments into its multi-currency accounts. Currency conversion costs roughly 0.41% on average (it varies by currency pair) using the mid-market exchange rate. Stripe, by comparison, adds 1% on every currency conversion plus 1.5% on international cards. For a freelancer invoicing $10,000/month across currencies, the difference is several hundred dollars a month.

- Key differences: Wise isn’t a credit card processor. You can’t bolt it into a Shopify checkout or accept online card payments through it. What it does do better than Stripe is hold foreign currency at real exchange rates, let you invoice in your client’s local currency, and move money between countries at the cheapest rates on the market. Pair Wise with Stripe: use Stripe for card payments from customers, use Wise for anything involving currency conversion or international payouts.

Payoneer

- Multi-currency receiving accounts

- Marketplace payment integration

- Low-cost currency conversion

Payoneer occupies a different slot from Wise. Where Wise shines for invoicing real humans in multiple currencies, Payoneer is the go-to for getting paid by marketplaces. If you earn money on Upwork, Fiverr, Amazon, Airbnb, Rakuten, or any other platform that pays sellers in bulk, Payoneer is probably already one of your payout options, and it’s usually the cheapest one. You get multi-currency receiving accounts in USD, EUR, GBP, JPY, and several others, and you can either withdraw to your local bank account for a flat $1.50 or hold the balance and pay suppliers directly.

Payoneer vs Stripe

- Transaction fees: Payoneer charges 3% on credit card payments, 1% on eCheck (ACH) payments, free transfers between Payoneer accounts, and $1.50 flat to withdraw to a local bank. Currency conversion is up to 2% above the mid-market rate, which is the one area where Wise beats it.

- Key differences: Payoneer’s native integration with marketplaces is the reason to use it. If you sell on Amazon in 5 countries, Payoneer automatically receives each marketplace’s payouts into separate currency balances and consolidates them in one dashboard. Stripe can’t do that because Stripe isn’t on the payout side of marketplaces at all. For freelancers and ecommerce sellers whose income is mostly marketplace-routed rather than directly invoiced, Payoneer is the default.

PayPal

PayPal is still the most recognized payment brand on the internet, with over 430 million active accounts worldwide, and that brand recognition translates directly into higher checkout conversion for anything selling to consumers. The joke used to be “nobody uses PayPal anymore” and it kept being wrong every year: a Baymard Institute survey found that adding PayPal as a checkout option lifts conversion rates on consumer sites by up to 44% compared to card-only checkouts. For B2C ecommerce specifically, skipping PayPal is leaving money on the table regardless of how much you prefer Stripe’s developer experience.

PayPal vs Stripe

- Transaction fees: PayPal’s domestic rate is 3.49% + $0.49 for Advanced Checkout (Standard Checkout is 2.99% + $0.49). International payments are 4.4% + a fixed fee that varies by currency. So PayPal is consistently about 0.5-1% more expensive per transaction than Stripe. The trade-off is the conversion lift: if adding PayPal gains you 5-10% more successful checkouts, the higher fee pays for itself.

- Key differences: PayPal includes invoicing, subscription billing, buyer-seller disputes, and a built-in user base that already has accounts. Stripe has better developer APIs, cleaner webhook reliability, and a more programmatic approach to customizing checkout. For most DTC brands, the right answer is “both” — Stripe for card rails, PayPal as the alternate button. For pure API-driven SaaS with no physical product, Stripe alone is usually enough.

Also see: Best PayPal Alternatives for Businesses and The Pros and Cons of PayPal for Business

Square

- No monthly fees for basic plan

- POS and online payments

- Invoicing and inventory tools

Square is the default answer for any business that takes payments in person: restaurants, coffee shops, salons, trades, mobile service providers, farmers’ markets, pop-up retail. Stripe Terminal exists but it was built as an afterthought to Stripe’s online payments business. Square started as in-person and everything else (online, invoicing, appointments, payroll, loans) grew from that foundation. The free reader is still the best way to start taking chip and tap payments from day one with no hardware investment.

Square vs Stripe

- Transaction fees: Square is 2.6% + 10¢ for swiped, dipped, or tapped in-person transactions, 2.9% + 30¢ for online payments, and 3.5% + 15¢ for keyed-in phone orders. In-person is the cheapest tier and the one Square really optimizes for. Online rates match Stripe almost exactly.

- Key differences: Square includes a full POS system, an inventory management tool, Square Appointments for service bookings, Square Online for a basic website with checkout, and Square Payroll, all under one account. For a retail or service business, you can run the entire operation out of Square without touching anything else. Stripe plus Shopify plus Calendly plus Gusto will do more things but cost more and take longer to set up. Square is optimized for physical-first businesses; Stripe is optimized for digital-first.

Stax (formerly Fattmerchant)

Stax uses a completely different pricing model from Stripe and almost everyone else on this list: instead of charging a percentage of every transaction, Stax charges a flat monthly subscription (starting around $99/month) and passes interchange fees through at cost with a small cents-per-transaction markup. That makes Stax wildly expensive for small businesses and wildly cheap for high-volume ones. The break-even vs Stripe is somewhere around $15,000/month in card volume. Above that, you’re leaving real money on the table by staying on Stripe.

Stax vs Stripe

- Transaction fees: Flat $99+/month subscription based on volume tier, plus interchange-pass-through (typically 1.8-2.0% for consumer credit cards) plus a small per-transaction markup (~8¢). A business processing $50K/month in mostly retail volume would pay around $900-$1,100/month total with Stax vs roughly $1,500 on Stripe. For $500K/month, the gap is $5,000+/month in savings.

- Key differences: Stax is a subscription-pricing payment processor designed for businesses that have outgrown Stripe’s flat-rate model. The dashboard integrates with QuickBooks, Xero, and most inventory platforms. Where Stripe wins is developer experience and API depth; Stax is a business tool, not a developer platform. If your business doesn’t need to customize checkout or build payments into product features, and you process more than $15K/month, Stax is almost always the cheaper option.

WePay

WePay is owned by JPMorgan Chase and built specifically for software platforms that need to facilitate payments between their users, the same use case Stripe serves with Stripe Connect. If you’re building a marketplace, a SaaS platform that processes payments on behalf of customers (GoFundMe, ConstantContact, Infusionsoft all use or have used WePay), or any tool where the end customer is not you but your customer’s customer, WePay is the direct alternative to Stripe Connect. The Chase ownership gives it the backbone of a real bank, which matters for risk-sensitive verticals.

WePay vs Stripe

- Transaction fees: WePay is 2.9% + 30¢ for online card payments, 1% (capped at $5) for ACH bank transfers, comparable to Stripe on raw processing fees. Platform fees and revenue share are negotiable based on volume; enterprise platforms often get significantly better rates.

- Key differences: WePay’s platform model is tuned for sub-merchant onboarding, where the platform owner takes responsibility for underwriting its users. The Chase integration means faster payouts (often same-day for Chase business accounts) and built-in fraud models trained on Chase’s consumer banking data. Stripe Connect is more flexible and has better docs; WePay is more batteries-included and has better underwriting for niche verticals. For new platform builders in 2026, Stripe Connect is usually the default; WePay wins when you need a bank-backed option or specific Chase integrations.

Adyen

Adyen is the enterprise Stripe. Uber, Spotify, eBay, Netflix, Microsoft, Etsy, and McDonald’s all run on Adyen, and the pattern is that high-volume, global, omnichannel businesses eventually outgrow Stripe’s flat-rate pricing and move to Adyen’s interchange-plus model to save millions in processing fees. Adyen covers card-present, card-not-present, and 250+ local payment methods across Europe, Asia-Pacific, and the Americas on a single platform and a single contract, which matters enormously if you’re a global retailer running physical stores and an online business from the same tech stack.

Adyen vs Stripe

- Transaction fees: Adyen uses interchange-plus: card network interchange (usually 1.5-2.0% on US credit cards, lower in Europe) plus Adyen’s margin, which is typically $0.12 + 0.6% for European cards and higher for Amex. There’s a $120/month minimum to use Adyen, which rules it out for small businesses. For businesses doing $500K+/month in processing, Adyen’s interchange-plus model is usually 30-50% cheaper than Stripe’s 2.9% + 30¢ flat rate.

- Key differences: Adyen is enterprise-only in practice. The account minimums and setup complexity mean it rarely makes sense below roughly $1M/year in processed volume. Above that, it’s the strongest Stripe alternative, especially for international and omnichannel use cases. Stripe is for startups and SMBs with API-first needs; Adyen is for scaled businesses with professional payments teams and cost-per-transaction sensitivity.

Authorize.Net

- Trusted by 440,000+ merchants

- Advanced fraud detection

- Recurring billing and invoicing

Authorize.Net (owned by Visa) is an old-school payment gateway that predates Stripe by almost 15 years and still powers over 440,000 merchants. The important distinction: Authorize.Net is a gateway, not a processor. You pair it with a separate merchant account from a bank or processor (Chase Payment Solutions, Wells Fargo Merchant Services, First Data, etc.) and Authorize.Net handles the technical layer of accepting cards while the merchant account handles the money. That split architecture is what traditional retailers and many long-established online businesses still prefer because you can shop around for a cheaper merchant account independently of your gateway.

Authorize.Net vs Stripe

- Transaction fees: If you use Authorize.Net’s all-in-one plan, it’s $25/month + 2.9% + 30¢, roughly the same as Stripe plus a fixed monthly fee. If you use the gateway-only plan with your own merchant account, it’s $25/month + 10¢ per transaction + $0.10 daily batch fee, and you pay your merchant account provider separately (often at a cheaper rate if you negotiate). For established merchants with a good banking relationship, the gateway-only route frequently beats Stripe.

- Key differences: The big Authorize.Net advantage is flexibility: you can swap merchant accounts without changing your gateway, which means lower risk of getting stranded if your processor freezes your account. The built-in Advanced Fraud Detection Suite with 13 configurable filters is better than Stripe Radar’s defaults out of the box, and recurring billing through the Automated Recurring Billing (ARB) module is stable and well-documented even if it looks dated. Downside: the developer experience feels like 2010 compared to Stripe.

2Checkout (now Verifone)

2Checkout was acquired by Verifone and rebranded but most people still call it 2Checkout. It’s a merchant of record (see the explainer earlier in this article), which means it handles sales tax, VAT, and chargebacks on your behalf as the legal seller, and pays you out net of fees. For small businesses selling digital products globally, 2Checkout is one of the oldest and most battle-tested MoRs on the market, covering 200+ countries, 45+ payment methods, and 30+ languages in a single integration. It’s the pre-Paddle, pre-LemonSqueezy option that still has the edge on raw geographic coverage.

2Checkout vs Stripe

- Transaction fees: 2Checkout has tiered plans: 2Sell at 3.5% + $0.35 for one-time purchases, 2Subscribe at 4.5% + $0.45 for recurring billing, and 2Monetize at 6% + $0.60 for full global compliance with tax, risk, and affiliate management. Higher than Stripe across the board, but you’re paying for a completely different set of services (MoR tax handling, affiliate tools, global payment methods).

- Key differences: 2Checkout’s 200+ country coverage is broader than almost anyone in this category, and it’s particularly strong in emerging markets where Paddle and LemonSqueezy still have gaps. The downside is the dated dashboard and a reputation for slower customer support. If you’re selling software or digital content to customers in 100+ countries and need one invoice per month instead of 47 tax filings per year, 2Checkout is worth the higher fees.

ChargeBee

Chargebee is not a Stripe alternative in the strict sense. It’s a subscription billing platform that sits on top of Stripe, Braintree, Authorize.Net, or Adyen and handles the complex subscription logic those processors don’t do well: trials, proration, usage-based billing, coupons, multi-currency pricing, dunning, revenue recognition, tax compliance via integrations, and the churn-prevention playbook built into the dashboard. It’s the tool SaaS companies reach for when Stripe Billing alone starts creaking under their pricing complexity, usually somewhere between $1M and $10M ARR.

ChargeBee vs Stripe

- Pricing: Chargebee has a free Launch plan for businesses under $250K in total billing, a Performance plan starting at $599/month for scaling SaaS, and custom Enterprise pricing for companies processing eight figures in ARR. Chargebee does not charge per-transaction processing fees; you still pay your payment processor (Stripe, Braintree, etc.) separately. Total cost = Chargebee subscription + Stripe fees.

- Key differences: This is the tool you add to Stripe, not the tool you replace Stripe with. Stripe Billing handles simple subscriptions well; Chargebee handles complex subscriptions (metered usage, multi-plan bundles, contract renewals, revenue recognition) better. If your pricing is “one $29/month plan,” stay on Stripe Billing. If your pricing is a spreadsheet, use Chargebee.

15 more Stripe alternatives worth knowing in 2026

The 10 tools above are the best-known alternatives, but the Stripe-alternatives category has exploded in the last few years, especially in the merchant-of-record and developer-focused payments lanes. Below are 15 more options worth researching if none of the main 10 fit your use case perfectly. I’ve grouped them into merchant-of-record tools for indie SaaS and creators (the biggest growth area), regional processors, platform payments alternatives to Stripe Connect, and traditional SMB processors.

New-generation merchants of record for indie SaaS

Four tools launched in 2023-2024 specifically targeting the same audience that made LemonSqueezy famous: solo SaaS founders, open source maintainers, and indie makers selling digital products. They all solve the same problem (global tax compliance, checkout, subscriptions, invoicing) as a merchant of record, but with faster onboarding, developer-friendly APIs, and better pricing than the established players. This is the most active innovation area in payments right now.

Paddle

Paddle is the most established merchant of record for indie SaaS and digital products. Fees start at 5% + $0.50 per transaction and Paddle handles every global tax jurisdiction, chargeback, and refund on your behalf. The selling point is that you, the founder, never deal with VAT MOSS, digital services tax, or sales tax registration ever again. Paddle pays you a single clean amount each month; everything else is their problem. The 5% premium over Stripe’s 2.9% is the price of outsourcing tax compliance entirely, and for most solo SaaS founders it’s worth it on day one. Powers Jasper, Super Monitoring, MacPaw, and hundreds of other mid-sized SaaS brands.

LemonSqueezy

LemonSqueezy is Paddle’s most visible competitor, also a merchant of record, also charging roughly 5% + $0.50 per transaction. LemonSqueezy was acquired by Stripe in July 2024, which is worth noting if you care about independence, but the product still runs as a standalone brand and continues to serve the indie maker audience. The developer experience is noticeably cleaner than Paddle’s, the dashboard is better-designed, and the affiliate program feature is built in. For solo founders launching a digital product today, LemonSqueezy and Polar.sh are the two tools I’d trial first.

Polar.sh

Polar.sh is the newest, most developer-native merchant of record on this list and the one that’s been generating the loudest buzz in the indie SaaS world since it launched in 2024. Fees are 4% + 40¢, a full percentage point cheaper than Paddle or LemonSqueezy, and the whole product is built around an open-source and GitHub-native workflow. You can sell one-off digital products, subscriptions, usage-based billing, GitHub Sponsors-style recurring donations, and license keys from the same dashboard. The API feels like Stripe’s with MoR tax handling bolted on top, which is the exact combination indie developers have been asking for. If you’re launching a SaaS or dev tool in 2026 and want the cheapest MoR option with the best developer experience, Polar is the one to trial. It’s also open-source itself, which matters if you care about vendor lock-in.

Dodo Payments

Dodo Payments is another 2024 entrant built specifically for global SaaS founders who need merchant-of-record compliance without Paddle’s enterprise-style onboarding. Fees are 4% + 40¢, matching Polar.sh and beating LemonSqueezy. Dodo supports one-time payments, subscriptions, metered billing, and digital license delivery, with a particular emphasis on serving founders in emerging markets (India, Southeast Asia, Latin America) who’ve historically had a hard time getting onboarded to US-based MoRs like LemonSqueezy. Onboarding is fast (hours, not days), the dashboard is clean, and it’s already the default recommendation in several indie SaaS communities for founders outside the US and EU. If Polar feels too dev-centric, Dodo is the friendlier alternative.

Creem.io

Creem.io is the third of the new-generation MoRs launched in 2024. Fees are similar to Polar and Dodo (around 4% + 40¢) and the positioning is SaaS-focused with strong emphasis on subscription lifecycle management, coupon codes, and affiliate programs. Creem has fewer users than Polar or Dodo today but is growing fast in the maker community and its checkout experience is among the cleanest on the market. Worth trialing alongside the other two if you’re comparing new MoRs head-to-head before committing.

FastSpring

FastSpring is the elder statesman of the merchant-of-record category, founded in 2005, and still running on enterprise-style custom pricing (typically 5.9% + $0.95 or negotiated down for volume). If Polar and Dodo are the new lightweight MoRs, FastSpring is the heavyweight that software companies have been using for 20 years. Powers brands like Zoom, Squidoo, RealVNC, and Bitdefender. Slower onboarding than the new crop, higher baseline fees, but better for enterprise SaaS selling six- and seven-figure annual contracts where you need custom quoting, purchase orders, and enterprise compliance features that Polar and LemonSqueezy don’t offer yet.

Platform payments alternatives to Stripe Connect

If you’re building a marketplace, SaaS platform, or any business that processes payments on behalf of your customers, Stripe Connect is the default. These two are the direct alternatives worth considering.

Finix

Finix is a payfac-as-a-service platform that lets software companies become their own payment facilitator. The economic argument: instead of paying Stripe Connect a cut of every transaction your platform routes, you own the payment relationship yourself and keep more of the margin. Makes sense for platforms processing over $50M/year in GMV. Below that, Stripe Connect is easier and probably cheaper. Finix is the main name in this category along with Infinicept and Rainforest.

Rainforest

Rainforest is a newer payfac-as-a-service option built for SaaS companies specifically (rather than general platforms). The pitch is a cleaner developer experience than Finix and tighter integration with the kind of subscription billing that SaaS platforms run on. Worth comparing if you’re looking at becoming your own payfac.

Regional and multi-currency business payments

Airwallex

Airwallex is a global business payments platform that combines multi-currency accounts (like Wise) with card issuing, expense management, and a Stripe-like payment gateway for accepting cards. Fees on card processing are competitive (roughly 1.5-2.5% + a small fixed fee depending on region) and the multi-currency account covers 60+ currencies. If your business spans multiple countries and you want one tool instead of stitching Wise + Stripe + your local bank, Airwallex is the closest thing to a unified global payments stack.

Braintree

Braintree is PayPal-owned and processes cards, PayPal, Venmo, Apple Pay, and Google Pay through a single API. Fees are 2.59% + $0.49 for cards, slightly below Stripe. The big win is native PayPal and Venmo acceptance without a separate integration. If you want PayPal as a checkout option on a Stripe-style developer-friendly API, Braintree is the answer.

Dwolla

Dwolla is a US ACH-only payment platform with pricing that starts around $250/month plus $0.50 per transfer. Not for small merchants, but for fintech apps and platforms that need to move ACH payments at volume (payroll, rent, marketplace disbursements), Dwolla is the API the serious players use. Competes with Stripe’s ACH product on compliance depth and volume pricing.

Traditional SMB alternatives

GoCardless

GoCardless owns the direct debit category. Fees are 1% + £0.20 for UK Bacs, 1% + €0.25 for SEPA, and 1% + $0.25 for US ACH, all capped at small absolute amounts. For recurring B2B invoices where customers expect to pay by bank transfer instead of credit card (common in Europe and the UK), GoCardless is dramatically cheaper than card-based recurring billing and has much lower chargeback risk.

Razorpay

Razorpay is the default payment processor for Indian businesses and the one that matters if you’re selling into India. It natively supports UPI (which is free or nearly free for the processor to route), Paytm, PhonePe, net banking, RuPay, and international cards in a single checkout. Fees are 2% for domestic transactions, 3% for international. Stripe technically works in India but lacks Razorpay’s local payment method depth, and Razorpay settles to Indian bank accounts significantly faster.

Mollie

Mollie is a Dutch payment processor that dominates European ecommerce. It supports local methods like iDEAL (Netherlands), Bancontact (Belgium), SOFORT (Germany), and Klarna/PayPal alongside regular cards. European card fees are roughly 1.8% + €0.25, significantly below Stripe’s European rates. If your customers are primarily in Europe and use local bank-transfer methods, Mollie is the cheapest and most native option.

Checkout.com

Checkout.com is enterprise-grade, interchange-plus pricing, and specifically strong for global businesses with complex fraud and authorization optimization needs. It’s the processor behind Deliveroo, Klarna, Henkel, and Patreon. Not for SMBs; below $1M/year in processed volume you probably won’t get an account. Above that, it’s a direct Adyen and Stripe enterprise competitor.

Helcim

Helcim is a Canadian interchange-plus processor with zero monthly fees, transparent pricing, and a better-than-Stripe dashboard for US and Canadian small businesses. Typical rates work out to roughly 0.3% + 8¢ markup over interchange for online transactions, which beats Stripe’s flat 2.9% + 30¢ for businesses processing more than about $5K/month. No monthly minimum, no setup fees, and volume discounts kick in automatically. Helcim is my quiet pick for small US and Canadian businesses that want to save money without committing to Stax’s subscription model.

Gumroad

Gumroad is the simplest merchant-of-record option and also the most expensive: a flat 10% + 50¢ per transaction. You don’t get a dashboard the way Paddle or LemonSqueezy give you, and you don’t get an API worth building on. What you get is zero setup time. Upload a product, get a link, share it, start selling. For creators selling ebooks, courses, art assets, or one-off digital products, Gumroad is the fastest path from idea to first dollar, even if the 10% fee makes it wildly uneconomical at scale.

Which Stripe alternative should you actually pick?

Instead of a vague “it depends,” here’s the decision framework I’d walk a real business through. Match your situation to one of these and you have your answer.

- Solo SaaS founder or indie maker selling digital products globally → Polar.sh, Dodo Payments, or LemonSqueezy. The 4% MoR fee (5% for Lemon) is cheaper than Paddle and you’ll never deal with VAT MOSS again. Polar for dev-heavy tools, Dodo if you’re based outside the US/EU, LemonSqueezy for creator-brand polish.

- Enterprise SaaS with 7-figure contracts and custom pricing → FastSpring or Paddle. They’re older and more expensive, but support purchase orders, enterprise invoicing, and compliance workflows the newer MoRs don’t.

- Global business operating in 3+ countries → Airwallex for unified multi-currency accounts plus card processing in one platform.

- Platform processing $50M+/year on behalf of customers → Finix or Rainforest. Become your own payfac and keep the margin Stripe Connect would otherwise take.

- Freelancer invoicing international clients → Wise for receiving the money, Stripe or Payoneer for card acceptance if needed.

- Amazon/Upwork/Fiverr seller → Payoneer. It’s the default payout option on all those platforms anyway.

- DTC ecommerce brand under $1M/year → Stripe is fine. Add PayPal as a second checkout option via Braintree for the conversion lift.

- DTC brand over $1M/year → Look at Stax or move to Adyen for processing cost savings of 30-50%.

- Brick-and-mortar retail or service business → Square. Not even close.

- SaaS with complex subscription pricing (usage, tiers, trials, proration) → Chargebee on top of Stripe, not instead of it.

- SaaS platform enabling payments for your customers’ customers → Stripe Connect is the default; WePay if you need Chase’s underwriting and settlement.

- B2B with recurring bank-transfer invoicing → GoCardless. The per-transaction economics are unbeatable.

- Indian business selling to Indian customers → Razorpay. UPI alone makes this decision.

- European ecommerce targeting Europe → Mollie. Local payment methods, lower card fees.

- Legacy online business with existing merchant account → Authorize.Net. Gateway independence is worth a lot.

- Digital product creator, one product, want to sell it today → Gumroad for pure speed (10% fee), or Polar.sh / Dodo Payments at 4% if you can spend 30 extra minutes on setup.

- Enterprise with 8-figure processing volume → Adyen or Checkout.com. Interchange-plus at that scale is where the real savings are.

Frequently Asked Questions

What are the best Stripe alternatives for small businesses?

The best Stripe alternatives for small businesses in 2026 depend on your business model. For brick-and-mortar retail and service businesses, Square is the clear winner. For freelancers and international invoicing, Wise is cheaper than Stripe on currency conversion. For indie SaaS and digital products, LemonSqueezy or Paddle handle global tax compliance that Stripe leaves on your plate. For high-volume merchants over $15K/month, Stax’s subscription pricing saves thousands vs Stripe’s percentage fees.

Is there a payment processor cheaper than Stripe?

Yes, several. Helcim’s interchange-plus pricing is cheaper than Stripe’s 2.9% + 30¢ flat rate for any business processing over roughly $5,000/month. Stax with its flat monthly subscription is dramatically cheaper for businesses over $15,000/month. Adyen and Checkout.com are cheaper at enterprise volumes ($1M+/year). Mollie is cheaper for European card transactions (1.8% + €0.25 vs Stripe’s European rates). Braintree is slightly cheaper (2.59% + 49¢) and includes PayPal native.

What is a merchant of record and how does it differ from Stripe?

A merchant of record (MoR) is the legal seller on every invoice sent to your customers. You build the product, the MoR handles the checkout, collects the money, pays global sales tax and VAT, handles chargebacks and refunds, and sends you a clean monthly payout net of fees. Stripe is a payment processor, not a merchant of record, which means taxes and compliance are your problem. Popular merchant-of-record alternatives include Paddle, LemonSqueezy, 2Checkout, and Gumroad. They charge higher fees (typically 5%+) but remove all global tax complexity.

Which Stripe alternative is best for international payments?

Depends on the use case. For receiving international invoices as a freelancer or service business, Wise has the lowest currency conversion costs (around 0.4-1%). For accepting international card payments on a website, Adyen and Checkout.com offer the broadest local payment method coverage. For global SaaS selling in 100+ countries, 2Checkout, Paddle, and LemonSqueezy as merchants of record handle tax compliance automatically. Stripe adds 1.5% surcharge on international cards plus 1% currency conversion, which is where most alternatives beat it on price.

Can I accept payments without Stripe or PayPal?

Yes. Square accepts cards in-person and online without either. Authorize.Net works with any merchant account. Adyen, Checkout.com, Braintree, Helcim, and Mollie all process card payments independently of both Stripe and PayPal. For digital products, Paddle, LemonSqueezy, Gumroad, and 2Checkout are complete merchant-of-record alternatives. Regional players like Razorpay (India), Mollie (Europe), and GoCardless (direct debit globally) cover their markets natively without needing either.

What is the difference between a payment gateway and a payment processor?

A payment gateway (like Authorize.Net) is the technical layer that transmits card data from your checkout page to a payment processor. A payment processor (like Stripe, Square, Adyen) actually moves money between the card network and your bank account. Modern tools like Stripe and Square bundle gateway and processor together in one integrated service, which is why the distinction feels academic today. It still matters for traditional merchants using gateway-only tools like Authorize.Net, because you can swap merchant accounts without changing your gateway.

Is PayPal cheaper than Stripe?

No, PayPal is consistently more expensive than Stripe on a per-transaction basis. PayPal Checkout charges 3.49% + $0.49 per domestic transaction compared to Stripe’s 2.9% + $0.30. International payments are even worse on PayPal, at 4.4% plus a fixed fee. However, PayPal drives higher conversion rates on consumer checkouts (the Baymard Institute measured up to a 44% lift from adding PayPal as a button), so total revenue with PayPal can still beat total revenue without it despite the higher fee per transaction.

Which payment processor is best for subscription businesses?

For simple recurring billing, Stripe Billing at 0.5% on top of standard processing is fine. For complex SaaS subscription models with trials, proration, metered usage, and multi-currency pricing, Chargebee layered on top of Stripe or Braintree is the industry standard. For indie SaaS that wants zero tax compliance headaches, Paddle or LemonSqueezy as merchants of record include subscription management plus global tax handling in their 5% fee. ChargeBee is free under $250K in total billing, which covers most early-stage SaaS.

What is the best Stripe alternative for SaaS?

Three clear categories: (1) Solo SaaS and indie founders under $1M ARR → LemonSqueezy or Paddle, because merchant-of-record tax handling saves weeks of compliance work. (2) Mid-market SaaS from $1M-$10M ARR → Stripe plus Chargebee for subscription complexity, or Braintree if you need native PayPal. (3) Enterprise SaaS over $10M ARR → Adyen or Checkout.com for interchange-plus savings, combined with a billing platform like Chargebee or Zuora. Stripe alone works fine in the middle tier; it falls short at the extremes.

Does Stripe charge a monthly fee?

No, Stripe’s standard pricing has no monthly fee and no minimums. You pay only per transaction: 2.9% + $0.30 for online US card payments, plus surcharges for Stripe Billing (+0.5%), Stripe Tax (+0.5%), and international cards (+1.5%). The lack of a monthly fee is one of Stripe’s biggest advantages over traditional processors like Authorize.Net ($25/month) or Stax ($99+/month), and a big part of why early-stage businesses default to it.

Why do businesses leave Stripe?

The top three reasons: (1) Account freezes or reserve holds by Stripe’s automated risk engine, which is why higher-risk businesses often migrate to Authorize.Net, Braintree, or Adyen. (2) Rising processing costs at scale, where interchange-plus pricing from Adyen, Stax, or Helcim becomes dramatically cheaper above $15K-$50K/month in volume. (3) Global sales tax complexity, where merchants of record like Paddle and LemonSqueezy remove compliance burden that Stripe leaves to the merchant. Smaller reasons include lack of regional payment methods (India, Brazil, Japan) and missing features like native PayPal acceptance.

What is the best Stripe alternative for high-risk businesses?

Stripe’s risk engine aggressively flags categories like CBD, supplements, adult content, coaching, and any business with a high chargeback rate. Traditional gateway-plus-merchant-account setups like Authorize.Net paired with a high-risk merchant account provider (PaymentCloud, Durango Merchant Services, SMB Global) are the standard answer for businesses that have been turned down or frozen by Stripe. Square is also more forgiving than Stripe in certain categories. Avoid Stax and Adyen if you’re high-risk, as they’re unlikely to onboard you.

Conclusion

Stripe is a great payment processor, not the only one, and not even the right one for most of the business models I see every week. If you’re a freelancer invoicing internationally, Wise will save you hundreds a month in currency conversion. If you sell digital products to a global audience, a new-generation merchant of record like Polar.sh, Dodo Payments, or LemonSqueezy will save you from ever thinking about VAT again, at a cheaper rate than Paddle. If you run a brick-and-mortar business, Square will do what Stripe Terminal pretends to do. If you process more than $15,000/month in cards, Stax or Helcim will cut your processing fees by 30% or more. If you’re in India, Razorpay. If you’re in Europe, Mollie. If you need a global business account with card acceptance in one tool, Airwallex. If your subscription logic is a spreadsheet, Chargebee. If you’re an enterprise at scale, Adyen. The Stripe-alternatives category has 25+ real contenders now across merchant-of-record, regional processors, platform payments, and traditional merchant services. Somewhere in that list is the tool that fits you better than Stripe does.

The biggest mistake founders make with payments is picking the tool their last job used and never revisiting the decision. Take 30 minutes, match your business to one of the scenarios in the decision framework above, and if you’re not already on the right processor, run the numbers. A 1% fee difference on $200K/month of processing is $24,000 a year. That’s a full-time hire. It’s worth 30 minutes of your attention.

Disclaimer: This site is reader-supported. If you buy through some links, I may earn a small commission at no extra cost to you. I only recommend tools I trust and would use myself. Your support helps keep gauravtiwari.org free and focused on real-world advice. Thanks. - Gaurav Tiwari